First, it is not the banks collecting surcharges, it is the businesses selling one goods or services who are putting on the extra charge. So don’t blame the banks.

Second, I have never paid surcharges for card payments when using normal Eftpos. Using the credit card network, yes. But not often for Visa or MC.

Expect that you probably will unless you always use cash even if only when out and about in other areas than your regular locality.

Surcharges are the norm up Eltham way, including some businesses that add a fixed cost regardless of what plastic one uses, credit and EFTPOS alike. It has become a rare business here that doesn’t.

Some related topics include

and others.

I also see fewer and fewer businesses posting their surcharges as they are legally obliged to do. It often is only on the terminal that posts ‘there may be a surcharge, OK’.

It would seem the fairest thing would be for government to mandate businesses post all inclusive costs of every product and service as is required with GST, accepting there are other complexities of inconsistent costs for the merchant, all solvable. In the US many business post cash and credit prices, especially at servos.

Also note, those pesky fees are tax deductible to the business in most cases! Few businesses mention that when one complains about their surcharge.

We often have this exchange. It is almost as if Eltham was a different country to the parts of Melbourne I shop in. Maybe this insideous practice of surcharging will spread my way in time. Maybe, maybe not.

But for now, my experience is card payment surcharges are rare for Eftpos. And so I comment as such.

My understanding is that businesses are passing on the charges that the banks put on to them for using cards.

And yes, I have been charged for using debit card as well. You are lucky you haven’t.

I might visit a few instances and just cut and paste then

While in the EU there were limited areas that surcharged, but where it was done it was near blanket. While rare in the USA overall where I visited, New Orleans was an example of merit. Virtually every business in the [tourist] French Quarter surcharged and most had a privately operated ATM machine (ka-ching) charging $3.35 per transaction and dispensing all $20 notes to encourage multiple transactions. A pocketful of $20 notes gets heavy/thick quickly. Going to the edges of the French Quarter there were a few bank ATMs, and no bank ATM charged for getting cash out. A handy money maker for the ATM operator and probably the business who got their surcharges (3.5 to 4%) and probably a percent of those $3.35 charges as commissions.

Yes that is what they are doing. Provision of card processing is a cost to business. So they pass on a surcharge to cover their business cost sometimes. Because they can.

Do they pass on the cost of providing employees to serve customers? Do they pass on the cost of cooking and serving food? Do they pass on the cost of rent, insurance, or all the myriad of business expenses?

Mostly covered by the final price. But it seems to be becoming normalized that if one pays by card, why not add an extra charge. Well not me. I reject that model.

If using an Eftpos card, is it up to one’s bank whether there is a surcharge?

