In the news today due to the productivity commission report into Super funds. Much of the commentary reports that the best funds are already very well know. That there are several good sources of this data. I have heard of Canstar doing this, but am not aware of any others. Is this a suitable topic for Choice, ie, a review of these reviewers of sources of Financial products and their quality and independence.

Related to this is how easy and costly is it to move from one fund to another, (say from industry fund to retail) and how easy it is to switch funds within a Fund (from cash to property or ethical)

If you want to rollover from one fund to another, most times the fund you wish to rollover to does most of the work. You sometimes need to provide a bit more detail but it isn’t normally onerous. It comes down to mostly that people don’t ask. Costs are normally not high but funds can and do charge for establishing a policy.

Switching the way your funds are handled are very similar unless the particular investment fund has a set investment profile. Then this may require rolling over from that particular investment stream to a new investment stream, that depending on your Super business can cause them to charge fees for the change but some do not.

@grahroll is right on for ‘modern’ super, but some people still have ‘archaic’ that had huge exit fees. Not all of those ‘fine respectable’ companies that sold such super plans for decades are happy to relinquish their trailing fees nor high costs, nor ridiculous exit fees.

Bottom line is if you have a decades old fund, read the PDS about its fee structure. If it appears to have draconian fees give them a ring to see if it can be sorted to a reasonable level. If an old one can be sorted, or you have a ‘modern’ fund, it is usually as easy as a single form, albeit sometimes having a few pages.

My experience is that it can be very easy to (consolidate) move super from one fund into another (existing fund). Having done this many times, over the past 20 years, it has become easier each time. It only needs a phone call, or perhaps an online chat session to set the wheels in motion.

I’ve never had to pay a fee or loose any super in the process. The fund I have been transferring to has provided the forms by mail. Typically I may have needed to provide a certified copy of my ID (EG from a JP), and paid a few dollars to return the docs using a priority tracable mail service.

In respect of asset allocations within funds the rules seem to vary too much for there to be one simple answer. Some allow free switching or changes with limits on how often. Others based on your age lock your allocations to their own rules.

Typically my experience of industry funds is that they are the least flexible, but best performing. The retail funds with a few exceptions have been the most flexible, but much more variable in their performance.

I’ve had approx 20 different super accounts in a full lifetime of employment. The system certainly needs reform in many areas, providing it is for the increased benefit of the customer and not the provider?

My 19 yr old granddaughter needs advice for her Superannuation. At present she’s part time/casual. It’s a mine field, fees, ethical, returns. I would love feedback from anyone dealing or have dealt with the best options. Cheers Rosemary (71 yrs)

Please note there are a number of topics about superannuation on the Community, discoverable using the Community Search tool. Those topics have links to various reports that should be helpful.

You are essentially asking for investment advice which is beyond the scope of Community members as none of us (AFAIK) are licensed to provide financial, investment, or legal advice. The other topics are about the mechanics of super, not investments.

Government has recently produced a league table of the best and worst performing funds and this government web site should prove helpful to educate oneself.

and from Choice

There are also some helpful commercial sites such as

This is not financial advice, or recommendation for a particular super fund. Our 3 children have had to navigate the same issues over the past decade. All started working part time in retail or hospitality at the lowest of levels.

All at different times have been able to select well known industry funds with large memberships as best suiting their needs at the time. Unfortunately not all employees have a choice of fund, depending on the industry, and relevant award agreements.

Their experiences reinforced the benefits of choosing a super fund that had low fees and costs. When starting out your super contributions are limited, because of the low earnings. Higher fees can quickly wipe out all contributions or a major portion. For each the returns from a fund appeared less important than the total amount held in super. What they lost in fees when starting out was their greatest complaint about the super system.

Review as much independently provided content as you can.

Your granddaughter will want a Superannuation fund, ie, she is in the early years of what is termed ‘Accumulation’, whereas you Rosemary are probably in the Pension or ‘draw down’ phase.

The last year has been a bumper year, ie, post COVID, so the actual growth figures are not typical of the general trend, but, so looking at the 5+ year performance is possibly a better, but you may miss out on good funds that have only been around for a short while.

I think young people are more aware of the need for more ethical and sustainable funds, ESG is the acronym that may help: Environmental, Social and Governance.

One thing to keep an eye out for is the basis of any recommendations provided generally, rather than specific to ones circumstance.

Canstar for instance rate their funds according to circumstances of a full time employee.

