Malwarebytes and ad blockers get in the way of many reviews presented in popups or redirections. As for the quality of reviews, 1 star awarded for a premium increase - well OK, but all companies play that game…a snip of the first bit of them is

If one compares the policies they are not so different but the quotes were $100 apart. Differences in claims/complaints handling in 2021? I cannot comment.

To make a long story short, I received a quote for renewing my car for $965, but when I went online “pretending” to get a quote for the same car the number was $766. NEARLY $200 difference, when I have had home building, home contents, 2 car comprehensive for over 20 years with the company.

Now the detail.

I have 2013 Hyundai i40 “Elite” wagon, the mid spec, of 3 levels

Out of curiosity I checked the lower level price and it came at $752. When queried I was told about the “factors”, but no one in Chat could tell what the specifics of my car where. I got the quote reviewed to $900.

Then I got a quote for the top of the range model which came at $825, a whopping $140 over my mid spec car. Contacted Chat again, and essentially was told that a computer decides the rates.

Then I did what I should have done first, had the shock not disabled my thinking, resulting in the aforementioned $ 766 against “my” $ 965.

I wrote to the company, requesting an explanation. For now I won’t mention the name.

Every year we get quotes for car insurance when it is due for renewal, which is easy to do online…but can take a little time. The renewal notice is used as a reminder to do quotes.

We do contact current insurer to get their best deal to keep us as a customer… However, most years we switch companies providing car insurance as we often can get a better deal elsewhere.

There are things to watch though, often each quoted policy will be different and have different inclusions and exclusions. This includes things like car hire for X days, windscreen replacement, vehicle contents or modifications etc where some policies they are included while others they are add-ons.

Excesses and market/agreed replacement values can also be substantially different and while one policy may be substantially cheaper, so might be the payout if written off. Standard excesses in cheaper premiums may also be higher.

Other things to watch are excesses for unlisted drivers against the policy (say a friend or family member driving the car) and younger drivers if this potentially applies to you.

We go through each policy PDS and usually the cheapest one isn’t the best for one or more of the above reasons. We find we usually select cover which suits our risk profile and generally is in the lower to middle cost range.

Has anyone else had a problem getting a realistic agreed insurance value, which takes into account current market values, when renewing car insurance? When checking the renewal for my wife’s low mileage one owner hatchback with the top 2 recommended insurers in WA we found that the maximum agreed value was $8,800 yet the Red Book value is between $9,300 - $10,900.

Hi @clubman I have moved your post into the Car Insurance review topic.

Your question is an interesting one, I personally haven’t noticed this with our insurers. We always insure for agreed value and twice we have moved the value up without ‘fight back’ from the insurer (AAMI and APIA). I would assume that we still had values within Red Book values but both cars were extremely low kilometreage but not pristine enough to achieve maximum values but were in very good to excellent condition at the time we increased the insured values.

Perhaps others here have had the same issue you have had and it may be something that CHOICE may be interested in as well. I’m sure it will make others aware to take notice to inspect their insurance values.

that is market value. As you correctly note, if insured for market value it will be the wholesale price a dealer would pay for the vehicle, usually not more than the bottom of the trade value range regardless of how good the vehicle might be.

I thought car insurance policies covered the value of the car at the time it was written off – in insurance terms the ‘retail market value at the point of total loss.’

From an AAMI policy - the covered amount is the agreed value or the market value as shown on the policy document, subject to certain adjustments… an APIA policy is the same, both are the same underwriter.

we will pay you the amount covered shown on your certificate of insurance less any deductions that apply.

When we pay you for a total loss claim we will deduct the following where applicable, from the amount we pay you: • excesses; • unpaid premium including any unpaid instalments for the period of insurance; • any unused registration and compulsory third party/motor accident injuries insurance (unless we decide to collect this from the relevant authority or insurer, in which case you must help us if we ask); • any input tax credit entitlement, see page 65; • our estimate of the salvage value; (in context, if one wants to keep the wreck) • any excesses arising from a claim for damage to the hire car (see ‘Hire car conditions’ page 35). Where we provide you with a new car you will have to pay us any of the above applicable deductions.