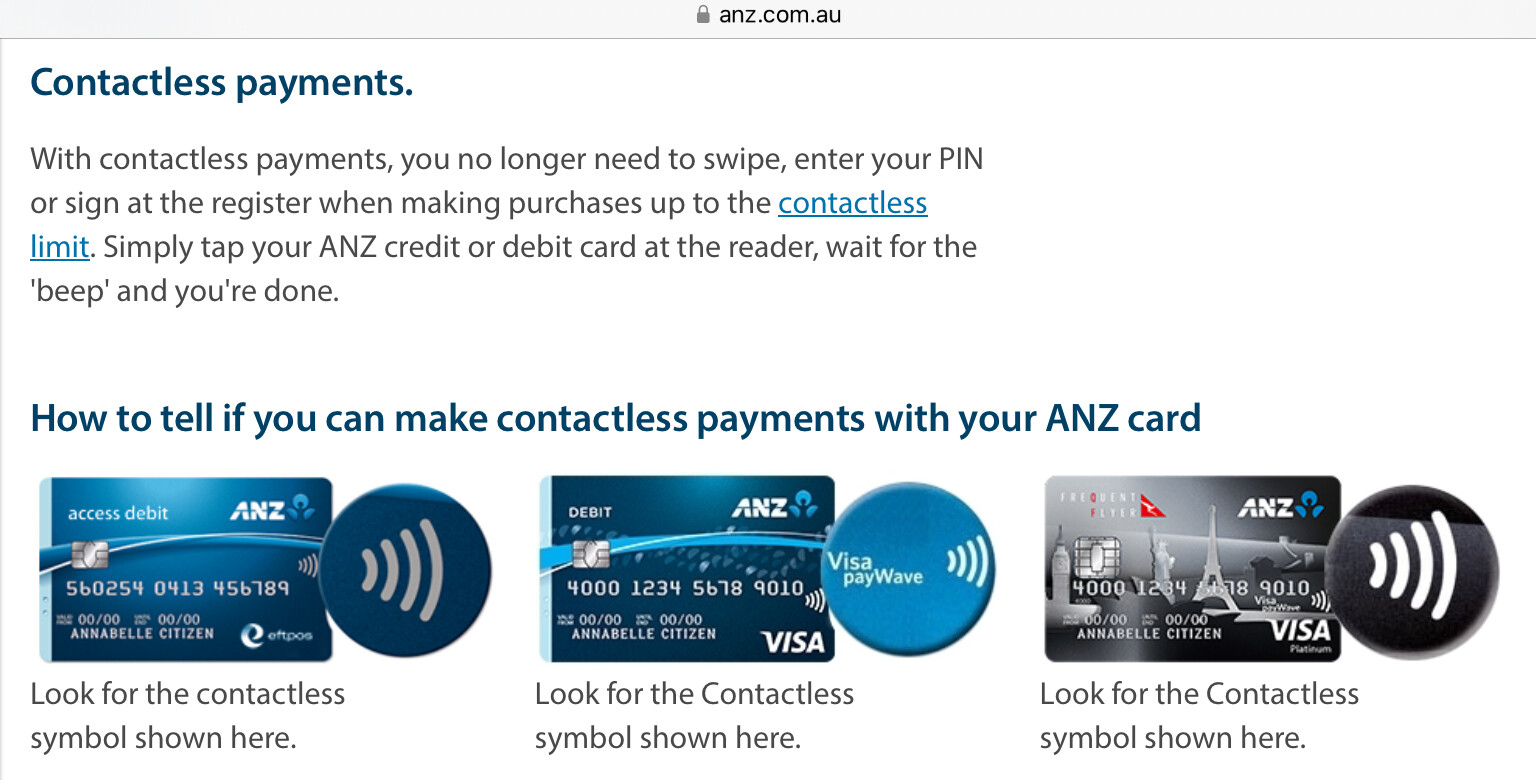

Looking to our two banks they promote the Visa Debit card over the Eftpos only card option. To be expected given Eftpos cards do not support contactless payment. Square has become increasingly common in particular with smaller retailers. Their basic terminal appears to only offer contactless payment.

Is this the future?

They do. A Visa/MasterCard debit card is also an Eftpos card. Latest version of Eftpos cards slso have contactless functionality, as seen on this example card:

Furthermore, with least cost routing which is becoming more common across point of sale transaction processing equipment, transactions are pushed through the Eftpos system where possible.

If one taps (contactless) the transaction can either be processed as credit for credit cards, Eftpos if it is a Visa/MasterCard debit or Eftpos if it is an Eftpos card.

The main difference between Eftpos and Visa/MasterCard debit card is Eftpos can’t used for what are called MOTO transactions. MOTO stands for mail orders and telephone orders (and includes online orders).

Hopefully that becomes more common. ANZ promotes Visa Debit/Credit cards. Re contactless options, even the ANZ branded card with Eftpos in one corner is labelled as a debit card in the opposite.

