The wording was perhaps lax. I think you are saying that you don’t have a legal right to use cash. So let’s try instead: We are on the cusp of losing our personal financial opportunity of choosing to pay by Australian Legal Tender.

I’ve said it before but I’ll say it again: We will lose the opportunity of choosing to pay by cash unless people start acting to avoid this. Use it or lose it. Don’t pay by card. Start using cash again.

One challenge with this is the rise of online shopping, where cash is nearly always not an option and credit card is the most widely accepted payment mechanism (and for international purchases credit card is almost exclusively the only accepted payment mechanism).

The pandemic was also a challenge for cash where “pay wave” was a way of minimising shared physical contact with anything (but then incurring a credit card surcharge, where the merchant chooses to apply one).

Then change to a different bank and tell ANZ why you are doing so.

You still have a branch?

I guess if you are really worried then you should buy your first X uncontroversial items at the supermarket, to reach the minimum purchase value that allows cash out, getting cash out with the purchase, then go back in and buy the remaining items anonymously, then go off to another store to pay cash for any other items that you require. Or change bank.

OT but relevant to many no longer in the workforce full time. The credit credentials offered by the next bank will not always reflect the possibly generous assessments carried with the bank one has used for many years previously. Banks tend to favour income over assets when making their assessments. A relevant topic for those interested.

‘Retirees being denied credit - #93 by PhilT

This is not correct. ANZ has announced that some branches will no longer have over the counter cash transactions. However you will still be able to deposit and withdraw cash via a machine at that branch, with staff assistance if required.

“Businesses don’t have to accept cash” - Does that include Government Services? If so, is that not undemocratic to change the definition of legal tender… the legal tender of the people of Australia.

I could do exactly that but where to? All the other banks will follow the way of the big boys and they will do what ever they want if we don’t question these things now.

Not sure if the ANZ understood exactly what it was saying here. What came first, customers not using branches as often because it’s too easy not to or customers not using branches because the ANZ has taken them away?

“Our customers are changing how they bank with more than a 50 per cent decline in branch transactions across ANZ over the past four years.

“Only eight per cent of our customers solely rely on branches for their everyday banking needs, with the majority preferring online and mobile banking methods.

Fortunately, if you can find an ANZ branch the friendly staff are there to assist in training customers to do all transactions at the ATM.

Depending of course on whether you want credit. You can use a debit card, or you can use EFTPOS, both of which are cashless.

For the record, what I suggested (change to a different bank) may also fail if you have been a victim of any of the recent mass data breaches and as a consequence have locked your credit record (again, in respect of getting a credit card).

Already have a credit card with Commbank as I said. I’m trying to get it paid off, I’d rather not have to use it. OTOH there are things I cannot afford otherwise, and my estate will ultimately pay the bill that remains. Already have debit card with Macquarie and use it for all small(ish) purchases.

I needed petrol in Gundagai. My rewards discounts info (Coles, Woolies, RACV, Linkt, …) are all via apps. Aldimobile/Telstra showed a strong 3G signal but multiple devices (phone and iPad w/SIM) got nothing but ‘network errors’. I finally paid with my card at full price and got my token points having been able to swipe the physical rewards card.

While each discount would have been modest individually in aggregate they would have been more than $5, a coffee or coldie, lost because of ‘network errors’. I am so enthused about the online life we [have to] lead. Not!

Another instalment of new found but old problems is reflected in the last paragraph,

‘problems for people who won’t – or can’t – adapt to a more digital climate, such as the elderly or people with carers who don’t want to hand over their bank cards.’

Most banks mandate no passwords or PINS be shared or revealed or ‘the fraud is on the customer’. How does that work when the customer cannot go out and about themselves? Many aspects of banking will have to evolve to support reality, either by choice or governmental actions.

Power of Attorney (PoA) is one way that this can be formalised. In that case the person holding PoA is him- or herself identified to the bank and operating the account - so no PINs or passwords need be shared or revealed.

A trust account is an alternative to PoA.

Both are of course open to fraud and depend on a level of trust existing - but that is no different from a straight out sharing of PINs.

PoA’s are not magical as many institutions have their own forms and some will decline to accept standard ones regardless of how legal they might be. There are a few relevant posts discoverable on the Community.

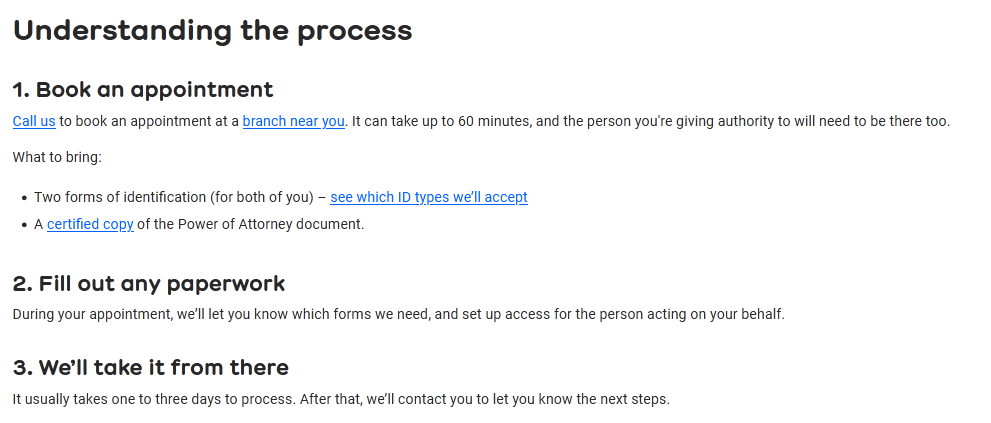

They can also be a pain to initiate. From Bankwest for example.

An alternative that may suit some is to open a joint account with the other your trusted support/loved one. It was one solution we have used. It enables the trusted person to have a seperate card, pin, online access and transact as for everyday. It keeps one’s personal account access seperate, and any funds there less accessible to all others.

The account need only hold sufficient funds for the weekly or what ever needs. Topping up? Easy for those who trust phone or online banking from home. Not an option for others. Requesting your trusted one to pay by direct debit (most transactions these days) produces an audit trail for yourself and others.

We’ve also been through the route of being an authorised person with an EPOA. Too long a story for today.

Curiosity is a solicitor will readily come to Aged Care or Rehab in hospital for all and any needs. Banks? It would be useful to hear of any experiences where the bank would offer a similar level of service.