A lot of developments have occurred since the last post on this subject. We now have substantial negative equity in housing in Australia (e.g. Western Australia), a slowing global economy and Australia approaching zero in the RBA cash rate. It is time that we had a look at the situation overseas. Here is a review of negative equity in housing in the European Union: https://www.freelance-work-guide.com/housing-negative-equity-in-the-european-union.html. Any comments?

Yes the third party view is a potential warning for Australian investors with European property investment portfolios.

I prefer more authoritative sources with a proper understanding of Australian economic circumstances.

The real risk is as I read it nothing to do with negative equity. The real economic risks are in higher unemployment and inflationary pressures reducing real incomes.

A secondary consideration is that a large percentage of investments in the high capital growth properties associated with the mining affected regions of WA and Qld were speculative. Ignorance is no excuse. They also represent just a tiny fraction of Australia’s total property markets. And yes, there are some very unfortunate mining families who may be home owners and have been caught in the mining boom and bust bubble. That’s the way mining goes. It has less to do with events in EU and more to how the mining industry invests in the local economy.

Very good point and anyone who would have done some basic homework when making an property investment decision in such regions, would have been aware of the volatility of house prices (cyclical just like the resources sector).

There has been recent reports that the market in these areas may also be turning…

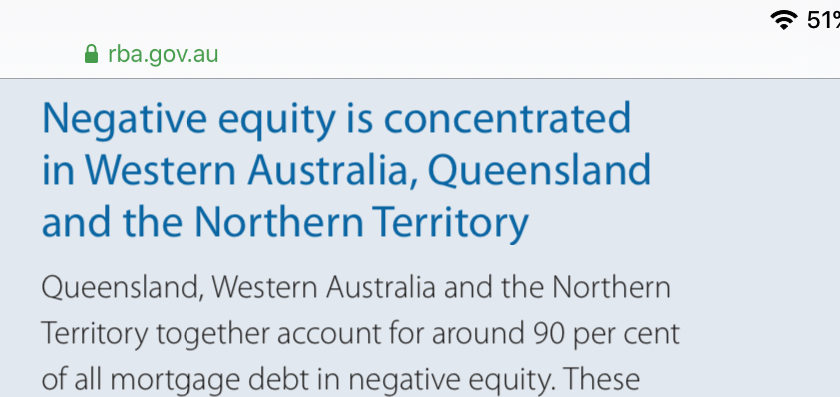

Looking at why and where we have some negative equity is useful.

WA has been going through a boom/bust pathway for years. This has distorted many things financially including State tax receipts, GST shares and the State budget, as well as the housing market. This cycle has been largely due to fluctuations in the mining industry. The high proportion of investor loans in WA is no coincidence, when a boom is on the speculators will come running pumping money into the market and hoping to be one of those who cash out before the bust, not one left holding the bag having purchased unwisely or hung on too long. I suppose some amateur investors would have come from Camelot where booms go on forever.

Sadly the owner occupiers are caught up in the boom and have to pay the higher prices too. And sadly some of them get caught out when the bust comes as well. Mining booms also corrupt the rental markets in growth mining towns. You can get a sleepy little place explode when a new mine opens nearby. As miners earning big bucks move in demanding housing rents double and triple and the locals, who are often on more typical rural low wages, cannot afford to stay. This is another pressure as investors pushing up prices on rental properties stokes the market more. Sure booms produce winners - but they also produce losers.

We also see conflict over changes to lending rules. On the one hand we have those wanting to borrow very large amounts that they don’t see as excessive because they too come from Camelot where interest rates are always low, wages always rise and it only rains after sunset. This desire sets them up for a fall individually but also contributes to the boom as they are prepared to borrow more and spend more which only pushes the market up further.

I have heard young marrieds say “Why can’t we borrow as much as Fred did three years ago, it’s so unfair, and why do we have to have such a high deposit?”. They cannot see that they may have been saved from committing to a huge burden and be better off saving a bit longer and buying a smaller house. But I want instant gratification and I want it NOW! And five bedrooms, three bathrooms and a study and a sewing room and a big sundeck and a kitchen just like on The Block.

