Independent financial services providers are in the market of offering loans to assist parents pay fees. I’ve noticed more often adverts popping up in the side bars or imbedded in search results/online content. The advertising targets may emphasis giving one’s children a better start in life by using a loan to pay for schooling including school fees for primary or secondary schooling.

The loans are effectively personal loans, secured or unsecured with higher interest rates and fees.

Looking to several of the brands the easy to apply online, no security same day approval tactic stands out. There are alternatives available through the major banks. For post secondary education there is Govt HECS and HELP funding. Note the personal loans on offer also include promotion of their products to support post secondary education.

Has Choice taken a look at some of these products?

Are there community concerns some of the loan products are debt traps with excessive fees and high interest rates relative to need?

As a broader community are these additional loan facilities really necessary, and if so is there a better way?

It’s up to others to consider if something is seriously wrong with how our primary and secondary education is provided for. Especially if families now need to take out loans to pay for the education of the next generation of Australians.

There is also Fee-HELP, SA-HELP and OZ-HELP, but again there are eligibility criteria for these as well and not all enrolled students would qualify (noting that about 27% of students enrolled in tertiary institutions are overseas students and are eligible for government support). The loans are possibly targeted to those who don’t meet the eligibility criteria for government assistance, or incur other costs which aren’t covered through government support.

Like any financial product, it is important to obtain independent advice on the suitability of the financial product one is interested in. Each product will have its own risks which need to be understood as these risk may or may not be acceptable.

@mark_m was pointing to the primary and secondary education fees that are now the targets of loans to assist families pay the cost of educating their children in the public school system (free education perhaps not) and perhaps the private schools system:

It is distasteful to me to see how costly it has become for families to pay for “free education” for their children.

I would think no more dodgy than the usual unsecured personal loans available for various purposes. Short term compared to home loans, the usual higher interest rates, establishment fees, onging processing fees.

If aimed at parents, then they would have to consider the benefits. If aimed at students, then they would have to consider the course of study, since only those considered to have Government support will be eligible for HECS-HELP.

But with a personal loan, nobody is going to lend a student money unless they have an income to service the monthly repayments. So presumably part-time students who are working.

Presumably Dr Watson would have read the opening paragraph.

The questions relate to those products which are being directed at the parents of school age children. Agree, it’s a different context with loans for mature age students.

People are most at risk if they are firstly sold enrolment in a course that has little or no prospects of giving them a meaningful qualification or job prospects and then advised to borrow to pay the fees.

Unfortunately for both transactions there is likely to be little, if any, protection.

How much are they paying? Is it compulsory? and What is it for?

We have had experience in two states, Qld and Tas where government primary school fees (which are for things like student room supplies, excursions, and in Tassie - student stationery) are compulsory for those who can afford them.

Families, which can’t afford them and show evidence, the fees can be waived. Student families which can pay the fees possibly pay a bit more to subsidise those families which can’t. The local Rotary where we currently live also provides funding for financially disadvantaged families as well so they have the same opportunity as others.

Government/public education has never been free for everything. Parents have always paid for stationary, excursions, uniforms, sports uniforms/equipment and special activities (such as a performer visiting the school). The main change has been many parents now pay a one upfront fee for these to the school/P&C. In the past, parents organised their own childs stationery and paid for other things at the time they occurred. Many parents struggle with paying a larger upfront fee you the year, rather than being dripped fed throughout the year.

I have issues with upfront fees from a waste perspective. When I was a youngster, a lot of the stationary was used year after year until fully used. Now with upfront fees, new of everything is bought each year. Last years are either thrown out or sent home to stockpile.

These would be non-government sector or special schools. If a parent choses to send their child(ren) to non-government schools or special schools, they need to finance these fees. This would be done by a range of means including in some cases taking out loans. Marketing education specific loans provides an alternative to consider than other loan options. Some other options may have higher long term costs.

When I went to primary school in Qld all items needed for my education were free including stationery, text books, pencils, tissues. School uniforms were also optional. In about 1972 in a restructuring of costs, more cost was placed on parents and some funding was supplied to supplement the added costs. This funding continues.

My mother has confirmed that education in Qld public schools was free until the changes made. In her years, primary was free and up to junior was free. To continue past junior a student either had to pass scholarship or enter into a trade. My mother was not allowed to take up her scholarship by her parents and instead finished her senior under what was a bonded school teacher program of the Qld Govt Education Department.

My first degree was free as well, only later was HECS introduced.

