I know of the issues with Dynamic Currency Conversion re: Cruise Ships/Overseas ATM’s etc (where the EFTPOS machine asks you if you want to be billed in your own currency based on the card issuer AUD$ and suffer exorbitant rip-off on forex fees), but have recently noticed it happening involuntary on shopping websites. One website in the E.U. I thought it might have been my mistake the first time, but the second time I was explicitly careful to select EUR € instead of DNS default AUD $ as my card (with Bankwest) has pretty close to mid market rates and is a good deal close to what it should be.

So I authorised the payment on my Mastercard for EUR€480,00 (equiv AUD$805.00) on that date - and was sent a confirmation email of AUD$896.00 and charged that on my Mastercard - a whopping $91.00 something for nothing that I specifically went out of my way to avoid.

No sense from Bankwest, they speak CommBank gibberish and all Mastercard scheme advice online is merchant based.

Has anyone had similar, I am not sure if it a “Shopify” site or DIY site and where Mastercard and ultimately AU/EU stand on this unauthorised behaviour which feels like a scam?

Was that the xrate published by Mastercard or another source? All the card companies do their own conversions and add their own markup on the published rates of the day. From my own experience a difference of about 3-5% is common. 11% seems usurious and would reflect an ‘instant conversion service’ as you suspect.

Terminals/payment systems offering to process in one’s home currency are, as you wrote, one of the biggest financial ripoffs a consumer can fall for. That ‘service’ is provided by the bank or processing company operating the terminal (payment system). The merchant may be unaware it is happening.

Routine transactional xrates are regulated by country so the location of the merchant and their payment processor matter. Any policy or regulation is thus country dependent although EU members act as a block.

To check if you have been scammed rather than were a victim of the Mastercard xrate of the day, your card statement should show (overtly or by clicking ‘detail’ on the line item - most issuers have that in their online systems) whether the charge was processed in € or $.

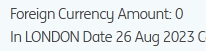

From a recent off shore transaction in $AUD, note the foreign currency notation is ‘0’ meaning it was processed in AUD. If it shows the € amount my understanding is it would have been processed as such and converted by Mastercard. A partial snip -

Yes, thank you I think you missed my point. My issue is not with Mastercard or Bankwest as I routinely purchase in foreign currency and the rate charged on the date of settlement is very close to mid market rates, not at issue.

At issue is the payment screen showed EUR€480,00 which I hit pay/process/enter whatever and the company in EU then did Dynamic Currency Conversion and I was billed (internationally of course), but in AUD$ at their rate - not Mastercard’s rate at settlement date, which would be what Bankwest would have then showed…

Below a typical forex example of USD$460 at Bankwest equiv AUD$694.79. Mid Market rate at Historical Rates Tables - USD | Xe is 460 X 1.503062938599915 equiv $691.40 so that is all good.

Then the second example it is just billed in AUD$, not in EUR at all so Mastercard/Bankwest not at issue here.

Nothing was missed. You answered what I asked about. While the merchant is probably an innocent bystander you might start with them, and move on to the platform while assuring maximum exposure to the apparent rort. Part of the process is determining what jurisdiction the payment platform operates in, and what relationships it has for processing.

Who monitors and what laws are (or are not) applicable can then be discovered.

You seem to believe that the exchange conversion will be done at your end by the credit/debit card issuer for the card you have.

Unfortunately while this can occur, the merchant might charge fees for some currencies used or different card types.

It may have been better to accept payment in AUD as you would have known what the price was in AUD. Accepting payment in EUR you don’t know the actual price in AUD until payment is processed. It is worth noting when travelling and paying AUDs for a exchanged currency is a good way to get terrible rates as the conversion is set by the ATM provider…it is similar for what you thought would be a better exchange rate.

Edit: changing to EUR might have also incurred two foreign exchange transactions, particularly if the business operates using a currency other than EUR. In such case, you could have been hit for fees for both exchanges (AUD to EUR and EUR to other currency). It is getting more difficult to determine the currency foreign websites use as indicated in other threads where consumers buying in AUD, from what looks at first glance an Australian business, have been hit with exchange fees.

FWIW the myriad ‘international business’ web sites that allow one to pick their currency of choice allows the customer to do an xrate comparison of their own. Set €EUR or $USD or whatever, then $AUD and see the offered comparative costs in $AUD. One can easily compute the comparative xrate.

In my personal experience the best currency deal depends on the locale of the ‘store’ or will be in $USD, but in recent times have found the $AUD price has often been reasonable against the other currencies; but sometimes there is a premium for our now volatile currency so I use my foreign transaction fee-free card in ‘the other’ currency, and it usually works to my benefit. But not always.

You might be doing the wrong thing by expecting the foreign currency to always give you a better deal when you receive the $AUD bill.