EG From Canstar’s advice on choosing a super fund. Prepared on 24/05/2021 based on data available as at that date. Scenarios begin at the start of the 2021-22 financial year and are based on a 25-year-old with a starting balance of $25,096 (per the average from APRA’s Annual Superannuation Bulletin for a 25- to 34-year-old) with a starting gross annual income of $74,516 (the median figure for an employee working full-time in their main job per the ABS’ Characteristics of Employment data), growing 2.5% annually (per the RBA’s inflation target),

This does not align with what might be the actual circumstances of an 18yo starting out in part time employment. I could not find any Canstar modelled scenario specific to that need.

I’ve had to work through issues with one of our sons, where the employer super fund was taking most of the contributions for the year in fees. It’s not a pleasant feeling. Understanding the fee structures and comparing funds on that basis aligns with the first item on the Canstar check list. The effective gain or return is irrelevant if at the end of the year there is only $1 left in the account.

From the ABC report linked to the APRA performance report.

For someone starting out and earning $10,000 in the first year with $1,000 transferred to super. Which of the above funds would provide the best outcome?

I’ve highlighted 4 with lower fees. The differences in return based on past performance are just 0.7% or $3.50 on the average balance for the year. The difference in fees between the lowest and highest of the 10, a not inconsiderable $302 for the year. I’m not offering financial advice. It’s just an observation.

An 18yr hospitality worker gets a minimum about $28k pa.

I’m assuming an 18yr old with an interest in Super want links to learn for themselves, maybe with help from granny.

The two links I provided give general info about what to consider, eg, Return and Fees. My understanding, in general, is the major portion of fees comes from a % of your total holding, free in the early years when the holding is low, hence return is most critical in the early years.

The majority of general advice assumes the fund member has a relatively large balance EG $25k or $50k etc as a starting point and regular income close to average earnings.

