Recently I paid a security deposit at a hotel using my ING Visa Debit card. The hotel told me it would be released after 5-10 days. It hasn’t been so I rang ING. They told me that Visa has changed conditions and only release hotel and car rental deposits after 31 days! Though if you convince the hotel to email the bank requesting release they may do it!

Anyone know the background to this? Has ING given me accurate info? Is it only a change by Visa - or Mastercard too? Does it affect both credit cards and debit cards?

Has has anyone else been caught out by this 31 day hold on their funds? At least it in my case it was only $200 and not a car rental deposit which can be thousands of $$$.

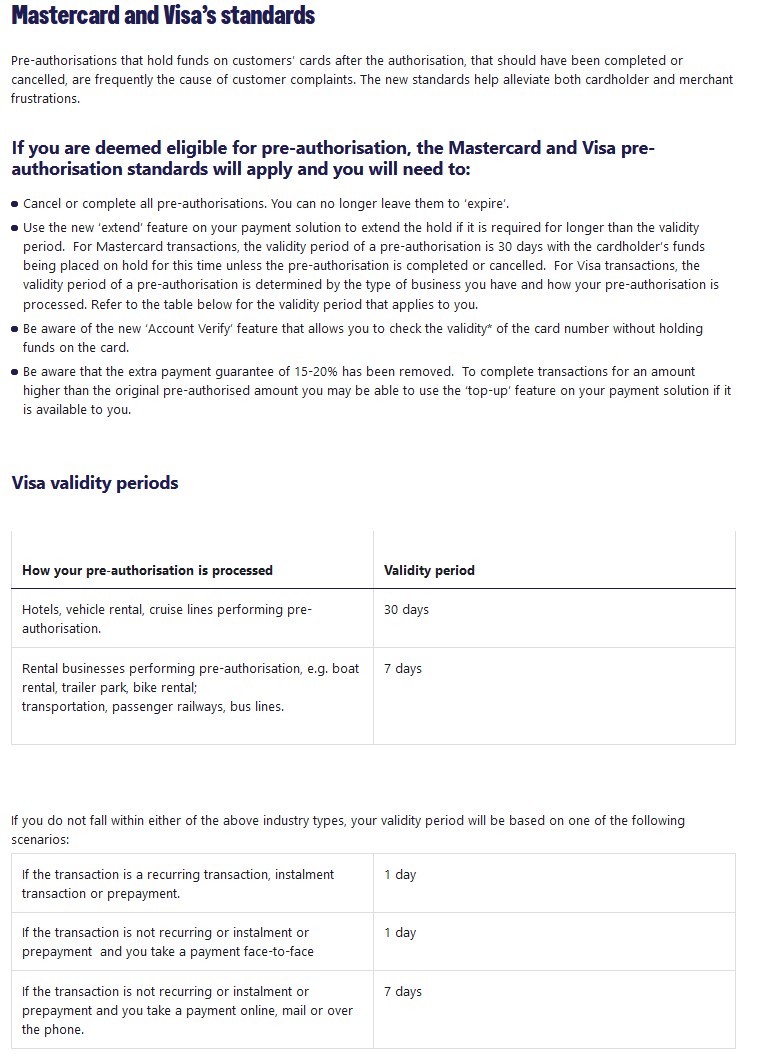

I believe you are talking about pre-authorisations used for the security deposit. For lodging and car rental pre-authorisations, these have a currency of 31 days before they lapse, earlier (24 hours after reversal is instigated) if the pre-authorisation is reversed by the merchant. See…

If a business indicates that the pre-authorisation is released in 5-10 days, then the ‘hold’ on funds should be removed shortly thereafter. If it isn’t released after 5-10 days, either the hotel didn’t reverse the authorisation or the card issuer doesn’t process reversals regularly (it might be done say at the end of month to coincide with issuing of statements).

I would check with the business who instigated the pre-authorisation first to make sure it has been released. For car rentals, they may be unwilling to reverse the pre-authorisation quickly as they may wish to wait to see if any tolls or fines occurred during the rental. This can take some time for the machinery of bureaucracy to issue fines/payment notices. As a car rental pre-authorisations may be a substantial sum on hold, a car rental company may be willing to do a partial pre-authorisation release to cover any further liabilities.