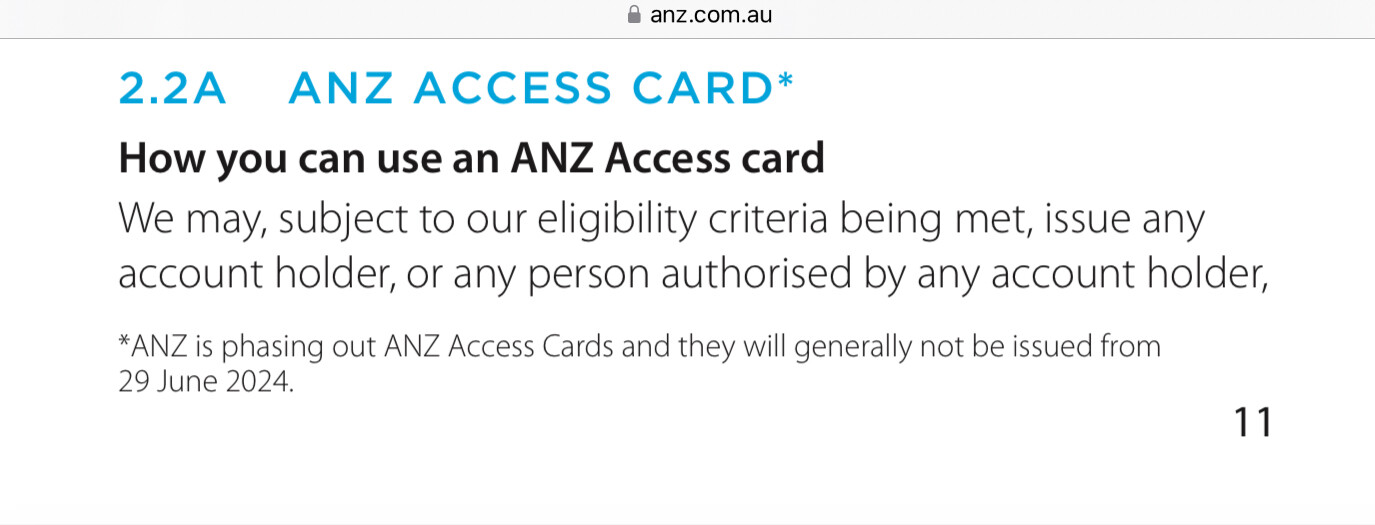

It’s relevant that the ANZ personal account Access Card has been able to be used for Eftpos transactions. This looks to be coming to an end for customers as cards expire. So far all other references I’ve seen refer to ANZ providing Visa Debit cards. Whether these will offer the option for Eftpos rather than debit when used might need a deeper search of ANZ.

A second observation - Is EFTPOS always surcharge free?

