Edit: New readers to this topic can read through or skip to post #38 where it continued in Feb 2022.

Choice reviewed credit card travel insurance in April and this was very useful. However, for the future, I suggest more commentary on pre-existing medical conditions. For many (older) people this can be the major consideration. For example, the NAB (QBE) policies that got the highest score cover NO pre-existing medical conditions under any circumstances, not even after medical assessment. For many people that makes them useless.

Thanks for the feedback @Jumbuck . The cover for pre-existing conditions for credit card travel insurance varies widely, as it does with standard travel insurance policies. You can get an overview of the cover by selecting a few products to compare or clicking ‘Compare all products’ in credit card travel insurance review and scroll down to the ‘Pre-existing conditions’ section.

Aside from whether or not the insurers might provide cover we do have trouble uncovering the adequacy of their cover for travel insurance. Once you’ve submitted an application for cover, we’re not sure how they’re assessing it and whether they’re subsequently providing adequate cover. If anyone has more information on the travel insurers cover for pre-existing conditions, please feel free to share.

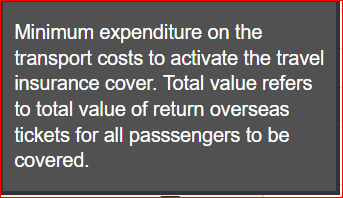

@JodiBird, I found that interesting since I have used my card policy for international travel for years. However I am not sure it is as precise an overview as some might expect. Noting pre-existing conditions were the topic and the summary comparison line items for pre-existing conditions each have references to the PDS, a related example of how things can be unintentionally distilled into mis-information is that the Westpac QBE policy is stated to require at least $500 in air fare through a generic “information” button that displays

and that is how some policies must be activated, but the text in the Westpac QBE policy is (with bolding added for clarity, and applying individually to each of the “card holder” and “spouse and dependent child” travelling under the card policy.

“You (or in another clause “Each spouse and dependent child”) spend at least $A500 on your prepaid travel costs (i.e.your travel costs that you pay for before leaving Australia)and you charge these costs (e.g. cost of your return overseas travel ticket; and/or airport/departure taxes; and/or your prepaid overseas accommodation/travel; and/or your other prepaid overseas itinerary items) to one of your following eligible credit cards issued by Westpac:”

With the text “Each spouse and dependent child” it is not obvious if Westpac or QBE are promoting polygamous relationships although the lawyers obviously have it in their legalese for clarity.

I have recently learned the hard way that pre-existing medical condition rules also apply to any one you are travelling with or care enough about to need to cancel your travel when they get sick. My recent cruise plans got cancelled when my partner was admitted to Hospital for a condition he had once before, several years ago. My insurer and my credit card insurance would not refund my 100% cancellation fee because my partner’s condition was pre-existing. So if anyone in your family becomes unwell and you need to cancel a trip there is a good chance you won’t be covered. This applies to all travel insurance apparently though the definitions of pre-existing conditions seems to vary.

I travel on an ANZ Platinum card with QBE backed travel insurance. I have to apply for assessment of an existing condition. It costs $75 for the assessment and has been approved 4 times for me. It relates to heart surgery (quad by pass). The only time I was deferred was within 12 months of the operation. They wanted to wait 12 months before the assessment. I think it is good cover.

The other big issue is over “mental health”

It appears that even if you have at some time in the past seen a psychologist for any reason at all This can be determined a pre-existing “mental health” automatic exclusion

Once you are over 80, as far as I have been able to discover, there is no credit card insurance. Travel insurance gets harder and harder to find, and more expensive every year. Should we stop travelling!

@habari4u2 - that’s a big problem and one we’ve discussed around the CHOICE office before. Interestingly, the Financial Ombudsmen recently ruled that mental health exclusions like this are unlawful.

@pmslaytor, thanks for highlighting this issue too.

The “Can purchase be made with frequent flyer points” line on the Choice review can’t be trusted. The Amex Platinum Edge card, for example, only allows you to use cash or Amex Membership Rewards points in order for the insurance to operate. Membership Rewards points, in their own right, are not a worthwhile way to buy flights and are not airline points.

The main value of the Amex cards is that you convert MR points to the points of the airline or hotel that you want to use. When you use those frequent flyer points for a trip, it is not covered by the insurance. The table really should mark that as a “no” for all practical purposes.

So as per the AMEX PDS “Cover is effective when You pay the full fare for a return Trip … with American Express Membership Rewards points.” But not, as you point out, if you convert those Rewards points to Frequent Flyer points and then use those Frequent Flyer points to purchase the flight.

It seems to me the title of that column in the review is misleading, it should instead be called ‘Rewards points’ and the description should be explain that cover will be activated if credit card rewards points are used to purchase the flights (not frequent flyer points).

I’ll check to see if it’s a similar scenario for other cards, I suspect this is the case.

I have found the ANZ Platinum card cover through QBE pretty good. I have a pre-existing conddition. I pay $75 for that to be assessed. So far they have covered me 4 or 5 times. When my travel was initially interrupted by the condition, they paid me the relatively small amount involved in cancellations. Read the consitions and see if it suits you.

I have been travelling with this insurance as well and have had very good experience with a couple of claims relating to an accident and rental car cover, QBE was efficient in processing the claims and refunded all applicable expenses (once I had to ask for an explanation for expenses not covered and on review I got everything refunded). My husband has recently developed heart problems and I was worried about cover for our next trips - the process you outline looks simple and fair. Let’s hope this remains when ANZ changes their insurance provider to Allianz in April this year.

This raises an interesting question - what constitutes ‘pre-existing’?

If you have a condition that is ‘resolved’ but something with the same definition happens again? What if you had a bad case of the flu? and get the flu again - same diagnosis so pre-existing? clearly not and maybe thats an easy one to argue, but it seems to me there might be many others that are less clear. Chicken pox/shingles? What if I have a skin cancer removed on my left pinkie and another bad one develops on my right knee? I’m clearly not a doctor, but I get the sense there are some easy ‘outs’ for insurance companies that might not necessarily be congruent with medical science.

To my understanding, almost anything can be considered pre-existing by an insurance company. Getting a medical assessment from your insurer can help give you the ‘all clear’, and even though it’s a hassle, it might save a dispute in the event of a claim.

Always read the PDFs. We have an ANZ Platinum Card and the cover is excellent…although we have never claimed so will see if worth the paper it is written on if/when that day ever comes.

We have saved $THOUSANDS on not buying medical insurance which covers the same things we get for ‘free’.

I have just been advised that the travel insurance provided by QBE for the NAB platinum visa is only for the primary card holder but for secondary card holders it only covers you while you are travelling with the primary card holder. So if I use my card with my name on it to book separate travel I will not be covered.

That was good you pointed it out, but that is a standard limitation, not isolated to NAB or QBE or any other issuer or underwriter. Further it is not just travelling with the primary card holder, it is on the exact same itinerary! So if one (eg) goes home earlier or has an additional stop/routing than the other that secondary insurance ‘is not’.