I am looking at getting travel insurance for international, including cruise.

In the past my first port of call… pardon the pun has been Choice magazine and I usually go with what they recommend.

Imagine my surprise that they have listed travel insurance companies with out recommending any. It looks as though the youngins have taken over Choice and expect us to read all the fine print.

Why have the current employees of choice not bothered to ‘grade’ the travel insurance policies from recommend to worst with a score?

Very frustrating I will now have to go to a profit site like Compare the Market…

It is possibly because each policy offers different level and extent of cover. An example being, some offer cruise cover, others it is optional and some don’t.

If you have access to Choice Online, it is easy to do a Compare All to see which ones offer cruise insurance:

The comparison also allows one to compare the level of cover across 91 different policies.

Possibly @JodiBird might be able to provide information on why Choice didn’t rate travel insurance policy, like it does with many consumer products.

Our experience of travel insurance includes changing needs with age. Our needs have also differed depending on where we are travelling, when and how? Add some snow sports or back country hiking and the best policy may not be the one for a guided tour of the local history spots.

It’s possible one policy does not best suit all. To also note policy costs and conditions can change. There is an interesting scenario played out with older travellers looking for travel insurance for an Antarctic cruise (aka Expedition). Calling it an expedition adds to the marketing allure. Evokes for me images of Scott of the Antarctic and others on expeditions to the land of ice or to reach the South Pole. Not surprisingly many of the better known insurers run away from the risk.

In the past, they did rate them. I have noticed that dont rate health insurance companies either. They seem to just do articles. Not like the Choice of old, where they took the time to rate them.

I wonder how long before they dont rate ovens, or kettles or anything else. Will they just write articles about things?

I can understand why there are no ratings. Consider the difficulty of developing a value system that might be applicable to any individual for any given travel. From my view rankings on anything excepting claims complaints would be tenuous at best and misleading at worst.

Perhaps Choice editors realised that and have since focused on providing easily comparable datapoints in lieu via the compare option. Scanning the ‘review article’ additional sorting options would be an improvement as might additional options in the filters, but it is fairly comprehensive in the comparison tables although lacking cruise-specifics, just whether it is an option in the policy.

As with many Choice reviews/articles of ‘soft goods’ like insurances, the gold standard is reading the respective PDS.

I looked at this recently too, and was also disappointed. What was offered gave me no indication of how easy any of them were to deal with and whether people who made claims on their insurance felt they were dealt with fairly. At the very least I’d expect something like the brand reliability rating that Choice gives electrical items. I hope they listen to our feedback. Anyone can collate information from insurance websites. We need more than that to assess their value and reliability.

I noticed that CHOICE have not tested/reviewed Domestic Travel Insurance for some time.

I am also disappointed they no longer give recommendations for insurances. Yes I can check the inclusions but it is equally important whether companies actually pay legitimate claims instead finding endless reasons for refuting them. With some companies it can take months and much presistence to get a claim paid.

I am unsure where Choice would get such data from.

They could survey policy holders, but, they are more likely to gain responses from those who have problems, biasing any conclusions.

They could ask the insurers, but would they give out data which could damage their reputation and future ability to gain customers.

The government could legislate that every business must report to a central administrating authority customer stats, such as number of customers, total number of claims/complaints, total number of claims/complaints resolved, total number of claims/complaints unresolved, number of claims/complaints being disputed etc, and regularly audit every business to confirm accuracy. Could be expensive exercise for the taxpayer/consumer when costs are passed on.

I don’t think there is currently an easy solution to find reliable data that can be used for assessment and scoring purposes.

When we take out domestic/international insurance we always look at online reviews. This has often shown a mixed bag of feedback - no company seems better than the other. We end up deciding on the cover which best meets our needs . It is worth noting for other insurance we use a broker which provides anecdotal evidence of their own (or industry) experiences. This helps in the decision making process.

@MEG_12 We will get scoring and recommendations back up on the international travel insurance comparison in July (domestic later in the year). The delay is due to the entire travel insurance market re-writing their policies post Covid travel bans. We’re only catching up on re-building our database of policy and price data now.

I can assure you the young uns don’t like reading the fine print either. If anything, I’ve found they’re less likely to read it.