I have never been asked regarding the colour of any vehicle I have ever insured and Qld Rego Check does not list the colour of vehicles so I fail to see how insurance companies would know vehicle colours.

If they actually did, I could understand why pearl paints would attract higher premiums, as well as red cars, as everyone knows that red cars go faster.

Some of the quote systems have asked. It doesn’t seem to be routine though. Curious. They have all asked about metallic paint (in the manufacturer accessories).

Higher cost of repaint if it is metallic so premiums are adjusted for the cost. White and Black are the two that generally come free with a new car purchase, metallics are definitely dearer. White Pearl is considered metallic.

Can someone please let me know what might be a good (cheap) insurance company if I need to insure 4 cars. Pd Insurance is good, but they are starting to get more expensive.

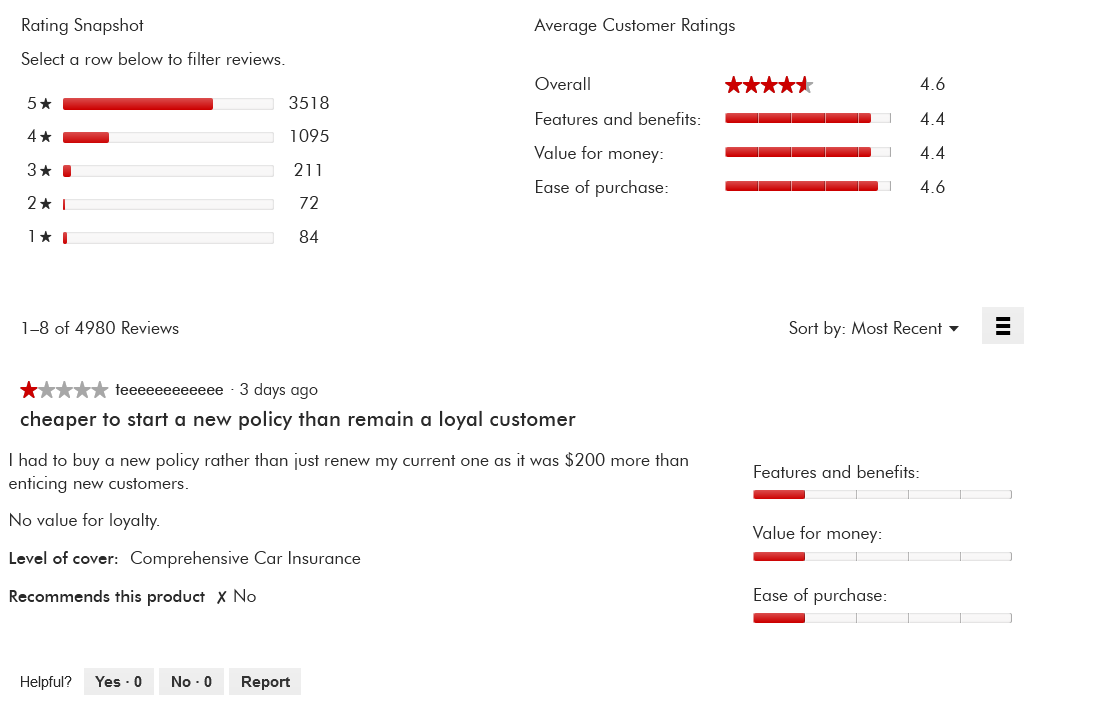

Choice has a guide linked above (it takes one to the 2021 ‘review’), and it depends on where you live, the vehicles, driver age(s), whether private or business, and so many other things. One consistent element is that insurers have ‘introductory quotes’ in year one and depend on the customer just renewing for large increases in subsequent years. It usually pays to get quotes every year including with one’s current company, and buy a new policy every year rather than renewing.

Although you might see some useful guidance in this topic it is so individual your best option is to either use an insurance broker or get your own online quotes - what is best for me is only best for me, not necessarily for you - to make the point.