I am interested to know why a pre-authorization would be needed for a deposit. That would be a transaction that should occur in near real time, whether by credit or debit card facility.

The required money or available credit is there at transaction time, or it is not, and the transaction will succeed, or fail. Right there and then.

A pre-authorization is for some future charge, such as final payment at end of accomodation or return of rental car.

Maybe I am missing something, but my understanding of a deposit is a part payment of what becomes the final full payment.

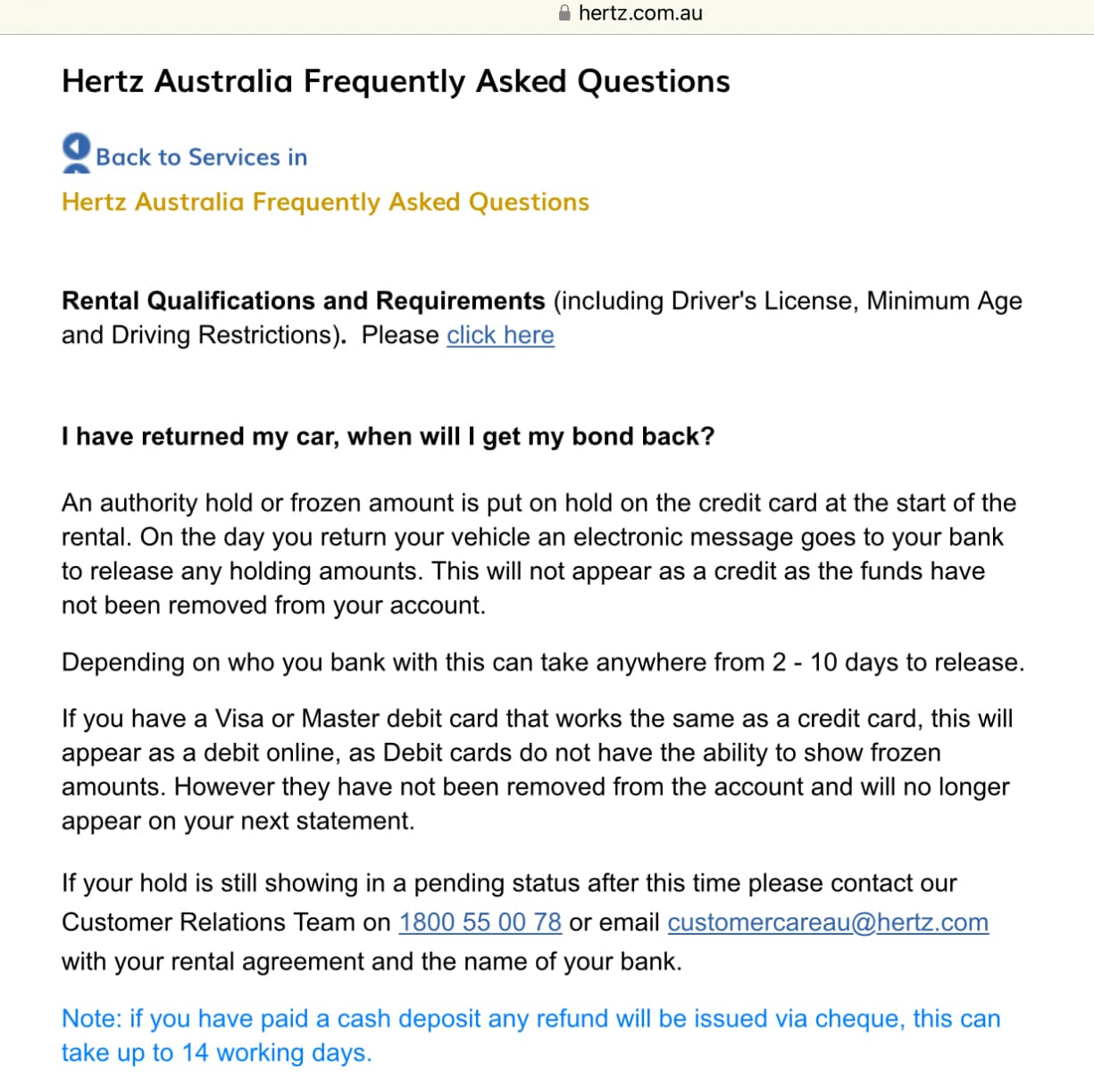

It is best to look to the Car rental business web resources. In this example Hertz release any hold on a CC on the day the car is returned. Similar for Visa and Master debit. What happens after the release is notified is up to your bank and chosen card service.

