I lodged a short coat for dry cleaning recently and was quoted $30.05. When I collected it, I offered cash payment but I was refused. Card payments only!

That was not stipulated when I left the coat for cleaning. If I had not had a credit card, I don’t know how that would have turned out. Perhaps it is assumed that everyone has a credit card these days.

Furthermore, when I checked my receipt, I noted that I had been charged an additional 0.45c surcharge - for using my credit card. I can see that that is a 1.5% surcharge on the $30.05 payment but I would have preferred to pay cash.

Is that unfair trading? If the store does not accept cash, that should be made clear and the all-up price quoted at the outset.

It seems to me that it is a business decision to refuse to accept cash payment. It saves the inconvenience of banking cash. But should customers have to bear the cost of that business decision?

I pointed out to the young person at the counter that I was not happy with this transaction but I let her know I was not blaming her. I asked her to pass on my displeasure to her boss.

Because of Covid, many businesses chose not to accept cash, which is legal subject to one requirement - customers are advised of this requirement before committing to a purchase or service (contract). This news article sums it up well:

As long as the business advises cash isn’t accepted either with a notice/sign in-store, verbally or by other means, it is legal.

Whilst they don’t have to accept cash, my understanding is they MUST offer a form of payment that does not require additional payment of a surcharge. So how can you pay without surcharge here except with cash.

If cash is not accepted, then there must be method of payment that is free of any sort of fee or surcharge. Or the displayed price should include the surcharge that is to be applied. It cannot be added on to the displayed price as a separate charge.

So if it is by, say debit card, then no charge can applied. Mind you, I have not encountered many places that apply a charge for Eftpos or debit cards.

The ACCC makes this clear.

So in the original poster’s amount of $30.05 that should have been the amount charged.

In the first instance it’s left to the consumer to known their rights and relevant legal requirements. The most difficult discussion for many of us is politely questioning the seller and asserting ourselves (challenging) the actions of the person on the other side of the counter.

Many businesses which do not accept cash avoid the issue by allowing for the added cost of CC etc payment in the minimum price. IE no surcharge added. The average cost is accepted as a cost of doing business.

Thank you, phb, don2 and Gregr for your advice. I hadn’t considered the Covid angle, and I accept that as a further point that may have prompted the business decision not to accept cash. (It is hard to discuss that point with the business when it is fronted by a young girl who is just carrying out the business policy!) I did Google the business and did not find a contact to reach out to.

The transaction just did not feel fair - being quoted one price on the docket when I left the garment and being charged a different amount when I collected it. And I was not made aware of the “card only” policy when I began the transaction.

The news item on “Cash myth debunked…” is interesting and may be a pointer for the future. With that in mind, I am awaiting receipt of a debit card to include in my wallet from now on.

I agree and would have been perfectly happy if the docket price shown was “allowing for the added cost of CC etc payment in the minimum price”.

And yes, “politely questioning the seller and asserting ourselves (challenging) the actions of the person on the other side of the counter” is not just difficult but impossible when that person is not responsible for the issue.

There are an increasing number of mostly small businesses we encounter that ‘prefer cash’ and apply a flat rate to any kind of card used. $0.30 per transaction has been common in one local centre where a butcher started it and the other shops followed. All of them prominently display the surcharge.

This might not allow one to avoid fees. For some businesses, the merchant fees charged by the point of sale payment provider is the same for credit cards and debit cards. A business can pass on reasonable costs to the consumer, which in same cases will be the same for both card types. Our own provider is an example where this occurs (noting we don’t pass a surcharge onto our customers).

If a business isn’t charged the same merchant fees for debit or credit cards, the business can’t charge the same surcharge, for both card types, to a consumer. A debit card can have lower or no fees in such case.

There is no obligation for a business to offer a surcharge free method of payment. A business may chose a surcharge free option in the interests of keeping a customer happy.

Unlike businesses choosing not to accept cash, there is no obligation for a business to advertise payment surcharges. Some businesses outline these at the point that payment is made (e.g. Aldi within the EFTPOS consol screen) or not at all which was highlighted in another thread about post-payment charges imposed by the point of sale payment provider.

While there is no obligation, one would hope that a business advises of charges before shopping/services are engaged so the customer can make an informed decision of whether they wish to proceed with the business in question.

Firstly businesses must be prepared to accept a Debit Card, with no additional fee.

Secondly, I understand that businesses are required to accept “the coin of the realm” as legal tender.

It is possible that businesses maybe able to avoid this requirement if they place adequate notices in view of the customer before any transaction is commenced.

Thirdly, if businesses refuse to accept cash and will only accept a Credit Card then those businesses should have to wear the surcharge the banks charge.

The short answer is no. While Australian currency is legal tender (meaning other currencies can’t be used), it doesn’t mean that cash must be the only By purchasing goods or services, you’re entering into a contract with the seller. A business can set the terms of the contract prior to the purchase, including how payment will be made.

Therefore if you provide verbal or written notice prior to entering the contract with your customer, your business isn’t obliged to accept cash as a form of payment. And instead, you can state you’re only accepting cashless payments.

For example, a business could state that they’re only accepting card-only payments. Therefore their customers could be required to use a debit card or a credit card. In practice, this is how vending machines can exclude the use of low-denomination coins by displaying a sign notifying purchasers.

Similarly, some small businesses refuse cash payments when they don’t want to deal with the expenses of carrying and accepting cash. It’s not uncommon for some shops to display place signs at their checkout or at the door to give customers adequate that they refuse cash payments.

Conclusion

If you’re a business owner who’s looking to reduce costs, take comfort in knowing that you can refuse to accept cash. Given that you’re setting the terms of the contract with your customers, you can choose whichever payment method you prefer.

