Hello all, I’ve made a claim against my car insurance policy after my house was broken into and my car stolen. The police arrested the offender a couple of days later after they were stopped with tire spikes after a short pursuit and minor collision with a guard rail.

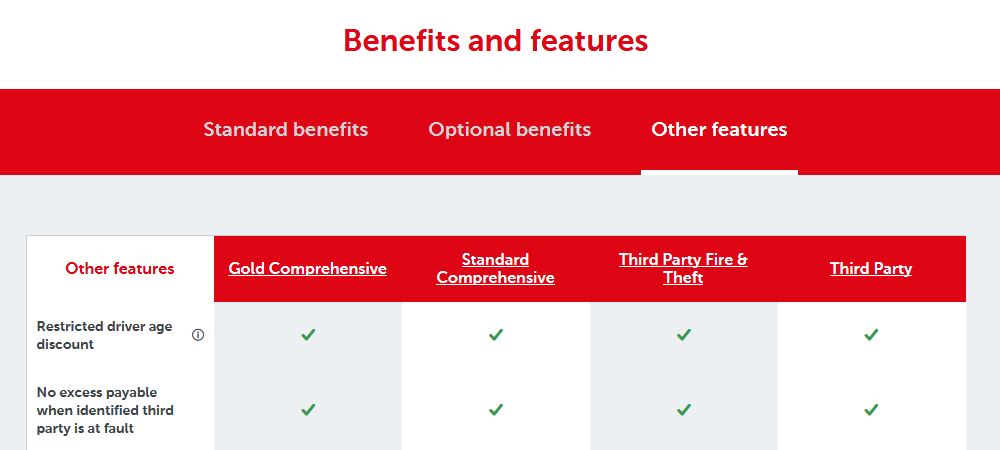

My policy (Gold comprehensive) has a $1000 excess on it for claims with some exemptions as shown in the below image. One being “No excess payable when identified third party is at fault”

They broke into my house, stole and crashed my car, I think this is “at fault” and they were arrested, so they are an “identified third party”

But, the company says I still have to pay the excess because it isn’t a “car on car” claim. And they are unable to get the details of the driver from the police because of “privacy matters” The company’s only recourse is to go through the court system to seek restitution that way and then I might get my excess back, “but it’s highly unlikely and takes a very long time”.

A normal person would assume that no excess is payable if the mentioned conditions are met? Or am I wrong? What should I do next?

In Australia, one is innocent until proven guilty, even if an alleged offender is caught red handed. The insurer won’t know for certain thay the offender is guilty until any court hearings are completed. This could take many months, if not year(s).

The insurer will want to settle the claim with you quickly, instead of waiting for the final outcome of court action. Otherwise, they could wait, not pay the claim and then settle many months/years later once fault is determined/confirmed.

As the theft was part of a crime that the offender was found, you could make a claim against the offender to recoup the excess paid. It might be best to get some legal advice to see what your rights are and also what you can do to try and recover the excess paid.

Unlike two cars in an accident where one/bith parties would always be at fault. Theif etc can be difficult to substantiate eventhough blind Freedy knows who is at fault.

The offender could also say that they had permission to drive the car, were given the stolen items from your house etc which could also muddy the waters in respect of a claim or determining who is responsible.

Also check the product disclosure statement (PDS) for the insurance as thus usually states when an excess is payable. Check the theft area of the policy.

We have had no fault claims for accidents where a 3rd party was identified. Even if they had no insurance, as they could be clearly identified we did not have to pay any excess. I believe the same circumstances would arise in this case regardless of how long it took the insurer to identify the name and address of the responsible party. My first port of call would be to your Insurance firm’s Internal Complaints resolution service and for some tips on how to proceed see https://www.afca.org.au/make-a-complaint/complain/internal-dispute-resolution-tips/. If that process is unsuccessful or you don’t want to tread that path then you can go directly to the Australian Financial Complaints Authority (they advise you to contact and complain to your insurer first but…):

(you can lodge a complaint by email, phone or letter (phone is 1800 931 678, email is info@afca.org.au or address is Australian Financial Complaints Authority

GPO Box 3, MELBOURNE VIC 3001)

Excess waived

You do not have to pay any excess if the car is involved in a no fault accident (see definitions) with another vehicle and the amount of your claim is more than the Basic Excess.

No Fault Accident – an accident where we decide the driver of another vehicle was entirely at fault, and you tell us their full name, residential address and vehicle registration number.

Reading the PDS, it appears that the excess waiver only applies when the vehicle is in a crash with another vehicle, and the other vehicles driver was entirely at fault.

As it appears from your first post that the vehicle was stolen and thief crashed the car into an object rather than another car, the excess waiver would not apply.

