An article regarding how Australian consumers are getting trapped by credit card debt.

We always pay our cards in full every month but unfortunately, a great many others do not,

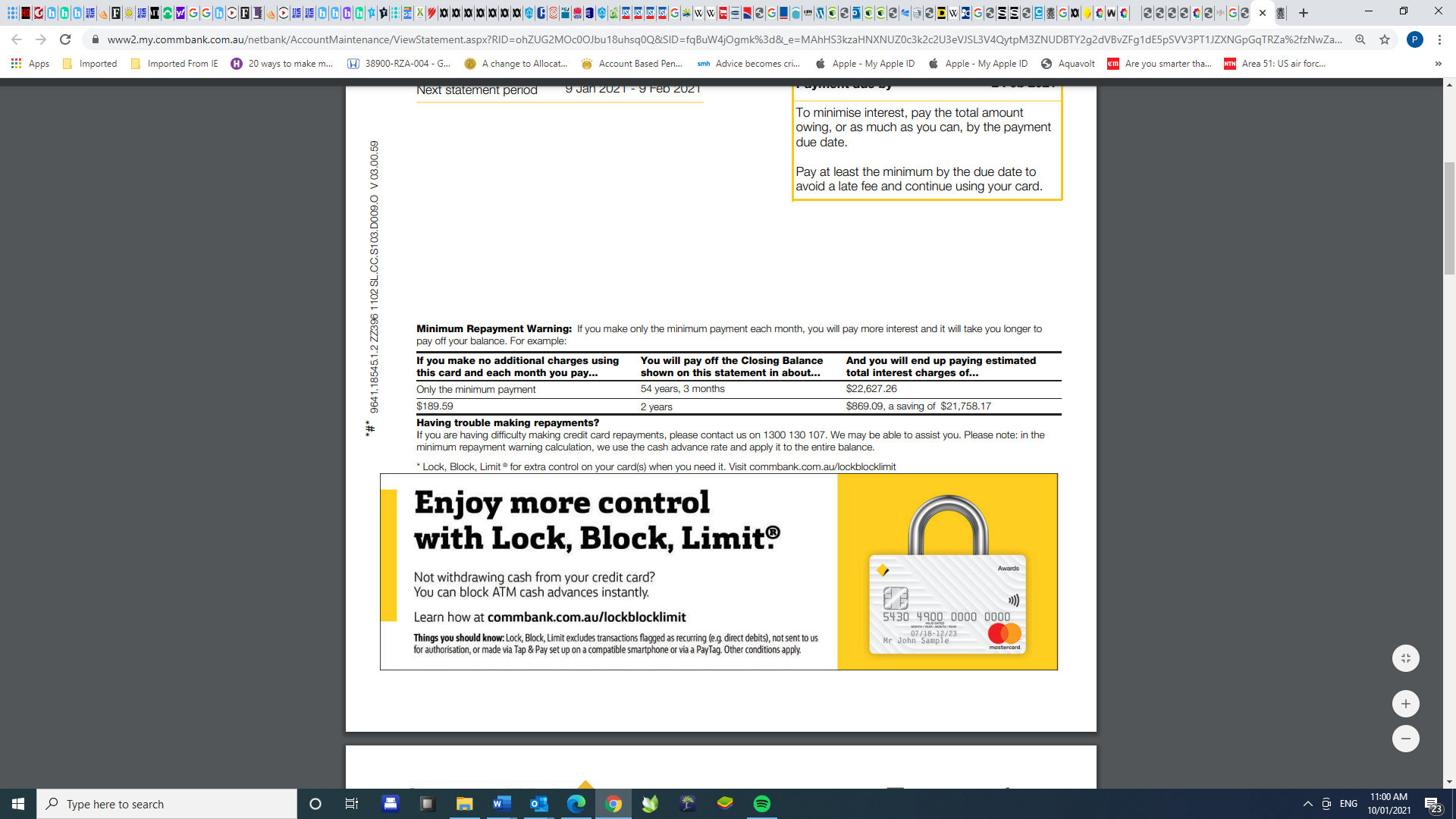

I paid my CBA MasterCard last week.It was just under $2,370 and the advice on the statement was that if only the minimum payment of $47.00 was made, it would take some 36 years & 11 months to pay off and incur interest charges of $11,696.38 but if $122.12 was paid, it would take only 2 years to pay off, incurring interest charges of $559.79 and saving $11,136.59.