If a business is going to retain a hold after the last day of use or occupancy, should it be advised clearly in the booking terms and conditions?

A further question to ask is of a business identifies after the fact that there are additional charges due, does it have a responsibility to inform the customer before or at the time of adding the charges?

P.S.

I’ll suggest consumers are being encouraged to take the convenient self service virtual or non contact check out or return. As a one time past employee who travelled on the company account, the norm pre Covid was to ensure all accounts were finalised on the day. Corporate accountants give no quarter.

One only needs to look to some of the issues arising from the Gig Economy to suggest there is a lack of adequate consumer protections where there are charges added with their knowledge and agreement.

It is a security deposit and not a deposit for part prepayment against a booking.

A security deposit covers incidental charges such as damage, other services, fuel in case there rental car isn’t full on return, fines etc. These are above and beyond the charges paid for the service such as car rental or accommodation booking.

A deposit for a booking secures the booking and offsets the total charges for the services. For example, at the time of booking a hotel may ask for a deposit of 1 nights stay. If one stays 3 nights, the other 2 nights are paid on or after check-in.

The amount was a security deposit that was kept in case I trashed the room or stole the kettle. And yes it was a pre-authorisation on my card which sits in my account as money I cannot use until it’s released.

My objection is not that it was taken, but the length of time for it to be released. Hotel said it would take 5-10 working days but “depends on the bank”.

Thanks PHB for the Visa policy - I now know what’s standard for future reference: ie 31 days. In this case, the hotel has not yet responded to my emails about whether they have told bank to release it.

So in reality, we are talking about a security ‘bond’, not a deposit. Except it is a claim on available funds should it be needed in the future, not an actual transfer of money from one party to another.

Calling it a ‘deposit’ is wrong. A deposit is an initial part-payment on the eventual final payment.

The title of this thread is wrong to talk about releasing a deposit when none actually occured.

Is a further consideration consumers have different levels of financial education/sophistication. Hence when looking to explain transactions the terms and concepts most familiar, easiest to use and relate. Similar might even occur with less well informed counter staff.

As much as it might grate it’s informative to occasionally listen to talk back radio. John Laws or Ray Hadley (2HD) or …. A great many of us like to keep it simple is what I take away. It also illustrates why we need consumer protections that are effective for all of us.

P.S.

A ‘security bond’ in my experience is a hard cash transaction. Not sure it’s a helpful reference?

More effectively pre-authorization is a ‘lien’ against one’s assets to repay a debt owed. In this case by money transfer from recorded account details with a reservation on those funds should the debt be called in.

No, it is a security deposit. The term security deposit has been defined and used when there are potentially future unknown liabilities, to cover such liabilities. Whether it is the travel industry, for tenancy or mining, it has the same meaning. It is also defined in some legislation such as that relating to mining (security deposits to cover rehabilitation liabilities). Security deposits can take different forms, such as cash, bank guarantees, bonds, credit card pre-authorisations or some other asset of value.

In the past in the travel industry, cash security deposits were common. These were provided on commissioning of services, held by the business and returned on cessation of the service. Many of us possibly remember in times gone by waiting in a hotel reception while floor staff checked a room to ensure there was no damage or what in the minibar was used before departure. With credit/debit cards being held by almost all consumers, pre-authorisations have become the norm especially when contactless checkout/cessation of services became more common or possible (such as a key drop).

Because I use the dictionary definitions of the word, noun, not verb. If there is no actual transfer of money, it is not a deposit by any definition I have found.

It’s not a lien either. There’s no debt owed in the normal course of the transaction related to the authorisation. It’s an authorisation for payment of a potential debt that should not arise in the normal course of the transaction - i.e. as a security. Hence for a credit card, it reduces the available credit without raising a debit transaction on your account balance.