It is also important when taking out car insurance that ine reads the PDS, rather than inferring the level of coverage from marketing material such as that in their website. At the end of the day, the PDS provides the details of the cover, exclusions and inclusions. The marketing material will only be a very high level summary of some of the policy cover.

I also expect that your policy certificate will outline that the policy coverage is in accordance with the PDS and/or when you took out the policy you would have had to confirm that you have read and understood the PDS in relation to the policy as this explains the details of the cover, exclusions and inclusions.

While one can lodge a complaint as outlined by @grahroll, Budget Direct will be relying on the wording in the PDS when responding to any complaint. One would need to determine if the effort to lodge a complaint is worth it when the PDS is considered.

It would be interesting to know if anyone has a comprehensive car insurance policy which waivers the excess where a car is stilen or dsmage to the car occurs entirely as a result of another party (parked car hit snd run for example).

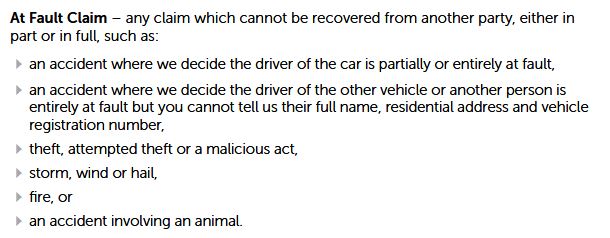

You are correct that they may treat it as an At Fault accident or incident but the At Fault states where the full or part cost cannot be recovered from a Third Party such as in a theft ie “At Fault Claim – any claim which cannot be recovered from another party, either in part or in full”. If the full or part cost can be recovered it could be interpreted that it was a No Fault accident or incident. Also in the “At Fault” for theft it does not require the insured party has to identify the thief, it only requires that full or part costs cannot be recovered. A court action or claim by the insurer for costs in the Criminal case would likely recover full or part costs of the damage and thus satisfy the requirements for “No Fault”.

The “Accident” part is referred to in the Definitions section of the the PDS as “Accident or Incident – an event that is sudden, unforeseen, unexpected and unintended by you” so does not require an actual accident but does include incidents.

The No Fault adds a couple of words which are in this copy of the item “the driver of another vehicle, or another person(my bolding), was entirely at fault” not just “the driver of another vehicle was entirely at fault”. It doesn’t say it has to be the driver of another vehicle it just has to be another person.

Further into the PDS importantly it states:

"Loss or Damage to the Car

If the car is stolen or catches fire, we will pay up to the maximum amount shown on your Insurance Certificate. We will also pay the reasonable cost of recovery, towing and storage of the car if it was unsafe to drive as a result of the damage".

Clearly the PDS states here that they will pay up to the maximum amount shown on the Certificate, not just the amount insured less Excess. Plus they will pay the cost of recovery, towing and storage…this is an added amount.

I think the terms of the Insurance Contract could be unfair if they determine that just because another person created the damage that it was “At Fault” and it would be worth attempting the Internal Dispute resolution and/or an AFCA complaint. ACCC may also be interested in the problem regarding the unfair terms part of their remit.

I agree @omy005aw is almost certainly going to have to wear the excess because the claim is for theft not a multi-vehicular crash. Regardless, if the thief had crashed into another car I suspect the person out of pocket would have been the innocent bystander who would have had to claim to have their own vehicle repaired.

That depends. Does that require payment or just a judgement? How many car thieves with judgements against them pay?

As an example of how insurance can be less than it appears or events ending with police doing the victim, this was in the morning news. Nothing about whether property or any other insurance is in play, just that it is the victim’s problem as the police see it.

I had a look at the policy PDS pre-29 March 2019. The wording of this PDS is different to that for policies taken after 29 March 2019 (with the wording "another person’ included)…in relation to No Fault Accident. One needs to read all definitions and clauses in the PDS to determine the coverage. Wven though the No Fault definition post 29 March 2019 also includes ‘another person’, the Excess Waiver statement is clear that it only applies when a No Fault accident is with another vehicle.

Irrespective of this, the Premium, Excess and Discount Guide for post 29 March 2019 states that “You do not have to pay any excess if the car is involved in a no fault accident with another vehicle.” The same wording is also included in the post 29 March 2019 PDS as well. While it is only a guide, its wording is also consistent with the PDS.

It would be interesting when @omy005aw policy was taken out…but is is unlikely to affect the outcome since the ‘Excess waived’ statement are the same.

The other thought which comes to mind relates to the house insurance cover. As the keys were stolen from a house…and resulted in the theft of the car. This doesn’t resolve @omy005aw issue if he has house and contents insurance with Budget Direct as well as cars are specifically excluded from the H&C insurance.

I have also checked the NRMA policy we have and it is generally similar to that of Budget Direct in relation to handling of vehicle theft (that an excess needs to be paid by the policy holder).

