Is worse yet to come?

Both a forecast and hindsight in the one article.

After almost two years of assuring Australians that interest rates were unlikely to rise above zero until 2024, the RBA boss — having by then delivered seven consecutive rate hikes — had little option but to confront the growing tide of public anger head on.

“I’m sorry that people listened to what we’ve said and acted upon that and now find themselves in a position they don’t want to be in,” he told a Senate Estimates Committee.

It’s not only that interest rates are going up. When interest rates were going down which lenders forewarned of increases ahead?

It suited the lenders, the property market, some would say also the governments of the day at all levels, to encourage increasing debt. It was a sure thing, despite rapidly rising prices, supported by the RBA’s bold forecasts of low interest rates until ….

Should consumers carry the burden of their failures to be better economic forecasters than our government and the RBA?

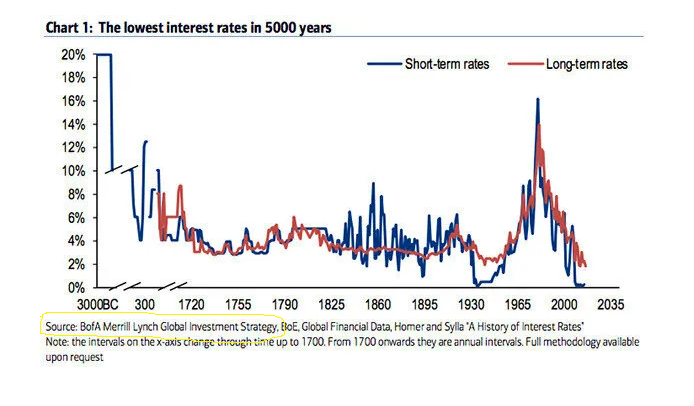

It’s tough economic medicine for an outcome the average consumer has no control over. There is one difference between now and the circumstances of the 1980-90’s. Back then a high interest rate was the norm, and lending ratios required a greater deposit than today. An increase of 2-4% over time on a home loan signed onto at 10-14% had a small impact, relative to today.

I can remember the RBA saying month after month for at least the last decade that they were concerned about the amount of debt being taken on by home buyers. But with inflation very low, and a sluggish economy, could do nothing about it.

APRA too was concerned, and required lenders to evaluate loans based on a minimum 2% above the prevailing interest rate. They were also concerned about the steep rise in fixed interest loans, especially interest only loans and directed lenders to reduce the number of these loans written by requiring more cash held to cover these riskier loans.

But still the borrowers piled into the property market, especially investors going after the overly generous tax benefits (I think some are more rorts). And state Governments threw first home buyer grants and stamp duty discounts around like lollies.

Well now that interest rates have to go up to combat inflation, the shakeup will be seen. Market analysts have been warning for years what could happen if interest rates had to rise steeply, or if a serious recession hit.

Whats that they say about those who ignore history are doomed to repeat it? This is what happened back in the late 70s, early 80s… cant recall exactly the dates… but I do remember the “mortgage cliff” being faced by many in Western Sydney (and probably in more locations) back then. People were having to just walk out of their houses because they just could not afford to keep paying. The reasons for it were different, but it happened.

Given a choice?

On one hand being a renter at the mercy of what to be honest is a poorly regulated short term rental market.

Or

Having the security and certainty of your own home.

For owners paying off the homes they live in.

What does an informed economist have to offer but cold comfort, and to also point out what is different? Consumers are left to ask whose interests our current financial system are best serving in this instance, given it can be done differently.

‘Australian households should prepare for many more rate hikes this year, experts warn - ABC News

Mr O’Donaghoe puts the interest down to frayed nerves about what has become one of the most aggressive tightening cycle in the Reserve Bank’s history.

.

“I think that reinforces just how sensitive Australian households are to RBA policy, because unlike in countries like the US, mortgage interest rates in Australia key directly off the cash rate,” he explains.

.

“This means that the household spending transmission mechanism in Australia is more powerful than it is elsewhere.”

No joy for renters, as the underlying costs of the more highly geared investors are also passed on. There are varied published expert views from leading economists in mainstream media on why and what might be done.

Nothing is assured. It’s suggested that if one asks 5 economists for their considered opinion you will get 10 different answers.

You may notice CHOICE staff have edited or removed some posts in this topic. Generally, taxation, macro-economics and discussions around the structure or alternative structures of government are not considered to be consumer issues, and are are therefore off topic for the CHOICE consumer forum.

While we understand there is some crossover of issues when discussing things from a macro perspective, the CHOICE forum is for discussing consumer issues such as the impact of rate rises on households. With that in mind, we’ve decided to keep this topic open for now for this purpose. We appreciate there’s frustration around this subject and that it can be tricky to untangle. If in doubt, you can always check in with a mod or CHOICE staff member. For reference, our guidelines are located here. We appreciate your patience and your assistance in keeping the Community a place for respectful, civilised discussion.

In 2008, as the price of oil surged above $140 a barrel, experts said it would soon hit $200; a few months later it plunged to $30. In 1967, they said the USSR would have one of the fastest-growing economies in the year 2000; in 2000, the USSR did not exist. In 1911, it was pronounced that there would be no more wars in Europe; we all know how that turned out. Face it, experts are about as accurate as dart-throwing monkeys.

Future Babble: Why Expert Predictions Fail - and Why We Believe Them Anyway

I have a different view about ‘negative gearing’. In the past I have used 100% gearing on property and unit trusts, but only as a short-term startup measure. Not a deliberate strategy to avoid or evade paying tax.

Investment income and expenses should be separated from employment income and expenses.

Capital gains and losses can be offset, but you cannot claim a capital loss against your employment income to reduce your net tax payable. In my view, you should not be able to claim excess investment costs, the main one being loan interest, against employment gross income to get you into a lower tax bracket.

Economics forecasters follow their models and use the current data to make predictions.

Not unlike weather forecasters.

Except that humans can’t in any short term way influence weather.

But humans can change market dynamics on a daily basis. Whether it be Gov decisions, a major conflict, a ship stuck in the Suez canal affecting global trade and supply.

I really don’t take much notice of economic predictions, just what actions are taken to deal with current market issues that are deemed problematic. Like inflation.

My cynical nature expects a ‘bombshell report’ that when all is said and done advises consumers to ‘shop around’ for the best interest rates. If there is a bonus it might be about transparency rather than change.

The banks are doing what they have always done. Comments about ‘why have an RC’ if nothing ever changes as a result suggests a few ‘turnips’ are getting frustrated. As one commentator made a point, bank executives make decisions to maximise their bonuses, not much else. There is truth to that in any industry so the underlying problem are many of the executive contracts and the boards of directors that sign off on them. It is capitalism at work and especially modern amoral neo-capitalism.