Why was your insurance company involved at all? If the at-fault person is 100% liable and since they are insured then their insurance company should be the one to pay you out (assuming the other party make a claim). They don’t have a contract with you limiting the payout, although you would probably have had the same issues with a lowball initial offer.

Now that you have made a claim, some insurers will increase your premiums in the future - even for at fault claims. And it clearly wasn’t easier for you even though you pay the insurance company to do the running around for you.

As @maryrhodes had an accident, most, if not all, insurers require the disclosure. Even if no claim was made through them, the insurers can increase the policy premiums or decline to renew. It isn’t always a simple process no matter which way a claimant goes.

Sometimes it is less stressful to deal with your own insurer to settle an accident claim. An example being that the other driver was uninsured or the other driver was telling their insurer one thing (e.g. accident not their fault), but others a different story.

Insurance companies (and some brokers) also provide such service and why one pays a premium with them. It is hoped that they represent their client over the insurer’s best interests.

Many individuals aren’t comfortable being forceful with negotiations with a business they have no relationship with.

My understanding is that an accident where a driver is not at fault (0% liability), this isn’t considered a claim where there is a full settlement through the other party. This is because the risk profile of the insured driver hasn’t changed. Maybe @Peterchu who worked in insurance can confirm is this is the case from his past experience.

It is still a claim. Many insurance companies do not increase premiums for not at fault claims, but I have personal experience of at least one that does.

That is fine, and totally different to making a claim.

I don’t see any explanation in post #2. In this case the at fault party was identified, was fully insured, and it is hard to argue that it was easier to deal with your own insurance company in this case…

Issues such as car hire are a non-event, in fact while the third party is liable for car hire if required, your own insurance may not pay for it.

I wonder if anyone receiving a renewal in recent times with the price of used vehicle up smartly, has an agreed value offer (or range) that is higher than last year considering the ‘replacement/market’ value is higher than last year.

Snap!

Both are policies with Suncorp have increased the value of the vehicle by approx 25% compared to last year. The premium increase a more modest 4.2% approx.

P.S.

Not that we asked for an increase, knowing the increased value of used vehicles why not.

As a Not At Fault driver, you are entitled by law to the full replacement cost of your vehicle, plus a like for like hire car paid for by the at fault driver or their insurance company.

If you have a claim number from the at fault driver, a company such as “I’m In The Right” (for whom I work) will provide you with a replacement vehicle and negotiate on your behalf with the insurance company to get you the full amount you are due - with nothing charged to you as the not at fault driver. I know of one person who did this, and received $9,000 more than the insurance company offered for the written off vehicle.

Insurance companies try to minimise costs. Your insurance covers you if you are at fault - so whether you have market value or a fixed value in your insurance policy is irrelevant if you are not at fault.

Spectre Law won a case in the High Court in December 2021 against Australian insurers, where the court confirmed that the not at fault driver is entitled to be put back in the position they were in prior to the accident. That includes the provision of a like-for-like hire car, and current replacement cost o your written off vehicle. Spectre Law is part of the I’m In The Right group of companies, so maybe give them a call for an unbiased view of your options.

Thank you for pointing out the action in the High Court and outcome.

Assume this is one part of the decision you are referring to?

Choice members and consumers are free to choose to argue their position directly with their insurer, or alternately seek support from a number of sources including their local law firms.

Promoting a business as per following??

P.S.

Also of note

Drivers who accept vehicles from credit hire companies after car accidents could be left thousands of dollars out of pocket following a series of NSW Supreme Court decisions.

You are right. There are many results of the High Court decision. Now that the decision has been made, the outcomes are set in place.

Also with the decision made, it means that not at fault drivers have available to them the legal option to be returned to the position they were in prior to the accident.

Insurers generally won’t tell them that though.

If you have had a not at fault accident and your insurer wants to pay out at under the replacement cost, you could look at other options.

In relation to the judgement, the case deals with the reasonableness of provision of a like for like hire car and is silent on a decision associated with assessing the current replacement cost for a written off vehicle. Indicating otherwise for this particular judgement is misleading.