It would also be interesting of the Budget Direct plans to take civil action against the person who stole the vehicle to recover costs claimed by @omy005aw under the policy cover. If they are, @omy005aw should also see if they plan to recover the who of the costs rather than the costs less the excess paid. If the insurer is to try and recover the whole of the costs (which I expect they would do if they were a customer focused insurer rather than leaving the customer out to dry by themselves), the insurer should be requesting the excess be reimbursed at such time. I suspect however even if a civil claim was successful, the likelihood of every seeing the money from the alleged offender would be limited.

Edit: If Budget Direct plans to take civil action to recover their costs from the alleged offender, maybe @omy005aw should be pushing Budget Direct to recover the whole of the damage claim (and not just the damage claim less the excess). @omy005aw should also be requesting reimbursement of the excess when Budget Direct receives payment.

In one instance as you point out is that excesses are payable yet in relation to theft the PDS advises that the maximum amount of coverage may also be paid. A bit contradictory/confusing and not very clear in intent.

This made me look up when our old Daewoo Cielo was stolen in 2008. As the offender was identified and arrested for the offence we did not have to pay an excess on our policy through APIA. All recovery, repairs and hire vehicle charges were met by our insurer. Obviously a different insurer but as I stated before it would be worth making a complaint about having to pay the excess. The terms of the PDS use a lot of “may” which are not definitive but rather are possibles.

I took the maximum amount of coverage as being market/agreed value + incidentals. One would have to pay the excess ($1000) to get potentially the maximum amount back once the claim processed.

I know a few years ago making a claim against our house and contents insurance (while not a car insurance claim) that the claim wouldn’t be processed until the excess had been paid…I asked if it could come off the payout for damaged contents (cash settlement) and was advised at the time no…I had the impression from the insurer at that time (we have a different one now) that as the excess triggers the processing of the claim. Until the excess is paid, the claim is not processed pending excess payment. I expect this is to protect the insurer from work being done before excess being paid and the insurer then having to take action at a later date, especially if the policy holder refuses, to recover the excess from the policy holder. Possibly a cleaner and simpler process for the insurance companies?

The PDS could be clearer in relation to the payment of excess for theft…like our existing NRMA one, but at the end of the day, it is likely they will point to the wording of the Excess waiver…which is quite clear that it only applies when a vehicle crashes into another vehicle which is at fault. It is also interesting they use the word accident…when in reality nothing is an accident (in safety the word accident is avoided as there is always a reason to why something occurred. An accident means that there is no reason or responsibility).

While the following mostly relates to claims investigations it does point to issues with the insurer and why a complaint may hold a lot of benefit for @omy005aw in their case.

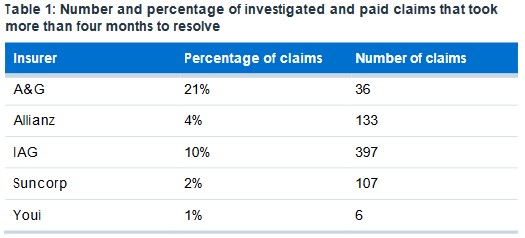

The parent company for Budget Direct, Auto & General Insurance Company, were one of the Insurers ASIC recently reviewed. They found to have delayed claims in “21 per cent of Auto and General’s paid and investigated claims” and “took more than four months to resolve”. Image from the report:

The report also noted:

"Nearly one out of every five consumers in our research reported that their claim had been resolved only after they had threatened to or did complain to an insurer, complain through an external dispute resolution scheme or seek legal advice about their claim.

Our research suggests some consumers thought that their insurer might only have taken action on their claim after a complaint had been made. This can undermine consumer trust in the claims process and can create a risk that consumers who are less willing to confront their insurer about a problem could be treated differently."

The other point is that it can take some time for a complaint outcome to be known. If one choses not to pay the excess, it could be some time before the claim complaint process comes to an outcome. It would be even longer should the outcome of a complaint not be satisfactory with Budget Direct, and one decides to take it to the AFCA.

This can leave an individual in limbo and also mean that a car is waiting repair (unavailable) to the policy holder until such time the complaint outcome is known (which could be in favour of the policy holder or the insurer).

This is also something to consider in relation to deciding how to approach the insurer and also what stand one wants to take.

The statistics for A&G are concerning and possibly why one should think twice of taking insurance with its companies. Saving s few dollars may give much later grief.

I agree but a user does not have to complain to BD first they can submit one immediately to AFCA and advise BD they have done so. This may curtail waiting for longer than what should be reasonable periods. Of course this is not a matter we can decide for the user in this case, whether they pay and then dispute, dispute and await an outcome, or even choose not to dispute and just pay is entirely in their court. The matter does need looking at though regardless of how they proceed.

