I don’t think so. I can see that the issue is close to your heart but in the previous you have not convinced me that the system is either workable or equitable. I don’t see that anything has changed since then.

What you are proposing comes down to giving some people the ability to not compete in the competitive property market. You have not explained how:

there is no subsidy involved and that as a subsidy either somebody has to pay the difference or, faced with being forced into it without recompense lenders will just refuse to offer such loans

you would avoid the situation where artificial rules that advantage some in the market places encourage rent seeking

you would avoid inflating the market by increasing demand as all the other home-owner subsidy schemes have done.

In a number of ways the scheme risks disadvantaging the people that it aims to help.

As reducing favourable tax conditions that favour investors seems politically impossible the only way to take the pressure off housing prices is to increase supply. This should not include expanding land available on flood plains, acute bushfire areas or risky seaboards.

I just don’t understand what the connection is between ability to choose between a fixed rate mortage and a variable rate one, and negative equity.

How much you can borrow is set by how much a lender will lend based on their valuation for security.

If the market value of a property has dropped, then a lender will lend less, whether it is a first lend or a refinance.

What variable rate or fixed rate of interest has to do with that is a mystery to me.

I suspect that if there are negative equity risks to borrowers they impact mostly property investors. That’s our observation as investors borrow against equity, and carry high gearing rations. IE increase debt to the max assuming never ending capital gain and increasing incomes from the investments. Investors gain financial support through tax deductibility and allowed business expenses that are not available to home owners. Investors can use pre tax income from the investments to meet expenses and claim back gst where applicable.

Owner occupiers meet all loan repayments, maintenance, refurbishment, and expenses from after tax earnings. Any offset for owner occupiers through exemption from capital gains tax is often far into the future.

For the banks the owner occupiers income streams are less volatile and readily assessed by the lender. When it’s the roof over your head most will do their best to keep it. For banks these are low risk customers. I’m aware of banks requesting additional payments from investors where the LVR in a falling market exposes the bank to risk if the loan is in default. I’m not aware of the same with everyday owner occupier loans.

Property investors would be going after interest only lending. To maximize tax deductions.

Only the interest is tax deductable. Any component as a part of regular monthly payment that goes toward paying off amount owed is not tax deductable.

Not the same as fixed interest loans. Different thing.

As is 100% LVL borrowing. Different thing.

Possibly one size does not fit all?

