The federal govt changed the rules early January to increase age kids can stay on parent family plan from 25 to age 30. Unsurprisingly my health fund has not changed their policy to match. Does any one know of any funds who have? If so I will immediately jump ship and swim over to that fund!

1 Like

From what I have seen, it is increased to age 31. But that is from the start of April this year. So not yet applicable.

So when you start getting notifications from your health fund about how much your premiums are going up, ask the question.

1 Like

Note - per Canstar review.

Treasurer Josh Frydenberg said that from 1 April 2021, health insurers would be allowed to increase the age that dependants can stay on a family policy, from age 24 to age 31,

2 Likes

We are with HCF and the last I heard was that only dependants under 23 were covered unless they were a student. So our 23yo daughter is now without insurance. I stay with HCF as they are not for profit which I much prefer. We still have one daughter under 23 - will be interesting to see if HCF changes the age. Anyone know of any good not for profit health funds?

If you are a Choice member you can start here.

Be wary of sites like comparethemarket or iselect as they are owned and operated by insurance companies to tout their own products, and others are anecdotal rather than objective.

You can also get an idea from productreview.com.au noting all posts there are anecdotal and disgruntled members are more likely to post than happy ones. Those having made claims are the most relevant. Does one care that signup was easy without having experienced their service and benefits, or lack thereof?

3 Likes

I just did this and it suggested HCI (Healthcare Insurance) which is not for profit but has the same age limits for dependants as HCF and was more expensive than what we currently pay. So will stay with HCF for the time being.

1 Like

If your 23 year old is working, why would they not have their own insurance? When I started work at 17, I transferred from my parent’s plan onto my own plan (with HCF, by the way) and do I started with the maximum benefits as I was regarded as having been insured for longer than just when I started my own plan. In order to avoid the possible age penalty (which commences when you are 31) should she take up insurance later, it is better she start a policy sooner than later. Even if she finds a hospital cover only policy to start.

4 Likes

They would in the public scheme. Whether they should buy into private insurance is another matter with its own thread.

3 Likes

I cannot find any suggestion a referenced ‘dependent’ is working re this topic. These days lots of young people are in university until 28~30 getting advanced degrees or are unemployed or underdemployed and meet the tests for dependency.

2 Likes

I also think this has to do with the day that a person starts to accrue a Lifetime Health Cover (LHC) policy loading which is 31 years. They could start their own policy on the last possible day in July after they turn 31and not face this extra policy burden " In most cases, your Lifetime Health Cover base day is the later of 1 July 2000 or the 1 July following your 31st birthday".

Allowing a dependant “child” to remain covered until they turn 31 is in line with that LHC loading. So they could swap straight from a Family policy to a Singles policy. If they have disabilities and are still “dependant” then no age restriction will apply to them to remain on the family’s policy.

2 Likes

They won’t meet the legislated definition of dependency which is outlined here:

In Australia, child dependency expires when the child is 22 years old, providing that child meets the dependency requirements up until that age. It is worth noting that health insurance appears to be different (see below). I haven’t been able to be find what the definition for dependency is in such cases and could be different to the above one.

I am surprised that health funds allow children to remain on the parents health policy until ages greater than 22 years. It would be interesting to know the rationale for such as it is inconsistent with the legislated definition. It appears that the dependency for health insurance may be different to others:

The social security definition doesn’t differentiate between those with or without disabilities. However, for health cover, there appears to be a separate definition under insurance policies where those with disabilities don’t have a dependency which expires by the age of an individual.

2 Likes

From the Budget paper you provided indeed show that Disability is different

“From 1 April 2021, the Government will increase the maximum age of dependants for private health insurance policies from 24 to 31 years and remove the age limit for dependants with a disability”

and the link to LHC is made

“This will help provide continuity of care for younger Australians and encourage them to continue with PHI when they reach the age of 31, which is the age at which Lifetime Health Cover commences. Allowing dependants to remain on the family policy until the start of Lifetime Health Cover provides them with a clear moment for decision about maintaining their PHI, and increases PHI’s attractiveness to young people” (my highlighting)

Each Insurer can make a decision on when a person is covered to eg from currently 21 to 24 years of age (24 is the maximum), I would assume the 31 years of age will similarly be at the Insurers discretion of age cut-off.

3 Likes

We were, briefly. Refer to attached from BUPA.

There are two different circumstances covered. One is based only on age and the policy holder pays an extra amount to include an adult child until they turn 25. The other option for full time students does not incur an extra premium based on a family cover policy.

We had this policy in place for all of our children. It’s not automatic.

Whether BUPA carry both options forward or only one when the new rules come in?