As another thought in this, they may not even have the money for the excess ready to hand or it may impose a significant financial burden on them to meet that cost at this time. The excess payment situation is a quandary we are not going to solve here as much as we might like to, it needs to be tested at the appropriate places/authorities.

Just also found this on the Budget Direct website…FAQ in relation to excesses…

It states…

My car’s been stolen – do I have to pay an excess?

Yes – but only your Basic Excess.

It would be good if such infornation was clear and upfront in the PDS like it is in our NRMA cover PDS.

Yes, having sufficient funds to pay an excess, especially one which is $1000 would be challenging for most. It would be interesting to see how many insurers have a hardship policy for paying excesses (such as payment plans or similar) when a policy holder has insufficient funds available to pay an up front lump sum. On a positive note, the Budget Direct website indicates that If you can’t pay it as a lump sum due to financial hardship, you can ask us whether you might be entitled to assistance. If you are, we may give you longer to pay the excess or allow you to pay it in instalments, for example.

Bingo. A driver in a rental hit a family member’s car. The driver refused to pay the excess and without the excess being paid the insurance on the rental would not process the claim. The family member’s 3rd party included uninsured motorist but since the rental had insurance that would not pay. The only recourse would have been to sue but the amount in play would not have been worth it. Insurance is not always insurance nor assurance.

Again I agree they have stated a stance they take, but the PDS which is the legal document they rely on to support the stance is lacking in total clarity. They even tell you not to rely on what you read unless you do so in the PDS. Hence a situation they say one thing one place and another way in another. Very confusing, not at all clear, and perhaps mindfully they have done so to create unclear outcomes and perhaps not done wilfully but just because they are so disjointed in their legal advice & preparation of the document. Still worth the complaint in my opinion and it will not hurt to do so.

Hi @omy005aw,

It seems like you have already very good general advice on situation. I will only add that I can also pass on your case to our CHOICE Help service if you are a member, and also please feel free to follow up in this thread and we’ll continue to assist as you progress.

Thanks for the very detailed replies (it’s making my head spin!). I’ve been a Choice member for many many years (please pass on my case CHOICE Help service) and find these community forums most helpful.

After reading the PDS several times through it seems that any thing other than an “accident” involving a identified third part is deemed to be “at fault”.

Although it seems contradictory to their website marketing page. So I guess I have the wear the cost of the excess unless I’m willing to participate in a drawn out saga.

The other thing that grates me, is that I have other cars insured with them and as soon as I started the claim process I was emailed automatically updated policies to reflect my “status” of having made an “at fault” claim. This added several hundred dollars to each policy and also to the policy I’m making a claim on These will add ongoing costs also for years to something I had no control over yet I’m “at fault”.

As I stated above in several posts At Fault firstly states it that a “At Fault” claim is any claim which cannot be recovered from another party, either in part or in full…it then states when these incidents may arise such as you were not at fault but they decide you are, or that you could not provide accurate details of the at fault person.

For an example of your case in two different scenarios

Your car is stolen by persons unknown and they are not locatable…you aren’t at fault but they cannot recover the cost from an unknown party so you are deemed to be at fault and must pay the excess.

Your car is stolen and the thief is apprehended, charged and is dealt with in a Court. The person is then able to be accurately identified and cost recovery can be instituted. You are therefore Not at Fault ie a No Fault incident. No excess should be payable. This is what occurred with us and APIA as I posted in another reply further up.

The problem faced here is that the PDS is somewhat contradictory in what it says eg further into the document it states they “will pay up to the maximum amount shown on your Insurance Certificate” with no mention of excess being necessarily payable if you car is stolen or catches on fire.

The complaint does not need to be an onerous affair. You state your case to AFCA with the relevant details ie person was apprehended and identified by the police, the PDS is confusing and in your case the cost could be partly or wholly recovered as part of the criminal judgement or as an outcome of a civil case. The lack of ability for recovery of part or the whole amount of the cost is the requirement made under the At Fault terms so they must satisfy that no cost recovery is possible. No Fault is where you can identify the other driver or other person responsible who are wholly responsible for the accident (which they define as Accident or Incident in the PDS so not just an Accident).

At the moment to get your car repaired it may be easier to pay the excess now but seek that the decision is overturned by AFCA or by Budget Direct (if you also seek dispute resolution with them) and that your No Fault status is restored. This would lead to your other policies being restored to the previous cost levels as well. However a future staying with such a company may only be to your detriment if anything similar ever happens in the future and I would advise looking around for a better policy with another insurer.

I am not a lawyer so my advice is only based on my reading of the PDS but you could get free legal advice about what you can do at a Free Legal Aid Service or contact a specialist legal advice service such as the Financial Rights Legal Service. They offer many free help services including getting advice over the Telephone ( 1300 663 464 but before you ring check their website for what steps you need to do before phoning) and they have many help services you can access online at https://insurancelaw.org.au/ including email advice.