They can call it whatever they like, but with a debit card, it’s your money that’s reserved rather than a reserve against available credit.

I suggest semantics are a side issue to how these pre-authorisations work, and especially the time it takes for them to lapse or be removed, which is the germane point.

The following from the ACCC provides some illumination, or not at all depending on the answer one is looking for. It covers some aspects of charges against credit cards, deposits, etc. There is no comprehensive reference to holds against a CC or Debit Card. How ever pre-payments, holds on cards or pre-authorisations are labelled, the ACCC often refers back to the Terms and Conditions of the contract agreed to at the time of booking. The usual caveat of unfair terms in a contract applies.

‘https://www.accc.gov.au/system/files/Travel%20%26%20accommodation%20-%20an%20industry%20guide%20to%20the%20Australian%20Consumer%20Law_0.pdf

Perhaps consumers might call it out for what it really is, “some customers can’t be trusted protection”. An impost on all due to the failings of the few. For consumers there is no reciprocity where a charge can be made directly against the account or credit of the providers in the instance they fail to meet obligations. It’s up to the consumer to seek support from the state and territory Consumer Protection agencies and courts. Whether it’s a level playing field, the ACCC doc is worth a read. I’ve appended a link to some of what Choice has to say for those looking for a more useful guide on accommodation.

Your examples are about actual deposits. I believe this topic is about pre-authorizations which do not normally turn into actual money transfer, and failure to clear them in a timely manner.

As such, they are liens, not deposits.

Pre-authorisation (otherwise known as ‘deposit’) is a pre-determined amount that is put on hold, on the nominated card, at time of picking up your rental vehicle."

Stripe talk about it as a type of security deposit

“The whole idea behind pre-authorization payments is to make sure customers are paying for goods and services. Once a pre-authorization payment has been made, the funds for that payment are unavailable until the payment goes through. Think of pre-authorization payments as a sort of security deposit; if a customer decides they don’t want to pay, a pre-authorization payment allows you to get the money that’s owed to you. Not only does this ensure you get the money you’re rightfully owed for goods and services, but it can also save you a lot of trouble when it comes to payment processing.”

and

"Car & Vehicle Rental

Car and vehicle rental companies can use stripe pre-authorizations to make security deposits before a client takes the car, and refund it when they bring back the vehicle."

Regardless of the various didactic definitions of the pre-auth, the hold of 31 days does seem excessive for auto-release when a rental has been completed. Most pre-auths where the rental or other reason has created the pre-auth, are automatically released 1 to 7 days after the pre-auth date (some businesses have longer periods before pre-auths are auto released), if not cancelled immediately by the business. If a pre-auth is cancelled by the business the release is almost immediate. The hold period is set usually by the Merchant Classification Code (MCC) and most are set for 1 to 7 days for the auto release.

However, VISA have changed their timings and WESTPAC do note this on their website, though the businesses are no longer allowed to let the pre-auth auto-release. The business must either complete the transaction by taking the money or cancel the pre-auth when the rental or other transaction is completed.

I would think the longer delays allow a business to have the damage or extra charges assessed properly before the pre-auth would auto-release. However if there is no damage or extra charges to be calculated/assessed then the pre-auth is required to be cancelled and once cancelled the funds should be almost immediately available to the cardholder. The business that is holding the funds should be contacted to ask why they haven’t released the funds, is there some damage or cost that has not yet be assessed/calculated.. If there is no reason, then the cardholder should request the cancellation and a complaint should be made to VISA/MasterCard and to the issuing financial institution about the failure of the business to adhere to the requirements.

Budget’s incorrect use of the term ‘deposit’ noted. I prefer the dictionary definitions.

But being able to hold onto liens on accounts possibly weeks after a transaction has been completed should not be allowed. Also, the amount pre-authorized should not exceed the expected final charge.

So what is it with rental car companies being able to put a $5000 hold on your funds or credit limit, when the rental is only expected to be a day or two? Why not just put an insurance charge as part of the rental?

Under the current requirements, if there is no assessment of other costs being done, then the pre-auth is to be cancelled. A business that is just allowing the pre-auth to auto-release is in breach of those requirements.