After the Banking RC, surely the government could at least legislate that the minimum payment must be a realistic amount.

If consumers cannot pay a realistic minimum amount, they would obviously be much better off without these debt traps.

‘Which government’ are you suggesting?

We now know ‘which bank’!

Of course the banks and the credit card companies could act as suggested without any need for legislation.

It might be worth pointing out that the CC statement neglects adding in the costs of the fees and any other charges attached to the credit card for the 36 yrs and 11 months needed to pay the amount off. As these typically increase each year without any control over the amount, a customer could end of paying an added bonus to the bank in CC fees over the 36 yrs and 11 months similar to the total cost of the repayments!

Minimum payment is a minimum payment only. It is the decision of the card holder how much is paid and the minimum amount is the amount the banks/card company is willing to accept to reduce their own risks.

In positive light, the minimum amount does pay off the credit card debt, albeit in a very long time frame. If the debt wasn’t paid off by the minimum amount, then this would be very concerning.

It is good to see this information (how long it will take to pay off) on statements. If you are income poor and had to use the credit card for a big payment, then coming up with a large re-payment may be a bridge too far. A minimum payment at least shows the bank you are engaged with your debt.

Fortunately I have never been in that position. I have kept meticulous records and budgets all my life, payed off my card in time. But I know people who are hopeless at it and get knocked for six when the car rego, insurance and rates arrive together.

I can’t afford to pay mine off completely, but I pay 3x the minimum and I think its 18 months before its paid. Even when the card was maxed, the minimum was doable. I ignored the many entreaties from the bank to increase the max I could have because I knew that was way beyond anything sensible. As it is, I plan to reduce the max once its paid off.

Me too. I’m one of those with a big debt but because I own my home, I am able to make 4x the minimum payment, most months. I still use it for large purchases (eg the new washing machine and dryer, and I will be using it for a new fridge and stove). Once the major stuff is paid for, I’ll be paying it off completely and sending it back/cancelling that account.

An underlying issue is the world of finance is an industry, somewhat analogous to manufacturing or farming. Each has a product and in this case the product is money (specifically debt).

Marketeers and businesses alike have two jobs, one being to maximise profits, the other to maximise dividends. Whether the products are fit for purpose or should/need regulation is not their problem, it is our problem and thus government’s problem.

Ideologically writing, Australia is one of the more libertarian countries with hands off regulation, at least as much as government can get away with. Historically the ‘money lenders’ have been vilified but neither their ‘business ethics’ nor role in societies has substantially changed. Even in Muslim countries where profit from lending is contrary to religion they have found ways around ‘the problem’ so their end-case is not so different from non-Muslim countries that celebrate financial gains whether moral or amoral.

The discussion began with credit cards that have always charged top interest. CC’s are unsecured loans usually with the lightest weight application and approval process that could be applied. While 2 years old, this report should fill in some of the blanks of ‘the business’ and ‘its consumers’.

The banks justify (or try to) the high interest rates on risk.

From a libertarian mindset it appears the bottom line and intractable problem is governments seemingly refuse to differentiate the business of money (debt) from any other business regarding regulation. Those in power and in decision making positions consider regulating credit card interest to be similar to regulating the profit a business can make selling cricket balls, tennis racquets, or foods.

When customers willingly line up to partake of credit card debt, or double priced hand sanitiser, who should stop them or the sellers? Back to libertarian ideology.