4 Likes

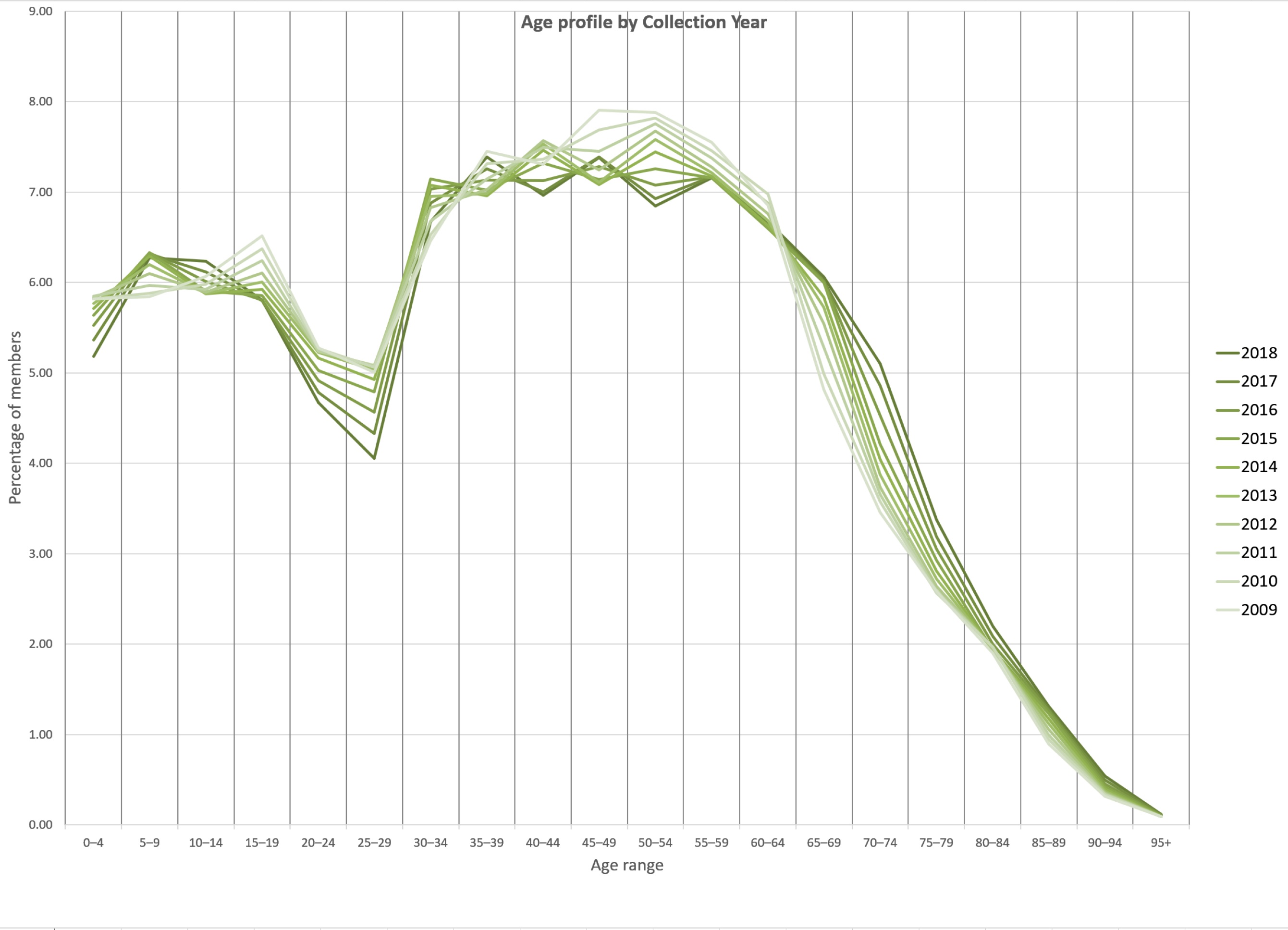

I think it likely that this move is an effort to remove the gap between premiums paid on behalf of dependants and when young adults re-join before the lifetime cover limit. There are many young people deserting the system during that interval.

This graph shows the problem:

https://choice.community/uploads/default/original/2X/0/011f70a9c056b3973582e0287bcf88c24f9058a7.jpeg

{kind=link}

To catch up with the wider issues have a look at the thread on Fix private health insurance

5 Likes

You could be right. The other idea I thought if is if they are retained under a parents cover until maximum of 31 years of age, it is likely that they will continue the cover when they are no longer classed as dependents. Maintaining insurance base when children are a little older…and they may think twice about cancelling any private health insurance, unlike the early twenty somethings when health isn’t an important issue.

3 Likes

Thank you for your thoughts. Our 23 yo has recently moved out of home as she wants to be independent even though she is only getting bits and pieces of paid employment (she did film at uni) and is most likely living off her savings. We of course will support her if she wants it. So she can’t afford private health insurance at present. Once she is earning a reasonable wage, then she may take up health cover but the public system will do for now, especially as she is young and healthy.

3 Likes

Check with your health insurance provider in their definition of a dependent. Check if your daughter not being a student and not living under the same roof qualifies under your policy. Hopefully the insurer agrees that they can be classed as a dependent as it is in their interests if your daughter plans to take out her own cover when she can afford to. The advantage of remaining under a parents covers is that some insurers roll over accumulated benefits to the children, then a child’s policy is started/rolled out from the parents policy.

An example of a dependent definition can be found on the Medibank website:

but note that each insurer may have different deinfitions and what qualifies as a dependent.

2 Likes

I did contact them at the time, when she was living at home and had just finished her uni and had no income. The only option I was given was for her (or us) to pay for a separate membership. So we decided she could do without for the time being.

3 Likes

This may change but the change only comes into effect on April 1st if a Health Fund chooses to increase the age level to 31. No policy will currently offer it until that date.

2 Likes

I guess you missed the operative word, right at the start if my question… IF…