Yes, you would have to wonder if the penalty even came anywhere near what was allegedly incorrectly taken by the alleged breaches (noting here that “The payment of a penalty specified in an infringement notice is not an admission of a contravention of the Competition and Consumer Act 2010 (CCA)”).

Weaker than water as my late father may have said except the water may have been replaced by a more noisome liquid.

Government sets nothing by example, excepting its own self serving ends. Noting surcharging is limited to the cost to the business of accepting a card payment I was curious about paying taxes by card and found the ATO surcharges are a miserly

while for comparison, over at home Homeaffairs

Government seems to have negotiated to get a good deal for their bankers with every agency for itself, by itself, eh. /sarcasm

Down at Vicroads they might not have gotten the message they could put more into the bankers pockets because the merchant fee is 0.54% for all VISA and Mastercard transactions.

I suspect the point has been made that we remain nought but fodder for the system to partake from and it is all above board since it is transparent.

Since it is all transparent it is all right, right?

I have just booked a return flight with Qantas - cost $804.74. Because of necessity, it had to be done on line (is there a travel agent that accepts cash - if any are open?). This included a card fee of $7.45.

I thought this sort have gouging had been stopped by the ACCC?

Can someone please explain?

Thanks

John Blakey

Hi john, I moved your query to this older relevant topic.

The ACCC position is, and specifically read the first example.

Note that banks charge a business percentages, but some airlines charge a flat fee, and the latter is only glibly referenced without definition. It is essentially a wink-wink nudge-nudge situation as I see it.

Choice seems to agree, using different terminology and looking at foreign carriers. I also enjoy the difference between a surcharge and other equivalent words for the same outcomes of dollars in pockets.

I hope that helps understand how and why we continue to be subjected to these ripoffs.

I am beginning to notice that every time I use my Debit card e.g. paying the toll fee automatically out of my account, or paying for Theatre tickets, I am being charged a fee. It is not much (7c on a $20 refill with Linkt ) but it certainly adds up over time. One accommodation place charged me $35 + and I used my Debit card. I should have taken out the cash, taken the risk of carrying so much cash ($4,000) and not being charged anything.

Has anyone else seen these charges? the Banks are very sneaky!!!

Hi @BlinkyBill and welcome to the Community. I have moved your post into this one about the limiting of surcharges on Credit Card like transacting.

Use of a Debit Card will often attract surcharges if used like a normal Credit Card transaction. This means Linkt for one I know charges a transaction fee, debit card payments are through a Credit Card facility (Mastercard or Visa) and so can attract fees from the establishment where they are used. This is not the Bank adding a fee. To avoid the possible CC surcharge, means that the transaction should be paid either by using the Savings Account choice, by paying cash, but not by providing the Debit Card number or the tap and go facility.

The ACCC/RBA notice about how to display surcharges is seemingly not enforced.

Never make an assumption about surcharges - always ask if there is no obvious posted signage in view. Some businesses are not posting, some only have it on their terminal, and some have it in small print somewhere (eg the bottom margin of a cafe/restaurant menu).

There are an increasing number of businesses that add (usually small) charges even for EFTPOS. A local butcher has a $0.30 charge for any non-cash transaction as an example. Another local business treats EFTPOS and credit transactions the same way. Who knows what shonky deal they have with their provider and might pay the same but who is going to demand a look-see of their books for ‘excessive surcharges’? (no need to answer)

After reporting a few it appears the ‘regulators’ are making a list and checking it never, but it is opaque what might happen behind the curtains. We called out one for incorrect rounding w/cards and a few months later they started rounding correctly so one can never tell.

With some non-bank POS payment systems, the merchant fee is the same irrespective of the card used (efptos, Visa/MasterCard debit or credit card).

For the system used in our business (SquareUp) it is a flat rate of 1.9% for any presented card and 2.2% for manual card entries (e.g. over the phone payment when a card is presented but card details are entered into the payment system). Some businesses absorb these fees in their business costs (like we do) or pass the fees onto a consumer.

Likewise some online payment systems charge flat rates irrespective of the card presented (ours does).

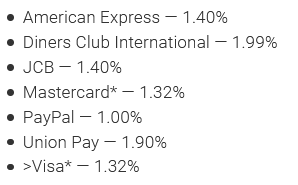

Some bank POS/eftpos payment systems have varying rates between card types (debit/credit/eftpos cards) and can have different rates depending on the card type of card presented (e.g. Amex is usually higher than Visa/Mastercard).

Many businesses use non-banking POS payment systems as they are more cost effective and/or practicable for the size and nature of the business.

One shouldn’t think that eftpos or debit card surcharges are cheaper than credit cards as it may not be the case. The only way to find out is to ask the business if they charge a surcharge and what it is for the type and branding of card presented.

Does the knowledge extend to the staff on the counter?

For a small owner operated business likely first hand knowledge. Although I know one couple who divided business skills between the physical and the paperwork, hence a 50-50 success likely. Hopefully the large retailers have the answer in their store staff training manuals.

What does one do when the staff cannot provide a succinct answer? Hopefully it’s written down somewhere handy, but often it’s not evident until it comes to making payment.

When you paid, did you tap or did you poke your card into the POS machine? I have a vague recollection that if you tap a debit card, it is treated like a credit card.

That’s correct. Through bank POS payment systems using bank issued Visa/Mastercard Debit Cards, tapping a card goes through the credit card payment system. Swiping or inserting the card goes through the EFTPOS payment system. The merchant rates for these can vary depending on the POS platform used by a business.

It once was true. I suspect it still is depending on?

…… One of the local small businesses recently started adding a surcharge to card payments and advised customers inserting the card would cost less compared to tap and go. No mention if the card and account type was relevant. And even the owner seemed a little uncertain, or keen to encourage tap and go.

I’m still looking for a recent answer to confirm it is still so. Through the haze of consumer ignorance, little seems straight forward.

That is correct and any differences in merchant fees lie with the type of SquareUp POS console used.

I suspect that when a Eftpos card (either bank issued eftpos card of a debit card swiped/inserted with cheque or savings selected), SquareUp (and its competitors) processes these through the credit card payment systems rather than through the Australian Eftpos system.as SquareUp isn’t a Eftpos Partner. In such case the merchant would be charged the application card presentation rate (since Eftpos can’t be used unless presented).

I wonder how many intending customers expecting to use their debit card realise there is no additional benefit before presenting the card for payment? My recollection is each time I’ve used a card to pay through Square I was advised there was no extra fee for card payments.

Not Square but one local, it’s clear, assuming one understands that eftpos is not tap and go and not credit?

It’s open to ask or survey the average consumer to establish just how many of us understand the different choices, and how many do choose the easy way? The marketing seems to be all for the convenience of contactless, IE Tap and Go. It feels like we are being set up for another phase in how we pay for services that will financially most benefit others.

I don’t use a digital wallet or phone App. Do they facilitate direct debit via contactless or is it no longer an option?