We got into the trap using our credit card to stabilise our cash flow in very small business. Shouldn’t have been an issue, it was easy enough to pay it off as we were paid (irregularly) - but all it took was one large debtor to go bankrupt and leave us with an unpaid account, a couple of others to be a bit late and a downturn in business and now we have a lingering debt.

Luckily its on a low rate business card around the 10% mark…

It’s been there, being slowly chipped away for a year now, and I’m kind of getting used to just having it, if you know what I mean. Like the stone dragging behind.

As I have posted previously in another topic, the worst part is the ridiculously unrealistic minimum monthly payments which lock consumers into ongoing debt.

Why would the CBA offer me a minimum monthly payment which I would not pay off unless I lived to around double my current age which would make me vastly older than the oldest person who ever lived.

The Federal Government needs to act on making minimum monthly payments realistic so they will be paid off within a few years and not decades.

Allowing it suits those with uneven incomes whereby they may only be able to make a minimum some months, and say half or all of it on others.

A literate consumer should (but does not always) understand the ramifications, even though they are on the paper (pdf) statements. Many increasingly do not look at anything beyond the minimum payment, balance, and date due, regardless of whether and how they set up auto-pay arrangements.

For some the low amounts enable their lives, for others it is a trap. Does one address the trap at the expense of those it might help?

Financial literacy is the key, but as you post many times ‘you cannot help stupid’, but a corollary is you can always try. If you fail, you tried. We cannot take responsibility for 100%, we can only try to guide them and keep the more egregious, insidious lechers away.

The difference between the minimum amount and the higher amount is relatively small.

On my latest statement, the minimum payment was $50.00 as usual and the higher payment amount was $130.05 but the difference in repayment times was 39 years and 10 months in comparison to 2 years and the difference in interest was over $13,000 in comparison to some $600.

An extra $80 in the monthly payment is not much but over $12,500 in interest certainly is.

Whilst financial literacy is the answer, something still needs to be done to protect those who are not financially literate and who are not in a position to learn it.

I understand your point, but assume you have $1,000 per fortnight and needed to pay your annual vehicle rego of $763 and some prescription medicines on your card in a month. Take out rent, groceries, petrol, and insurance from your $1,000 for the fortnight. Might be pushing against $2,000 for the month. Your card bill arrives but do you pay the minimum to keep in good standing, default, or do better (how)? Next month perhaps no prescriptions and that ‘extra’ might also be paid on the card by the financially more literate, or spent on an extra carton to make the fairest point. I cannot help the latter person if they do not wish to be helped. Can you, without potentially handicapping the former?

I recceived a text message from CBA today “kindly” reminding me that my MasterCard is due to be paid in 3 days time, namely this Monday, which so happens to be a public holiday in Qld, NSW, SA and ACT.

Whilst we always pay our credit cards on time and in full, I would question whether banks can legally charge late fees to residents of a state or territory when they themselves have set due dates that fall on public holidays.

Qld TMR received a very well deserved smack around the ears from the ACCC some years ago for ripping off motorists with late payment charges when their registration renewals fell on a Sunday or a public holiday in Qld, and they were forced to refund all the monies that they had stolen.

Some might suggest that consumers can pay online or with telephone banking but so could the motorists that Qld TMR ripped off, and that did not cut it with the ACCC.

I would say yes. Days of human intervention for paying bills has gone and it is highly automated. Computers work 24/7 meaning it could be reasonable for a bill to be due on a Saturday, Sunday or public holiday.

One needs to check the payment system one uses also processes on Saturday, Sunday or public holidays as ones like BPay are tied to business days.

Paying with say a credit card within the billers website can be any day one choses…but if one wants to pay by phone or at Australia Post, it may only be business hours on business days.

I tried to find the articvle both on the ACCC website and by just Googling it, to no avail.

From memory, it was around 2012 because our son-in-law was one of the persons who were ripped-off and later refunded.

CBA has had Netbank for almost 20 years and Qld TMR has had online payments for at least a decade.

I would be very interested to read the article again regarding the result of the ACCC case against Qld TMR as I would expect that it would have set a legal precedent.