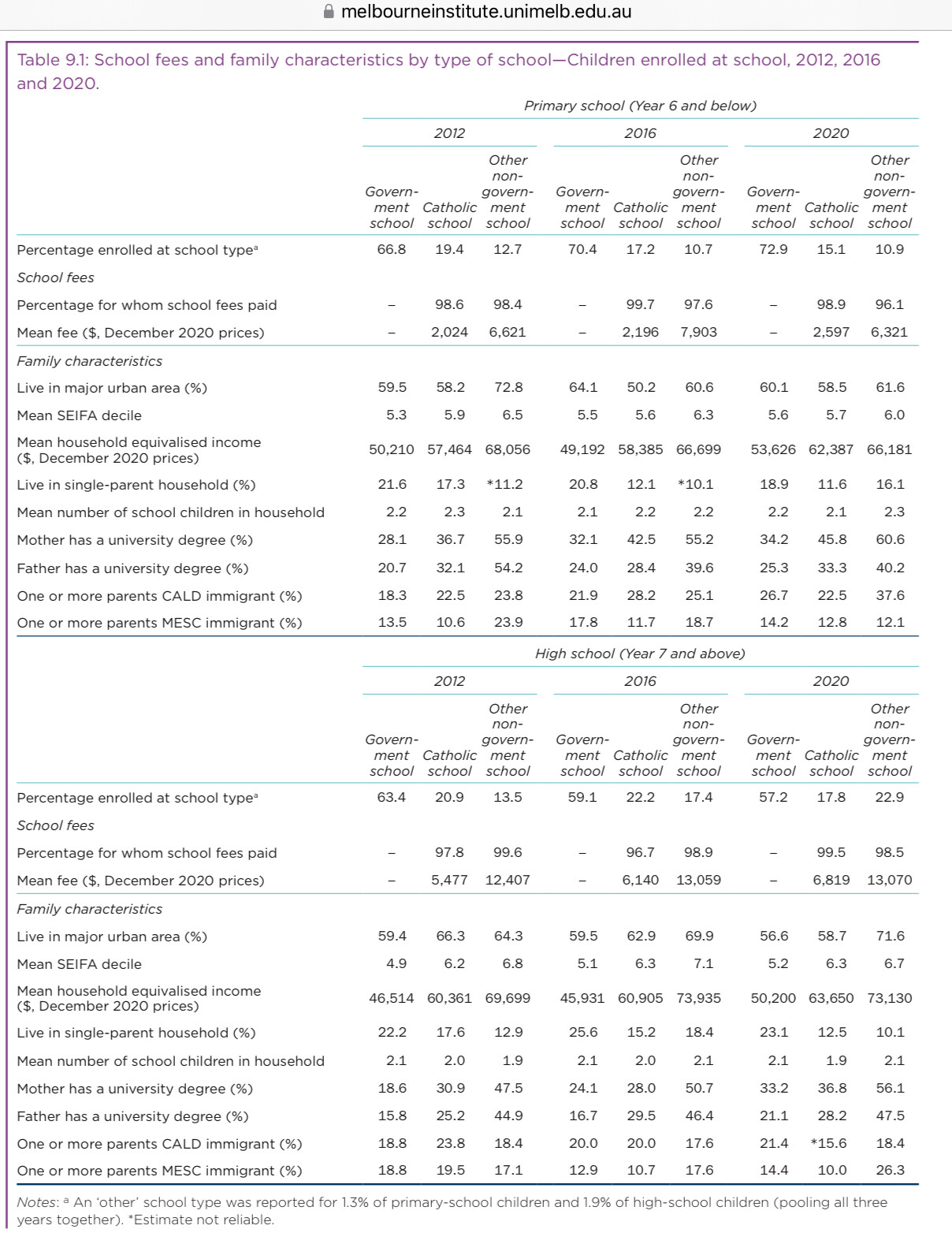

“School fees” for primary and secondary education are principally a payment for tuition/enrolment. Government schools do not charge a periodic fee to attend schooling. Access to education is provided free of charge. Hence not included in the following table. In contrast as shown Catholic and other non-government schools charge tuition/attendance fees.

For primary 26% (approx 1 in 4) students and for secondary 40% (approx 4 in 10) students pay school fees. Typically there are slight differences with more recent selected data, refer to the following table. Although typically not presented in the same detail/context. Follow the link if the table does not display with sufficient resolution - section from page 128.

Yes, there are other added costs including uniforms, etc at every school. The level of additional support available in government schools varies nationally and by school. Typically the national statistics do not include these needs (necessary or voluntary) as “the school fees”. Although private schools vary as to what may be included or expected.