Be warned that travel insurance comparisons on sites such as Compare the Market or Canstar can be misleading. When I checked for my last trip, a travel insurance product that was very highly rated on Canstar also had extremely poor reviews on productreview.com because they found excuses to avoid paying most claims. It’s important to also check the track record (for paying genuine claims) of the company backing the insurer you choose.

@Patanty we have ‘Satisfaction scores’ for car and home insurance, which is a combination of customer satisfaction with claims and customer service overall. This is also listed on our home insurance comparison and going up on our car insurance comparison soon. We didn’t get enough responses for travel insurance for it to be representative, so we haven’t published it there.

Claims satisfaction would be the holy grail, but due to the low rate of policyholders that actually claim (particularly for travel insurance), it’s very difficult to do it using a survey based method. You need very large sample sizes so you can capture the small percentage of people that actually claimed on their policy.

We explored this for travel insurance once, but the research company we spoke to told us the large sample sizes required jeopardise control of how representative the sample population is (i.e. for gender, age, state etc). So even if you could afford to survey using large sample populations, you end up with a dodgy set of data anyway.

The best way to get accurate claims data would be if ASIC mandated claims reporting and made this public, as they do with life insurance. We’ve asked many times, and will continue to push for this.

Alternatively if AFCA returned to reporting complaints as a proportion of policies issued, instead of absolute complaint numbers, that would also be helpful (again, we’ve asked many times, and will continue to push this).

@JodiBird How is the Travel Insurance scoring and recommendations going? Do you have an update as to when Choice are going list the recommendations?

I am delaying purchasing my travel insurance, as I am waiting on Choice’s scoring.

Sorry for the late reply @MEG_12, it’s been a busy month. The scoring and recommendations are now back up on the international travel insurance comparison for the annual and single trip products. Please feel free to post any feedback here.

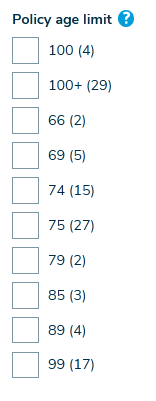

Wouldn’t it be more useful as a filter if, using an example, 85 (3) was 85 (57) because policies covering 85 (3), 89 (4), 99 (17), 100 (4), and 100+ (29) would all be applicable to an 85 year old? One can tick all those boxes, but.

Thanks @PhilT. I’ll have a play around with the filter to see if I can get that option to work. One day I’d like to have the insurance comparisons in a tool similar to our health insurance comparison, but until then, it requires me to do some data manipulation to make these things as user friendly as possible.

Insurance is not easy to assess,

Firstly, look at the prime reason why one should insure, namely to get an honest claim fairly and promptly met, forget the cheapest premium which is only the reasoning prior to needing to claim.

There is only one way to assess this, by comparing how the various insurance companies have performed over a significant number of similar claims, this requires the collection of a large amount of significant data from people with both good, bad and mixed claim experience from the relevant insurers. Also the special circumstances relating to a claim. An example I can give is my son’s Motor claim from several years ago where the treatment he received from RACQ can be described as shabby. He was stationery in a row of cars at a red traffic light when he was rear ended by a ute, and driven forcibly into the rear of the vehicle in front, which in turn damaged the car 2 ahead of him.

You can’t be more in the right than that. My son’s car was a write off, he had owned the vehicle less than 6 months, it had been purchased for $8000, and was insured by RACQ for $7500.

The ute that caused the carnage was also insured by RACQ, in dealing with my son’s claim he was offered $4200 by RACQ, we protested and provided irrefutable evidence that the market value of Mitzi Lancers of the same year, distanced traveled and condition were all above $6000, The RACQ assessor then took the stance $4200, take it it leave it, not negotiable and no explanation. The pay out was not sufficient to clear the outstanding finance of $4800

My guess it was claims cost mitigation, if the driver responsible had been insured with other than RACQ they could have recovered the cost from the other insurer.

As a consequence I wouldn’t insure anything with RACQ at any price, and will tell this story to anyone who asks.

Unfortunately, many people don’t read their insurance documents and write such reviews after they find they aren’t actually covered for the loss.

What happened when you presented the driver at fault with a letter of demand for the loss? After all, the driver is responsible, they are just indemnified by the insurance company.