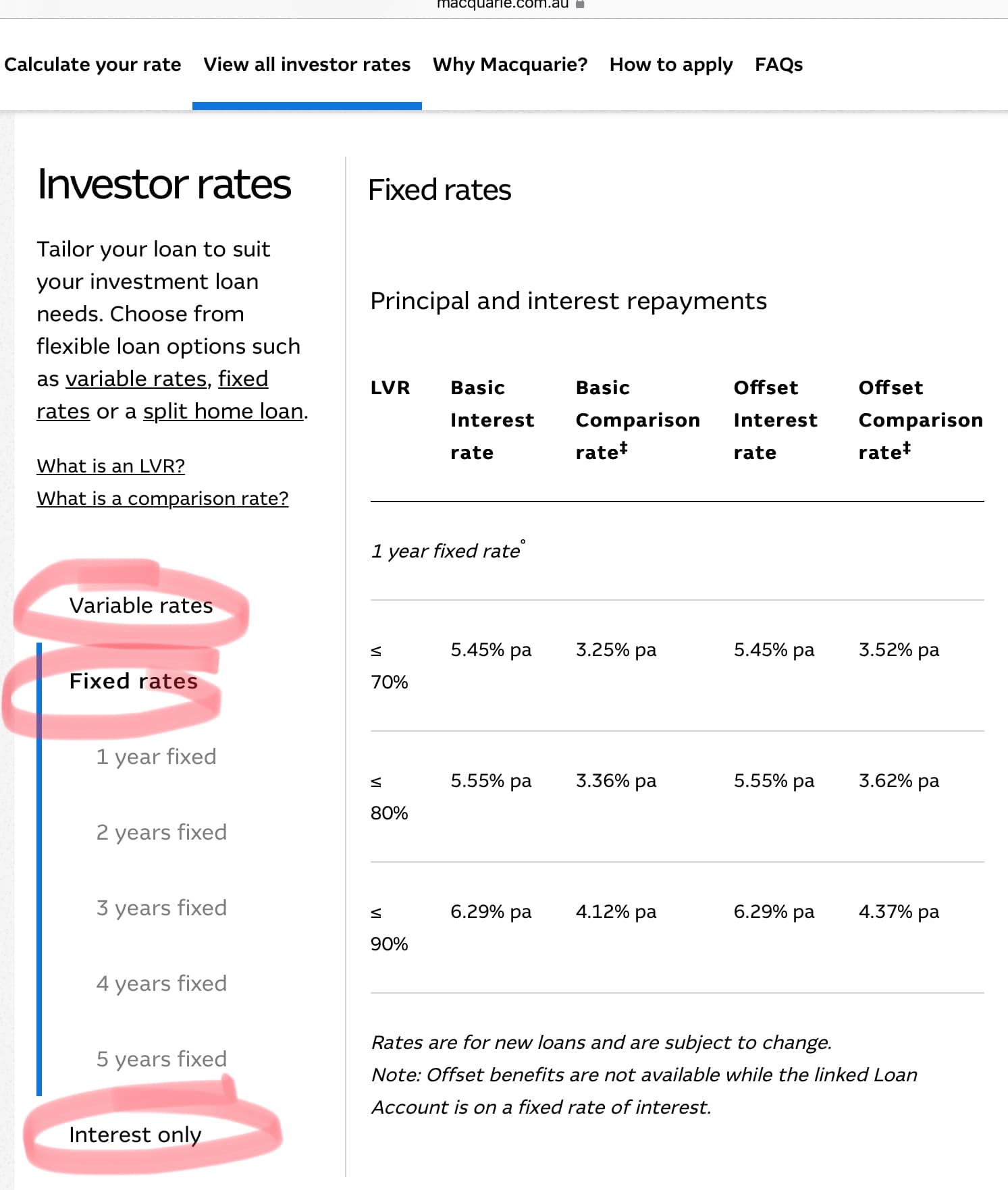

One well known bank offers investment loans with Variable rates and Fixed rates (interest + principal) as well as Interest only.

I’ve linked the web resource. It should be evident if one chooses to look further that there are significant differences in the costs between the available options. There is clearly a demand for the options, otherwise they would not be offered.

Is there wisdom in choosing one over the others? Best to discuss with an accountant or properly qualified financial advisor. Personal circumstances and ability to absorb risk may differ. Any property investor concerned about the risks of a downturn in the market place hopefully has assessed the risks carefully and clarified their lenders ongoing equity requirements before signing up.

It isn’t, and the closest example of monetary policy to Australia is possibly New Zealand.

In relation to negative equity, like New Zealand, it is unlikely to be a significant issue. It is worth watching the video interview of NZ ANZ chief economist Sharon Zollner, who discusses changes in house prices in NZ due to recent interest rate rises and the situation of negative equity.

For NZ she states:

“Very few people are sitting in a house that’s worth less than they paid for it, even fewer in a house that’s worth less than the debt that they owe on it,”

It is likely that Australia will be in a similar situation as it’s RBA monetary policy is about 6 months behind that of NZ and what is happening over the ‘ditch’ is likely to also be seen here.

This topic has been chased around for quite a while, off into the bushes and back again and still there is little clarity. There are several key questions that have no answer. It isn’t clear to me that in this country it is a real problem.

We have no data on the frequency of housing loans falling into negative equity in Australia. We need to know why does it happen, how often and to whom.

For those who are in NE we have no data on the outcome. What are the demonstrable consequences of this? It sounds like a really bad thing but I see no evidence that it is. How many people are made homeless or have all their dreams shattered? Show me.

John tells us:

Fixed-rate mortgages could help to reduce the negative impacts associated with negative equity. This is because a fixed-rate mortgage loan helps to lock negative equity homeowners into an agreement made at the time of entering a mortgage contract. However, a lender is unlikely to approve a new mortgage for individuals in negative equity since their properties would not provide sufficient collateral.

What are these negative impacts?

You say that locking the homeowner into an agreement made at the time of the mortgage will help. You don’t say how this works or provide any evidence that it would. If the interest rate of a fixed rate loan is higher than the current variable I don’t see how will that help.

Household equity is a bookkeeping entry. If the homeowner keeps paying their mortgage+++ they have a house to live in and whether their equity is plus or minus makes no difference to their life. The time it matters is if they want to sell. Being locked into a fixed rate mortgage will not alter the problem of trying to sell at a loss instead of a profit.

I don’t see how it will assist but it looks to me that you want to negate the situation described in the last sentence. Instead of the lender having the right to refuse a fixed mortgage you want to compel them to accept it. As you say they are likely to refuse it for lack of collateral. Loans with poor collateral are higher risk to the lender. Higher risk loans attract higher interest rates. You say there is no subsidy involved so either the lender has to absorb the difference or the borrower has to pay a higher rate, which?

+++ The capacity to repay depends on the household income and the interest rate, neither of those are altered by being in NE. Interest rate shock is a separate issue to a property holding or losing value.

Those borrowers who chose fixed interest loans (short term, typically max 5 years), should have been fully aware that they would need to refinance at the end of the term.

Or sell before the end of the short term loan.

They took a gamble that if interest rates rose, the monthly payment would not increase.

And also that the valuation on the property would at least be the same and preferably higher so the refinance would not involve an injection of more capital, but may be at a higher interest rate.

Some of those gamblers may well find out they get the double whammy in the next few years of having to pay back more principal at the end of the term than a lender will lend to refinance, and the monthly payments will be considerably higher.