However, you must keep in mind that you may be required to provide adequate notice to potential clients that you have decided not to accept cash payments."

But you only selectively quoted the information. It concludes by saying:

Conclusion

If you’re a business owner who’s looking to reduce costs, take comfort in knowing that you can refuse to accept cash. Given that you’re setting the terms of the contract with your customers, you can choose whichever payment method you prefer.

However, you must keep in mind that you may be required to provide adequate notice to potential clients that you have decided not to accept cash payments.

A possible reason for the conclusion is it isn’t practicable for many businesses to accept cash. An example being a business where purchases can be made online.

As outlined above, a business can apply a surcharge to a debit card transaction, but any surcharge must reflect the cost of that payment method to the business. Generally debit card merchant fees are the same as or less than for credit cards. A business can’t apply a standard surcharge across all debit and credit cards, if the costs to business are different.

And for Eftpos debit cards, a business can refuse accepting such cards, which occurs with every online business as EFTPOS cards can’t be used for online transactions - one of the limitations of the card.

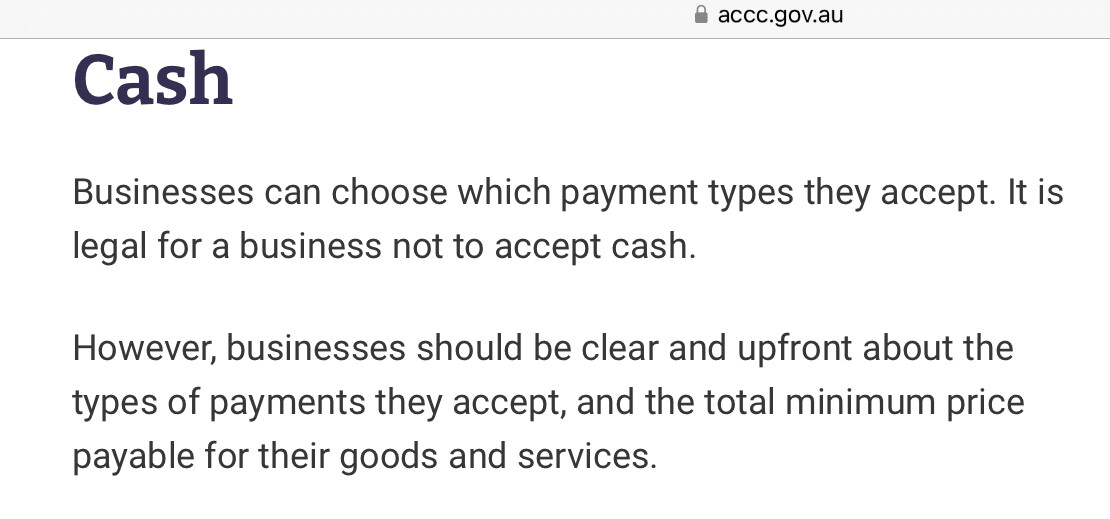

The business should be clear and upfront about …., and the total minimum payable for their goods and services.

My emphasis.

There are numerous different ways to express what one needs to do to comply. And numerous resources on the net all saying similar things. What the business should do ‘be clear and upfront’ it’s not an option.

Ok. I understand where you are coming from, but I was referring to the main part of the original topic by GHR, which is about face-to-face transactions in a physical shop, not online shopping.

The same applies to any transaction whether online or in person. The ACCC doesn’t have different advice for online or face to face purchases.

An example of not accepting debit cards is a small business which only accepts cash as they don’t have or use a digital payment platform. One that come to mind are stalls at market, some coffee outlets or a food vans - some of which only accept cash.

Leaving aside the issue of whether or not a business accepts cash for payment, the fundamental thing here is a price was quoted at $30.05 but it seems there is no way for the customer to actually pay that amount because a card surcharge is added.

That is deceptive pricing and contrary to the rules according to the ACCC. The displayed or quoted price must be what a customer could pay using at least one option the business provides.

I would like to thank all who have taken the trouble to respond to my issue. You have covered so many angles that I doubt there is any new one possible. You have given me much to consider.

What if the customer is in a situation where they cannot obtain the goods at an alternative place? (I liken this to the requirement of state government to provide a toll-free option whenever building a toll road).

At Commbank Stadium last night, we entered and then purchased our dinner. I had intended to use cash but it was momentarily easier to pull out the debit card. Later, it was regularly flashed on the main screens that the venue was cashless. In this situation how can I choose to get my dinner from somewhere that accepts cash? Once inside the stadium, I cannot exit, so they have me trapped. The choice I have is to go hungry if I wish to pay cash.

Is it adequate to inform your patrons of your cashless policy well after they have entered your premises and cannot choose an alternative? Isn’t that the purpose of pre-advertising, so that the customer can choose to go elsewhere?

Personally, I believe many retailers have used covid as an excuse to introduce what they have wanted for years - for everyone to use cards, and pay their surcharge for it. As a result, I use cash everywhere I can, and decline shops with cashless policies.

No answer, open to consider an alternative view point:

Worth reading all the fine print for the venue and facilities offered before purchasing a ticket. Once inside possibly all one has purchased is a ticket to watch an event. It could be eating a meal is an optional extra, the conditions subject to a seperate agreement with the vendor. Ticket holders choice and nothing to do with the venue that it does not suit.

If the venue promoted the meal facilities as an incentive to purchase a certain type of ticket or seat location, and one purchased with that intent? Open to argue misleading if the advice on cashless was not provided clearly and in advance of selling the entry ticket.

How did the booking procedure and promotional content present? Did the venue/event promote prominently one would be assured of purchasing a meal at the vendor you selected?