None of us really know what the salary package arrangement is. It’s confidential.

I’m on the same page as

There are multiple permutations for how the final amount is remunerated.

I’d not speculate.

P.S. there are a number of other strategies not canvassed in the previous posts that may be available. Only the departing Director’s accountants will know, what works best. Many are only effective or accessible to individuals with high personal wealth and income. Legal tax minimisation or rort? Ask any of the overpaid shock jocks, You might get on air, and you might not like the response.

Excepting for top tax lawyers and accountants it is so complex and convoluted the best most of us can do is speculate.

‘My’ CEO who during his tenure in Australia (AU, US, and other citizenships!) had a base in the strong 6 figure range, bonuses, and 27% ‘extra’ super on top of the 9% super guarantee.

As a US citizen he enjoyed his relationship with the US IRS even more than myself so we often talked taxes. Much/all of his tax on the 27% extra super was covered by the company. He still had to pay tax at his marginal rate but only on what the company paid re his taxes, not on the full amount, or such was my understanding.

That was a few years ago before the last round of tinkering with super and taxes, so it might be different today, and I might have misunderstood. It seemed fuzzy then and fuzzier now, but bottom line is he came out quite well.

Companies to get the people they want at the top often pay extra “tax” money to cover the tax difference to what a person may otherwise pay thus leaving them cost neutral tax wise.

As easy a target as a bank is in Australia, a loan is not a gift. The bank has a reasonable expectation that the loan will be repaid in accordance with the loan conditions. Nowhere are we told what those loan conditions are, but an overdraft is a relatively unpleasant way of borrowing money. Nowhere are we told what the borrower’s overall financial position is.

If your money is with one of these superannuation funds you might want to consider swapping.

That quote is not financial advice and neither is this post … but “swapping” after one bad year of performance may just be selling out at the bottom. Do that a few times, chasing last year’s returns, and you will be your super balance’s worst enemy. It would be even worse if you were forced to do that because the fund is shut down by APRA, as threatened.

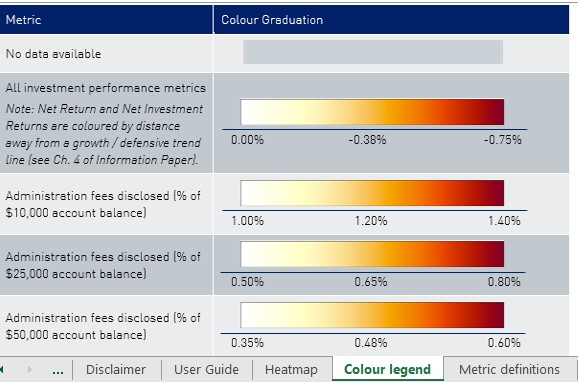

Strangely though that article seems to be completely devoid of any information about performance of any super funds.

The reference in the article to “glowing red” is because the worst end of the colour gradient used is quite a red colour.

The Heatmap in some cases does not provide a value but a colour coding of results for a 5 year period and some results are not very good at all with some showing -0.75% growth over 5 years.

As to being devoid of any information about Super Funds it was mostly general but some actual references are made to Funds and Fund managers eg “For fees on a $50,000 balance. Pritcher Partners’ Pritcher Retirement Plan was the worst identified in the group, charging 1.93% in fees.”

True. However performance-after-fees is all that matters. If my fund achieved performance-before-fees of 15% (annualised) and charged high fees of 5% (annually), I am happy because that probably means that my fund beat every other fund on the market.

One thing that I would want APRA not to impose is that fees are based on relative performance. I have seen this frequently outside the super system. If APRA is to intervene on fees, it needs to be based on absolute performance. So if we have another GFC-like period and annual return before fees ranges from the horrible -30% to the bad -10%, I don’t want to see the “bad” rewarded with higher fees.

Many of the corporate names in the article re under-performing default funds seem somehow familiar. Now where did we hear about them recently for other ‘top rorts’?

NRMA was a surprise in more ways than one. I wonder why anyone would go to any non-financial organisation/institution for a financial product? Don’t they at least throw in free road care with every Super plan?

They used to be a financial organisation and I think they still manage a large portfolio - but would have to rustle up an Annual Report to verify that.

Westpac’s shareholders have delivered a second strike to the bank at its annual general meeting, forcing a board spill motion, but the directors survived with that spill rejected by more than 90 per cent of votes cast.

Increasingly, companies who are on “one strike” are using this tactic. By law the remuneration resolution for the second strike is on the agenda (as it must be every year regardless). So they add the spill motion up front as a conditional resolution, conditional on getting the second strike.

Because the threshold for a strike is only 25% vote but the threshold for a spill motion is 50%, it would be highly unusual for a spill motion to succeed.

As I have said before they will wring their hands, they will tell us Sorry, they will promise to improve but reality says they won’t change much if anything and will still continue to be Boards etc with almost no impact to them.

I think and it’s only my opinion here that they are Sorry because they got caught and now need to show public contrition so privately they can continue to personally prosper.

I once thought the pervasive nature of our self serving boards and politicians was a result of our small population developing a small number of individuals with skills to deal with ‘those things’.

Reality is there are many, many countries with far smaller populations and far more responsible boards (and politicians).

I have also come to understand many of the most culpable political apparatchiks that consult with political parties globally, who take the ‘very lowest roads’ are often Australians

One of many… a “master of the dark political arts”, “the Wizard of Oz”, and “the Australian Karl Rove”

and

It appears to be historic and now culturally pervasive for the top end since they have been successful doing it, and have a long history of doing what they do with impunity.

edit: We are led by these self serving sorts from the top down. Let the rorts flow, no problems and we refuse to hear of any.

In some sense they should never have been allowed! Only unaware people paid the commission. You could always contact the fund manager and tell them that you no longer had a relationship with the adviser and the fund manager would clear the adviser from your holding and stop paying the commission. Simples.

However the language used in that article is a bit misleading as it is not a fair representation of the situation to say “despite there being no ongoing service” because the point of trailing commission as an alternative, in whole or in part, to up front fee was to avoid the sticker shock of up front fees and to avoid the impact of up front fees on the investment.

Whether the advice is good advice or bad advice is a whole other can of worms, and is independent of the fees.

I learned at some cost there are many aspects of the super industry that are ‘Simples’ if one knows about them. One of the problems with that is that the ‘Simples’ are often well hidden and never talked about in ‘polite company’ so long as the funds were able to avoid it. I accidentally ‘had a conversation with some documents’ I stumbled on so recovered without much financial impact; if I had not and did not have an adviser (which I did and do not) by now it would have been in the many $10,000s rather than a small number of $1,000s due to the differences between ‘retail’ and ‘wholesale’ fund fees.

Anyone can get a wholesale fund with a fairly reasonable entry amount, and one can move from a retail to a wholesale once the threshold is reached, on application; they are not just for investment houses, something many ‘new Australians’ might not understand since in many countries the wholesale versions are only open to financial institutions or have substantial entry minimums ($100,000+).

As for advisers getting trailing commissions forever, not so many years ago one had to have an adviser literally sign off on some super issues (salary sacrifice for one) so it would not be surprising if the punters exposed to that era thought one needed an adviser of record so just went with it not realising the implications.