Well now I am quite confused as you said the insurers were being deceptive hiding the exclusion in the fine print. If you read it and understood it how were you deceived?

I don’t think I mentioned underinsurance, voluntary extensions or alterations.

So a building can be damaged so badly that the remains must be demolished in order to rebuild and then it can be rebuilt according to the outdated standard?

It isn’t the insurer that offers the like-for-like coverage who invokes the upgrade, there are two parts to this problem, it would be clearer if we keep them separate.

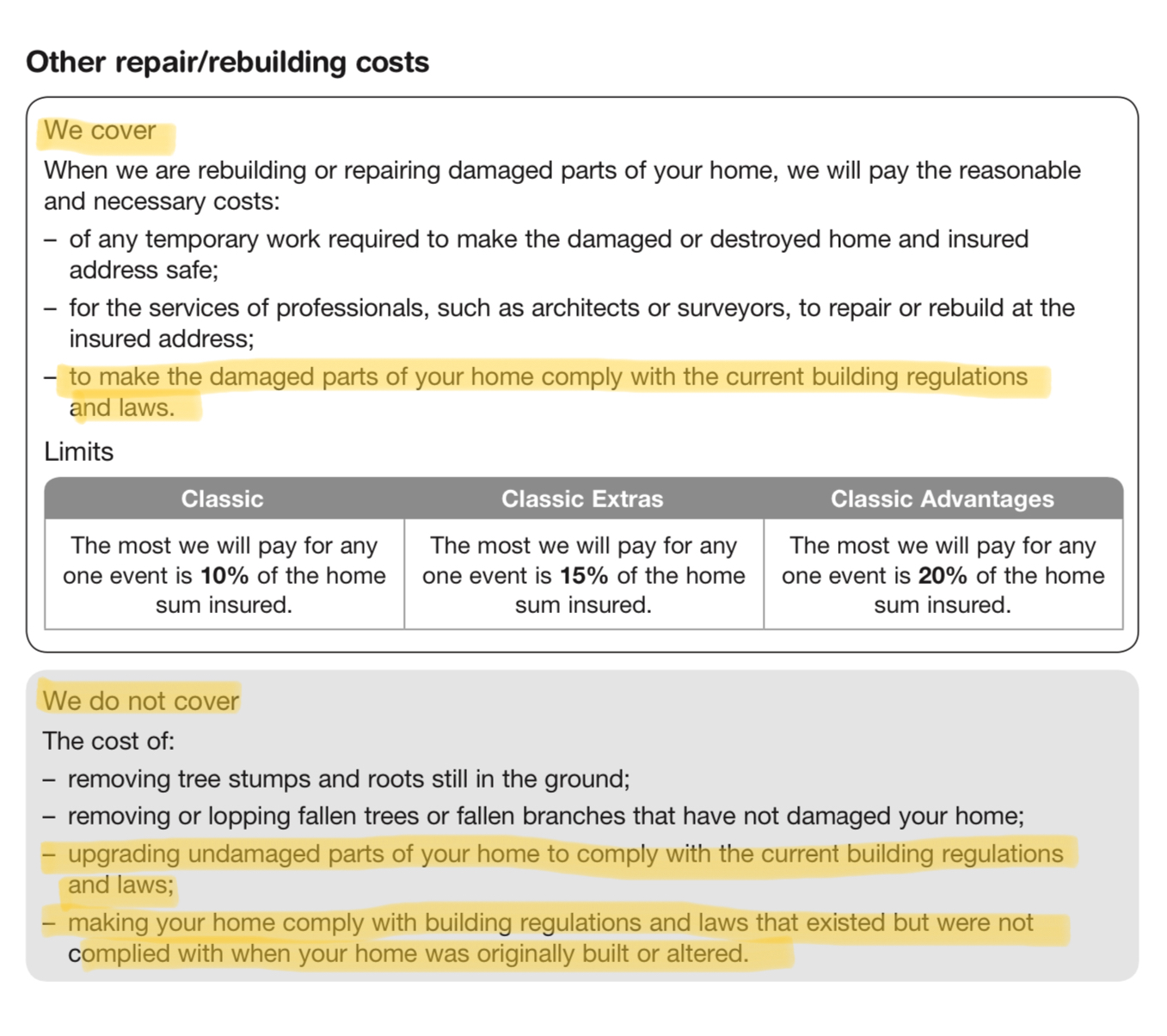

Building/planning approvals are covered by an insurance policy, along with making works comply with existing standards.