On the other hand the same people don’t want to pay huge amounts of interest servicing big debts and don’t want to end up stuck because they cannot afford to sell. However in some unstable markets some have got stuck. This is unfortunate for those who need to move because of other commitments but perhaps they could have factored that in before they bought. As for those who are staying, if they keep up the payments and increase their equity, in time markets will rise and they will be in the black again. In the meantime they have a roof over their head and are paying historically low interest.

My point here is borrowers need to plan ahead and take responsibility for their decisions, this includes being careful in unpredictable situations. If you bail out those who overcommitted who else will have their hand out? Where does it stop?

Your scheme of guaranteed fixed interest rates would only corrupt the market further by giving the foolhardy and investors another reason to overcommit. The result would be to add to instability and exacerbate the problem you are trying to solve.

Should there be a bailout or ‘protection’? That would be terrible policy as many have already written.

One of the troubles of negative equity is that if a buyer walks away and a bank repossesses a property, the bank is not in the property business. Simplistically they will dump the property on the market, apply their income toward the balance, possibly sue the defaulting party for the balance or if there was mortgage insurance they will collect it and move on.

This is a disincentive for the banks to maximise the sale price of repossessed properties. They want ‘out’ as soon as they can. Any loss they incur is a tax loss so they are whole or close enough regardless of sale price. If there are enough repossessions in an area the number of dumped properties will further depress local prices possibly creating a downward spiral.

If tax laws were changed so that if a property was repossessed there was no tax loss applicable regardless, it might encourage a bank to work with a defaulting mortgagee longer, or to renegotiate the terms to keep payments at ‘interest+any amount’ flowing, and might make it less likely they would dump a property on the market; it is conceivable they could create (or contract for) property management subsidiaries to rent them out until they could be sold for full value or better. That might be short or even very long term, so some tinkering to make a long term ‘out’ has to be considered.

There are legitimate ways to manage a property market through tax laws that are not protection and not bailouts, where all parties have a chance to come out better.

Hi BBG, Thanks for the comment. Yes, I agree that the bank’s are not in the property business, but they are in the risk management business. The pages of history have shown that we need to manage the risks in housing real estate better from a client’s perspective. I do not think that it is fair and reasonable that homeowners should be exposed to the risks associated with borrowing for their homes. I think that banks in Australia can do it better. Here is an extract from a research article:

Quote

How EU Banks And Homeowners Can Protect Themselves Against Negative Equity

Jyske Bank has developed a unique way to protect themselves from the hit of negative equity, but how do other banks and homeowners weather this reality across the European Union? For the most part, banks account for and cope with negative equity through the use of something called lender’s mortgage insurance (LMI).

As it sounds, this type of insurance provides a guarantee for a lender in the instance where they don’t receive full repayments on loans. As can be seen from financial crashes like those in Ireland, though, this is not a fool-proof plan for wide-spread defaults and issues. It also offers no protection for borrowers.

That’s where consumer’s insurance comes into play. Also known as mortgage protection insurance, accounting for policies like these in monthly payments could see homeowners avoiding negative equity altogether. These types of policies are widely available to all homeowners across the EU.

Some lenders even offer such insurance or require it before approval. As well as protecting against fluctuating house prices and interest rates, mortgage protection guarantees lenders can continue meeting payment in times of sickness or job loss. In short; this is the most rounded and vital way for homeowners to avoid EU negative equity at all stages of their life.

The issue is that mortgage protection insurance that protects the consumer should be a part of the structure of all home loans. The reason for this is that when negative equity occurs the shortfall has to be paid back if the market does not readjust over time. The extent of the readjustment over time can be considerable, possibly extending beyond a lifetime. Here is an example from Canada of what the IMF thinks of their real estate market: https://betterdwelling.com/the-imf-crunched-numbers-on-canadian-real-estate-heres-how-overpriced-it-is/>

TheBBG, do you think consumer protection should be compulsory in all home loans and what and what other policy protections should the Australian Banking Code of Practice have in place related to this issue that the Australian Consumers Association should be campaigning for?