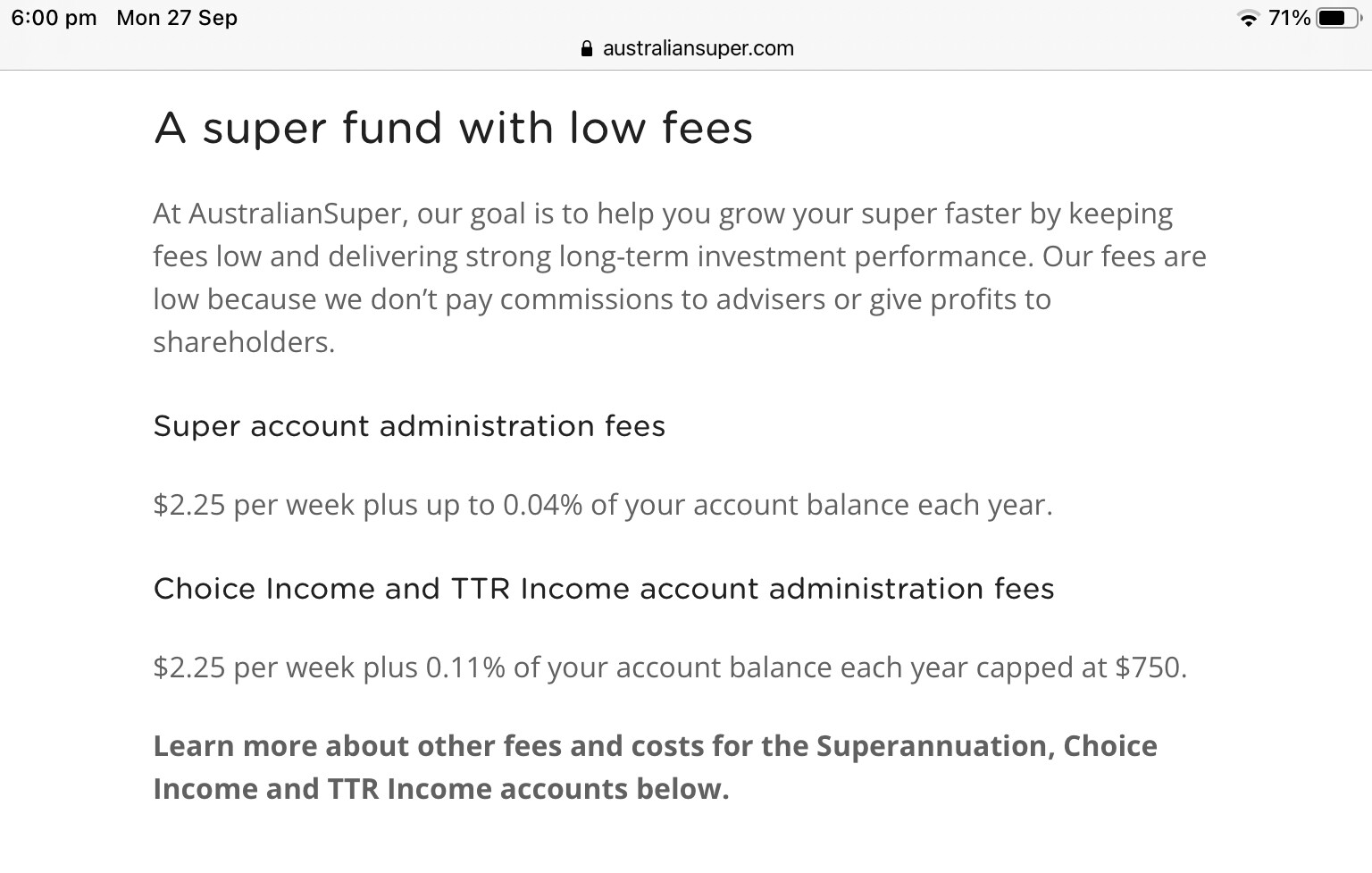

Edit - added link to the current fee structure (from the pds) for Australian Super. Each fund produces a similar document. Note for account balances of less than $6,000 there is a legislated requirement to refund any fees paid above an annual cap of 3%.

There are a couple of considerations relating to fees.

For accounts with a balance of less than $6,000 the total annual fees are limited to 3% of the balance.

Fees can consist of two components, although some funds might not charge the first amount.

a. An account fee charged regardless of your balance e.g. the $2.25 per week charged by Australian Super; and

b. An amount calculated as a percentage of your balance.

For someone working limited hours and with a nil or small previous balance, you might want to choose a fund that doesn’t charge an account keeping fee. However, the same fund might not give the best fee outcome when the balance increases. For this and other reasons you should ideally review the appropriateness of your fund regularly.

As you have mentioned, the amount of fees charged is only one of a number of considerations when choosing an appropriate fund

It’s of considerable benefit. The two reference sites you linked are very useful for anyone with a modest balance through to retirement. It also informs those starting out about what to look out for into the future. A criticism of Canstar and the ABC, but not intended as personal, the immediate needs of first timers were not specifically addressed by Canstar or the ABC in their material.

@Glenn61 has responded appropriately and added that there is a refund of a portion of the fees where the fund has a balance of less than $6000 at the end of the year. I missed this. My error.

This returns a portion of the fees deducted during the year to the starting balance for the following year. It is based on a cap on the combined fees of 3% of the fund balance at the end of the year. It was legislated and introduced as 01 July 2019. Choice provided a summary of the changes.

I’ve edited my earlier reply to point to a more complete example of the Australian Super fund fee structure. The 3% cap is mentioned only once. It’s in the fine print. The full fees are still deducted during the year. The greater the fees the greater the impact on performance.

If you want excellent returns on your investment (who doesn’t?) and to know that your investments are doing good, I suggest Australian Ethical. I started investing with them 20 years ago, and my experience has been all positive.

The main reason I moved all my super and pension to AE was that I realised that putting my money where my mouth is was the best way to effect ethical changes socially and environmentally. I also realised that, despite our current government’s reluctance to combat the greatest existential challenge our world has ever faced, that’s where the money is; and that has turned out to be true. Industry in general knows that the future is in renewable energy, environmentally safe practices, better human health and non-exploitation of workers; hence shares in these companies tend to do well.

Super funds have huge amounts of money that can be used for good if invested wisely.

But don’t take my word for it. Check out these web sites:

Your particular fund suits your interests in various “ethical” areas, the definition of which are really yours to define.

Whether your super fund does well compared to others is up to the fund managers in investment decisions.

And of course management fees.

Not too sure about that as something that could be demonstrated as factors in investment returns to date.

Thanks Harry. I think it is great that the Ethical funds are performing well. Also the link to the UK site.

An aspect I am looking at is using ‘funds’ as part of the SMSF. Many SMSF want the flexibility to have direct investment, but that shouldn’t imply they are opposed to using funds. An issue however, is many of the better performing, and ethical funds, only have Super and Pension options, ie, no Managed fund. The latter can be important in SMSF, as the taxation/draw down aspects can be included within the overall SMSF tax/draw down.

I’m a real novice here. Are you saying that within a SMSF you cannot invest in a managed fund? We are looking to do just that and need to find the right one.

If you are a novice in relation to SMSF, it is worth getting independent advice on its establishment (inc. whether it is best for you), rules, reporting requirements etc, so that you don’t fall foul of super rules. I would not be relying on online views or opinions of laypersons.