That’s good advice indeed. The SMSF is already established. It is not for the faint-hearted. We will be shutting it down as soon as possible. We just need a good investment vehicle in the meantime.

3 Likes

Not saying you can’t invest managed funds in an SMSF. Almost the opposite.

With a SMSF, you manage all the taxation, investment and payment rules.

Industry Funds, are relatively good performers and also with lower fees, so they are attractive fund choices. However, most, maybe all, have only two broad fund choices, Superannuation (accumulation) and retirement. These two types, the fund managers, manage the tax, investment and payout rules.

What SMSF need is ‘Managed fund’ as their tax, investment and payment requirements are not part of their Fund managers role, hence they can be an important component of a SMSF portfolio.

Industry funds don’t seem to have the Managed fund option that other retail fund do.

3 Likes

There is an excellent ‘Dummies’ book. It isn’t called SMSF unfortunately but is totally focussed on them:

“DIY Super for Dummies”.

It covers every aspect from setting one up to dismantling it. All of it can be done without advice. But most don’t and it lists great sources for each aspect. Eg The Deed needs a lawyer, the annual audit needs a specific type of auditor, and even lists the things that they might find wrong and the consequence of each.

All in easy to understand terms.

I borrowed a copy from my local library.

1 Like

Most funds have at least 3 or 4 options often called ‘default’ (balanced), aggressive, conservative, and cash, each with differing risk-return profiles. My retail fund has a 47 explicit fund options including the basics, comprised of their own funds as well as those from other fund managers whose products they represent.

The funds range from flavours of growth, income, ethical, cash, property, geared, international, and the holder can define their own mix and change at will, although having to wear the sell-buy spreads.

edit for clarity: The major thing missing is the inability to include individual shares or properties - every investment regardless of the ‘super product’ being in accumulation or pension phases is in the account holders personally selected mix of the funds on offer.

2 Likes

I agree with you. I think the finance industry could use better, different terminology.

I think of funds as each ‘flavour’ as you refer to them has a Fund Manager, I understand usually a team of investment experts, who choose specific investments, which they change over time in an endeavour to increase their profitability.

As investors we can access a selected flavour fund by 3 different routes:- Superannuation (accumulation), Retirement, and as its most basic Managed. But the underlying flavour fund is just a single fund that delivers the same investment outcome, but the 3 routes have different tax, investment and repayment rules, which their administrator must apply.

1 Like

APRA has released its next round of assessments. The links are contained in this article.

Interestingly I have a Perpetual Super account consisting of self-picked funds, none included in the ‘bad list’ and that have been a quite good performer for the past 20 years. One needs to pay attention to everything, not just the headlines.

For those who need to have a fund they do not need to pay much attention to these reports are stellar. For the more engaged they are good information. For the savvy investor? Happy to help fund such things for the rest through my taxes

edit: it is interesting marketing that Perpetual has a few duds and proudly markets their wares with the phrase …investors looking to access Perpetual’s proven active management expertise. For some it might be proven as wanting, for others it seems to work a charm. On average?

1 Like

A following report reinforces it is not just about fees, and taking some responsibility above the default MySuper options can have a dramatic impact on balances. All funds/options are yet to be included especially the mix and match options.

1 Like

2023 APRA Superannuation performance report insights paper

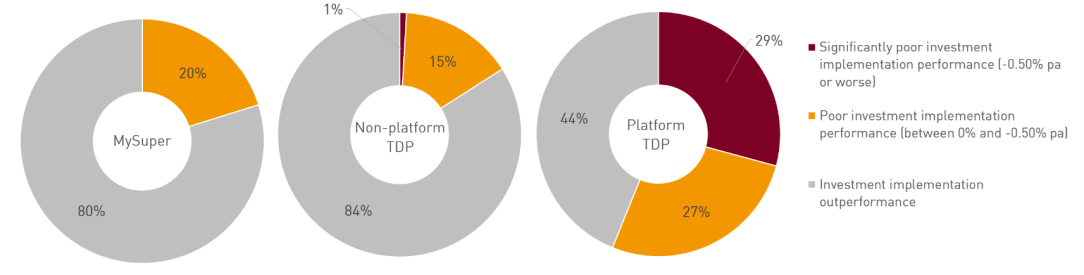

Platform TDPs have been noted to be of concern particularly as their fee structure may be quite high and a significant number producing under-performing results for that cost. 56% of Platform TDP had poor to significantly poor investment implementation performance. MySuper funds had 80% who had outperformance and 20% had poor performance, non-platform TDPs had 1% significantly poor performing funds , 15% poor performing and 84% achieving outperformance.

1 Like

I haven’t read anything before about TDPs, now know the acronym stands for Trustee Directed Products, but that doesn’t mean anything to me.

What IS and ISN’T such a thing, what are their characteristics? Without more context, the two subsets of TDPs, platform and non platform are equally meaningless.

Are conventional Super and Pension products TDPs?

If TDPs are a subset of Super funds, what are the other subsets of funds known as and their characteristics?

1 Like

Three links that may help explain the differences. Some Superannuation Companies may have a mix of MySuper and TDP funds. Basically a TDP is where a fund trustee has at least some direct control of where money is invested. Many of the Super funds we are usually familiar with while they have trustees, the fund investment is managed by investment firms not the trustee/trustees. These type of funds are not TDP ones.

MySuper (the default choice if no fund is selected by the employee)

TDP funds

Information that may further help explain the differences (it also lists the Trustees who controlled the failed funds…note many are retail fund trustees)

Thanks for the links. The Superguide links, only let you open a few before they request membership, @$60. Apart from that some interesting info. Still not sure I really understand the difference, but it will do. WRAP funds seem to examples of TDP, many which have failed the test.

In the past I have written to Choice and gov’t about WRAP funds. The idea behind them is good, I think of them as a stepping stone to SMSF, but they are often linked to fund financed FPs, and all need a FP to take even the simplest action eg, switch.

@BrendanMays An aspect that I think Choice needs to take up is the performance testing of Pension phase funds. This is probably more critical as retirees seem to have the most to lose, and the least amount of time to do anything about it.

Another very interesting statement from Superguide is the industry has determined that 60% of the fund growth actually occurs during retirement, ie, only 40% during the accumulation phase. Yet, the constraints on the retirement phase limit, or make change very difficult. Despite most being in retirement for decades.

For performance testing of Pension phase funds to be practical, their current inflexibly rules would require significant change. Important as the consequence of the test is to get rid of poor performers, and direct account holders to alternative, better funds. That general flexibility ought to exist in its own right to aid the accumulation, the 60% of accumulation that occurs during retirement.

3 Likes

Thanks for the suggestion @longinthetooth, I’ll pass on your comments to our team working on superannuation issues.

2 Likes