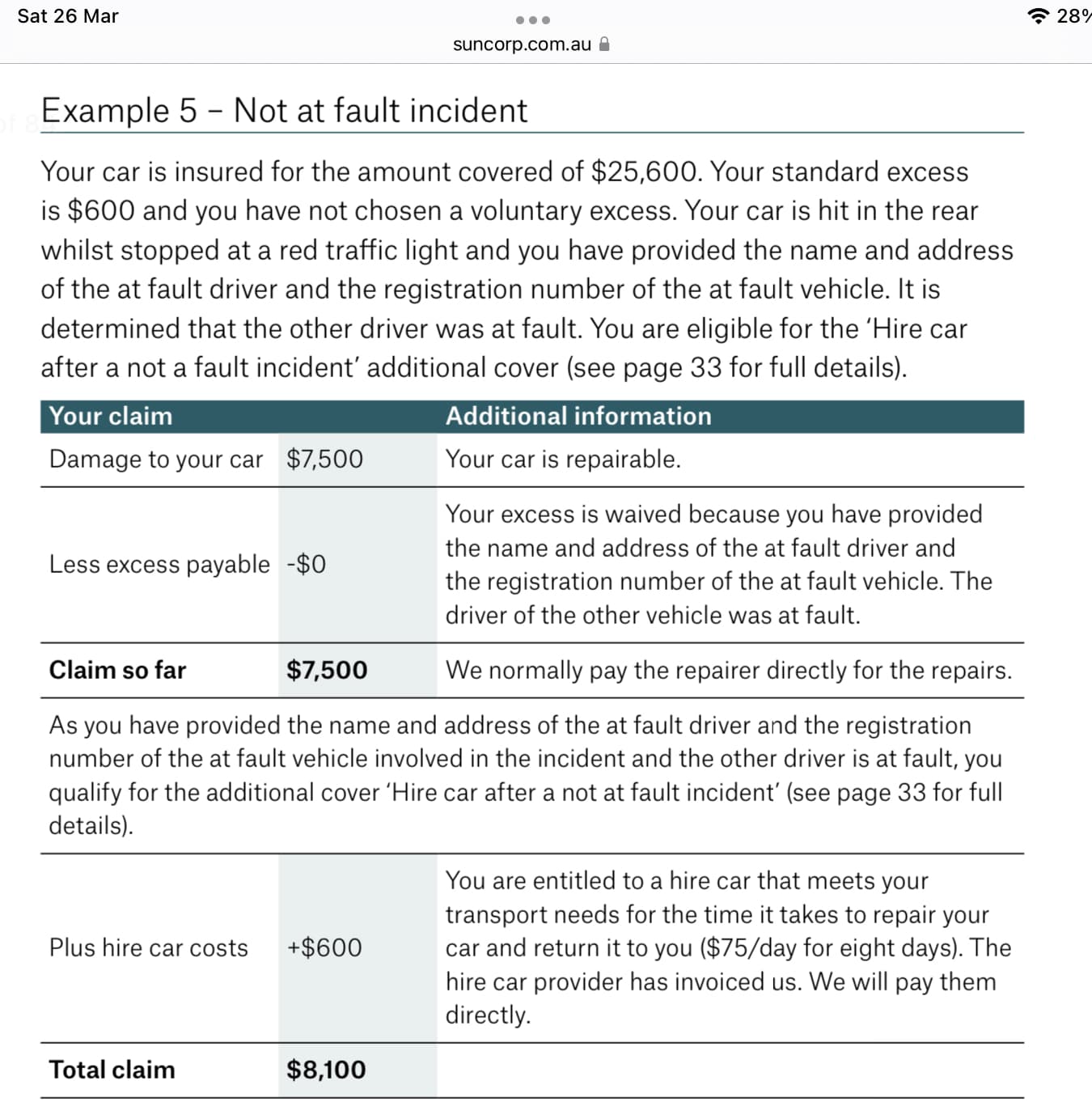

I struggled to find any clarification on how Suncorp assess a not at fault claim for a written of vehicle. They provide an example for a repairable vehicle that indicates zero cost to the owner (other claims excluded). Although there is some clarity regarding a hire vehicle.