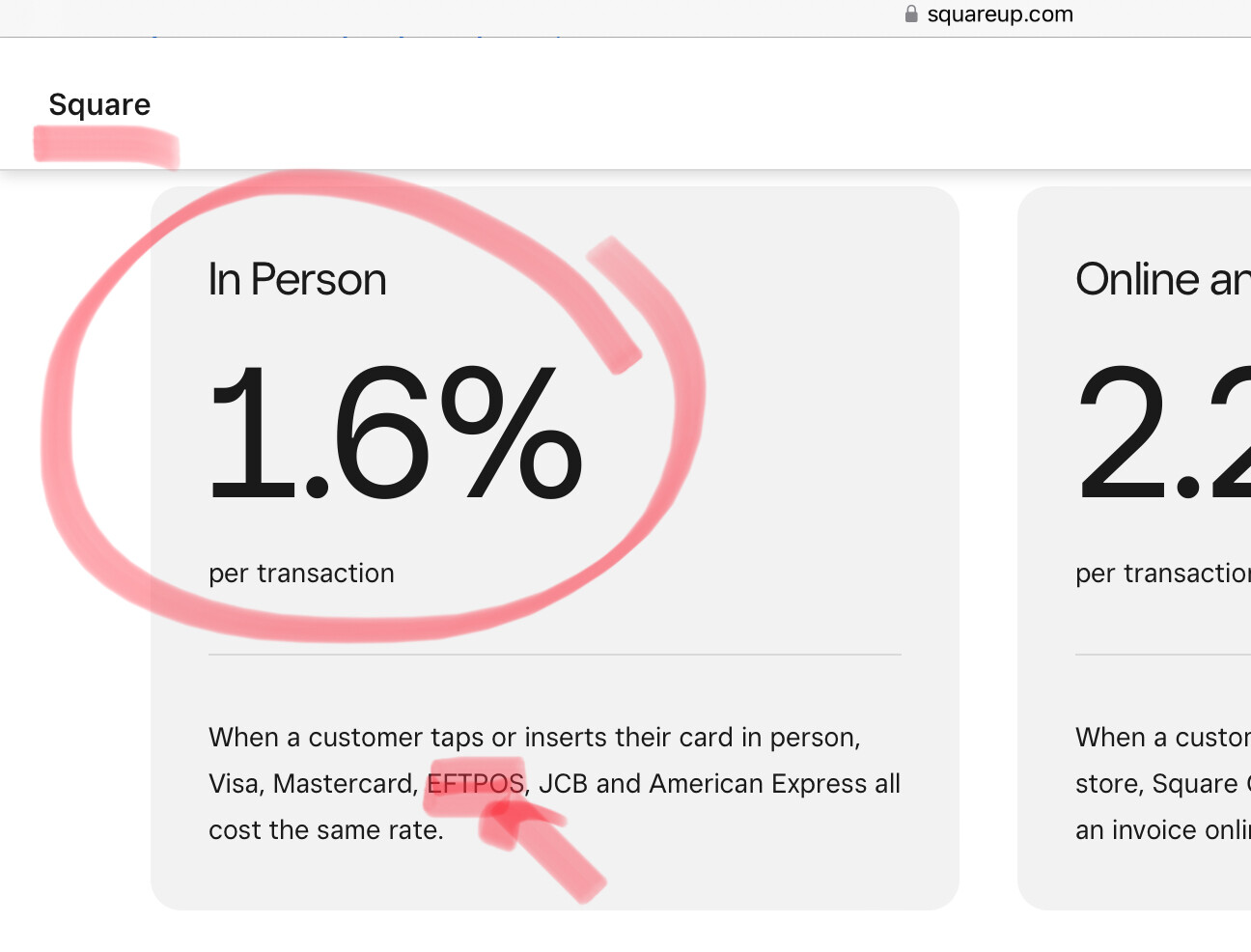

Irrespective of whether the merchant (retailer) adds a surcharge (up to 1.6% for an in person card payment), Square charge the merchant for processing EFTPOS, exactly the same as every other card type. Note only chip enabled EFTPOS cards are accepted if bank issued.

‘Understanding Square's Processing Fees | Square Payments

Eftpos are debit cards. Likewise Visa/MasterCard debit cards

It is very common and now over 50% of businesses would have switched over to LCR. In 2022/23 the RBA:

just over a half of merchants had LCR enabled, despite LCR being available to approximately 99 per cent of merchants by June 2023 (RBA 2023).[4] Small merchants are more likely to have LCR turned on, particularly those with less than $1 million in annual card transactions (Graph 3). Higher take-up among smaller merchants may be due to their higher use of fixed pricing plans (which increasingly have LCR enabled automatically): 95 per cent of merchants with fixed plans in 2022/23 had LCR turned on, compared with just 54 per cent of merchants on blended plans and only 15 per cent on unblended plans

It is worth noting that businesses incur merchant fees when Eftpos cards are presented. In the past for bank issued POS equipment, these were usually substantially less than for Visa/MasterCard/Amex/UnionPay etc card presentations.

However, with LCR, many bank now offer fixed rate merchant fees for any card type presented (noting Amex, Diner and other less common cards may incur higher merchant fees if accepted). This means a business pays same fees irrespective if it is a Eftpos card, Visa/MasterCard credit card or Visa/MasterCard debit card. Hence, some businesses now charge a flat surcharge rate for these cards.

A few of our locals add $0.50 flat rate for any plastic, not a percentage, regardless of sale amount. Whether that meets the spirit or intent of the law is another matter - that is how they have been operating for many months.

There has ALWAYS been a cost to merchants whatever payment was used. Using the Eftpos network was typically less than using the credit card provider’s networks, and with Amex and Diners club charging more than Visa or MC. There is a cost to dealing with cash, as has been seen recently now that the big cash customers like banks and the Colesworths are putting in tens of millions a year to keep Armagard going. There was a cost to cheque processing to the clearing house system, as well as the risk of cheques bouncing.

It is all irrelevent in my view. Any payment method has costs to the merchant. The issue is whether the business passes on the TRUE cost of the payment method, or as some are doing now just ignoring that RB requirement, or absorb the cost into their business operations.

If one were to take this surcharge model to recoup business costs to the next level, how long before there will be a surcharge for cash payments?. How long before there is a surcharge for a hot pie vs a cold pastry because the business had to pay for electricity to heat the pie? How long before there is a surcharge for eat-in vs takeaway because the business had to pay for staff to clean the tables and use cleaning products?

If business’s costs for payments by credit card is 1% and it charges a 1% surcharge for credit card payments, a customer buying a coffee for $4 would pay a four cents surcharge.

If the business decides to charge a 50 cent surcharge for all card payments on transactions less than $10 and a customer buys a coffee for $4, that surcharge is a 12.5% surcharge. This would exceed the businesses cost of acceptance for that transaction.

Having rules, regulations, and laws is one thing. Policing them is something else, rarely known in much of Australia unless there is a formal complaint lodged, and then they prioritise.

Is it a suggestion that because the POS providers charge for the service, and not provide it free, that they should be blamed when businesses hit customers with a surcharge?

I guess we would be bashing the electricity, gas, water, phone companies, NBN, insurers, councils, et al, for not providing their services for free.

Some business include the bank (merchant) or POS fees into overall cost of doing business. Consumers pay for these fees indirectly as they are included within the purchase price.

Others chose to pass on the fees separately as surcharges to the customer. These are directly passed onto the consumer.

Surcharges are visible to the consumer…including fees within the purchase price isn’t.

In some ways, surcharges may be seen as fairer as it is a user pays system. Whereas everyone pays the same fee irrespective of the payment method when the fees are included in the purchase price.

Either way, the cost of the fees are passed onto the consumer either directly or indirectly, so you are correct that businesses ‘pass it on to the customers’.