I do not think it is the banks responsibility to protect people from their own ignorance of realities that what goes up might come down. If they can fund a mortgage today why is it the lenders responsibility that they might lose their jobs 10 years from now, or 6 months from now, or a real estate bubble pops?

When that happens the tax laws essentially shield the lender from much financial harm. I do think the tax laws encourage a regime of foreclosure that is unnecessary as well as bad public policy.

Thanks TheBBG for that comment. All of the abovementioned are insurable risks to a certain level, but not the taxation law which I am not across. Reform is never easy because people are resistant to change. However, I think that the pages of history which are currently being written will be looked back on in ten years time and wondered at as to what the resistance to reform was all about.

I will be very surprised if many reforms to the financial system are not initiated by Christine Lagarde, the former Managing Director of the IMF, but now the President of the EU’s Central Bank. There is a very good video of her views in this New Economy and The Future of Work Forum in 2017 : https://www.imf.org/external/POS_Meetings/SeminarDetails.aspx?SeminarId=263>

Now that there is Covid 19 vaccines available and the world is starting to look to the economic recovery from the lockdowns should the Choice Community and Choice itself be looking to create working relationships with other consumer protection associations globally? I think that this is an important question in relation to common critical issues that the world faces for consumer protection as we start the economic recovery.

I believe that it is the role of Choice and the moderators of the Choice Community to open the communication channels for the interaction with the goal of better protection of consumers globally.

It is tempting to dismiss this as being of no consequence to Australia, but this is a mistake when you consider the mission statement of the Money and Pension Service in the United Kingdom:

Our mission

Our mission is to ensure everyone in the UK can easily access the information they need to make the right financial decisions for them throughout their lives, making the most of their money and pensions.

“MaPS is the largest single funder of free debt advice in England and also works alongside partners across the UK to make debt advice easier and quicker to access, and to improve standards and quality across the sector. We lead innovation by managing an extensive research and evaluation programme to help underpin decision-making related to financial wellbeing for consumers.”

Here is a question to the moderators of the Community Group and Choice Executives: Where can we find an equivalent article in the Choice Community that addresses this issue and the rights of home loan borrowers to fixed-rate housing loans when in negative equity and related issues?

Do other members of the Choice Community think that this issue identified by Which is important to Australian and global consumers?

Choice has an ongoing working relationship with Which? including sending staff to Which? (I am not aware if any Which? staff have spent time with Choice.) There is also a close relationship with Consumer (NZ). The organisations also have shared some tests, of course with some localised adjustments.

I cannot provide any insight into the decision making of what gets cross published.

Hi @JohnCosstick, I can confirm what @PhilT has mentioned - CHOICE is a member of Consumers International, the peak body for consumer organisations across the world. We also work in various ways with our colleagues at Which? along with many others.

Financial and housing markets including concerns around negative equity are not necessarily the same across the countries, so it’s important to take care of the differences. An older article from CHOICE can be found here, I’ll also pass on your comments to the finance team.

Thank you for the reply. I am aware that there are differences in the financial and housing markets in different countries. However, I believe that the writer of the Which article (https://www.which.co.uk/money/mortgages-and-property/mortgages/negative-equity-ap5p58v9gbs8) was issuing a warning about the impact of negative equity. A PHD researcher looked at the same topic here: https://www.negativeequitytoday.com/rights-to-a-fixed-rate-home-mortgage/. The question that arises after reading the article is: What are the Australian home loan borrowers’ rights to fixed-rate housing loans when they are in negative equity? This is particularly relevant to many countries, but especially Australia with its high level of consumer debt with record low-interest rates. Brendan, I look forward to reading a Choice article written by your finance team in response to the Which article. Of particular interest would be a case study of, say, a variable interest rate home loan mortgage for $500,000 (in negative equity) switching to a fixed rate and the savings of an average of 2% interest rate on repayments for the term of the loan for 30 years. Your Finance Team would be smart to do the calculations! This is the reason that Stefanie Garber wrote the article for Switch, in my opinion. Do you agree?

There are many consumer risks in the Australian housing market.

There is the current Choice and broad consumer awareness campaign against changes to responsible lending laws.

These actions have a much greater potential to protect consumers today, than one off suggestions that are more speculative of the future. Others may disagree.

These may bring about the changes you want if there is enough support in the Australian Community for them. If there isn’t enough support regardless of whatever CHOICE recommends, researches, and or reviews these things won’t happen. Getting a house is important to many people and they may resist the push for change when they see their options dwindle. I’d support a petition calling for stronger lending laws including those that reduce the risks of anyone getting into a situation that causes Negative Equity in the first place and I’m sure many others here would as well.

The strong safe lending law offers I think a better protection when loans/debt is assessed by Financial Institutions. I think many of the problems people face are because of weak lending laws that have allowed Financial Institutions to fail to properly assess the lending risk. This has already been reviewed by CHOICE and a number of other concerned parties. Negative equity would largely disappear if prudent lending practices were enforced.

If you haven’t done so already I ask you to please seriously consider supporting CHOICE’s, and their coalition of other groups, push to stop the weakening of the safe lending laws as linked to by @mark_m in the post just above. There is an open letter that can be signed if you haven’t done so already. If you have already done so please encourage as many others as you can to do so as well. With enough numbers this may be enough to halt any further contemplation to weaken the law. If there is enough support this may also generate a call for further strengthening of the law to further safeguard the borrowers.

Middle income citizens in the United States took a multi trillion dollar wealth destruction hit because of negative equity in housing partly due to Adjustable Rate Mortgages and the failure of consumer associations to protect them. To say people were angry is an understatement! The Consumer Financial Protection Bureau was the result, see here: https://en.wikipedia.org/wiki/Consumer_Financial_Protection_Bureau.

I suggest that is misinformation without the full story. Variable rate mortgages are comparatively rare in the US and fixed rates are the norm. One aspect is that accounting/tax encourages US banks to foreclose rather than to work with their customer for very long. When many foreclosures happen they are dumped onto the property market and drive prices down, hence negative equity. People then purposefully defaulted on their mortgages reinforcing the downward cycle.

You inclusion of ‘partly’ is thus appropriate, but ignored the major forces that drove it. Been there, was part of it circa mid 1980’s. I bought a property in 1987 where the owners paid $20,000 at closing (settlement) to finalise their mortgage and keep their credit rating intact. Few were so conscientious.

Thanks for the reply here is my research on the topic:

“There were many causes of the crisis, with commentators assigning different levels of blame to financial institutions, regulators, credit agencies, government housing policies, and consumers, among others.[5] Two proximate causes were the rise in subprime lending and the increase in housing speculation. The percentage of lower-quality subprime mortgages originated during a given year rose from the historical 8% or lower range to approximately 20% from 2004 to 2006, with much higher ratios in some parts of the U.S.[6][7] A high percentage of these subprime mortgages, over 90% in 2006 for example, had an interest rate that increased over time.[4]”

Is it time for Choice to revisit the rights of home loan borrowers in negative equity to have a fixed-rate housing loan for future loans? It is reasonably foreseeable that many variable-rate home loan borrowers and short-term fixed-rate housing loans coming to the end of the term of their fixed-rate loan will probably be in negative equity. This situation is not unique to Australia. The question for Choice’s researchers is how can consumers be better protected from an interest rate risk management perspective? It would appear to be that this is a discussion that Australian consumers need to have.

What do you think, an issue for Choice’s researchers and advocacy to protect consumers or not?

John Cosstick

Disclosures:

I am a freelance journalist. I own and manage these websites and associated social media channels:

I own this Australia Innovation Patent Number 2020102287 related to better interest rate risk management and negative equity recovery in housing loans. It is a public document accessible at IP Australia here: IP Australia: AusPat Disclaimer