When determining the replacement value of the property (total insured amount), this should be based on the replacement value and not to rebuild to the same standard as it was built in the past. The rebuild should include any approvals required to facilitate the rebuild.

If one choses to reduce the estimated replacement value, then underinsurance would occur. If one estimates the true replacement value, then this is the value of replacement to the standards/code at the time of replacement.

If a house is badly damaged and needs to be demolished and replaced, then this is also covered by an insurance policy.

If a house is damaged and works needed to make good, these works will be carried out to the current standards which apply for the works.

If for example the wiring in the whole of the house is found to be non-compliant (say it is of an age the the insulation is cracking, this isn’t an insurance issue but a maintenance issue. If a homeowner choses not to replace all the wiring when repairs to damage subject of a insurance claim is carried out, then this would be unwise as it may void any future claims as it will be known that the wiring is non-compliant.

Insurance companies also can’t ignore local planning/building approval requirements nor building codes when carrying out their work. If they did, then this would potentially be seen as negligent.

But there is a clear exclusion. As @syncretic suggested, this is a seperate issue. What insurers choose to cover is one. What the approvals may require is a second.

Yes. That’s entirely my point. It will remain a time-bomb for all home owners until the insurance industry and regulators recognize the real needs of home owners work together to solve it.

Yes, so the insurance companies are underestimating the true replacement cost, and incorrectly advising their customers, but then forcing the customers to wear the consequences of the bad advice.

The “remains” don’t need to be demolished. Most of the house is undamaged. The problem is caused by insurers and building regulators keeping the problems separate, behaving legalistically to protect themselves instead of working together to provide good outcomes for home owners.

I wasn’t commenting on your specific case but trying to tease out your position on the broader question. When is it reasonable for authorities to say the building is too damaged to make good by the old standard? You have said 50% isn’t fair in your view, so what is?

I don’t care as long as the insurance companies and building regulators recognise the issue and work together to inform house owners of the effect of their rules in advance and ensure that it is all covered by the insurance.

It would be interesting to know who your insurer is and also what local government area you live. It would also be useful to know what the damage is and what the challenges is you are facing with the local authority and building regulator. This might allow the community to provide comment on your specifics rather than trying to second guess what the problem is.

Thanks, phb. We still have a long way to go with the insurer and regulations before we out them. The purpose of my post was to warn others of the danger they face, and to find out if anyone actually has a policy which does not contain the flaw.

There is a potential gap in common home insurance policies cover. The gap only arises,

where there is a substantial repair,

where a need to upgrade the undamaged portion of the property can be demonstrated,

where the responsible approvals will not provide concessions

where the additional upgrade costs are outside the means of the owner

From the exclusions in existing policies it is evident insurers have not provided to cover the gap in this specific set of circumstances. Although as previously pointed out they would in the instance the property was a total loss.

In respect of upgrades under building regulations and (National Construction Code - NCC). Each state has different requirements including concessions or discretionary advice for repairs to properties partially damaged through fire, cyclones, floods etc. For some states or insured events the gap may never need to be considered. IE the requirement for upgrading is able to be varied in specific curcumstances.

Prior to significant upgrades, EG cyclone rated roofing and tie downs, updating older homes to bush fire protection rating, AC (fibro) roofing and cladding etc, such properties unimproved sell at a discount to the market. It may be prudent to upgrade the whole of a damaged property, even if partly from your own pocket.

The specific gap is something all home owners could have covered (potentially through premium increases). For many newer homes, or those purposefully improving their homes it might be pointless.

Alternately is that extra gap cover an optional extra for those home owners most at risk. EG Home owners in tropical cyclone areas get discounted premiums based on the ratings of their properties. The industry does have the ability to differentiate.

It would be IFF one has the economic resources. In many cases that doesn’t exist, and after a major event may not exist in a practical sense at the time.

Excepting in most cases it seems their ‘ability’ is to reject cover or present a ‘take it or leave it’ rather than tailor a policy.

That 50% damage clause is interesting in itself. We might reliably guess who determines 50% versus 49% versus 51% to maximise P/L and minimise payouts yet how often would it be close in actuality? Even if only once per 10,000 claims and it was ‘your’ claim, ‘you’ would become most interested in the issue.

mark-m:

I accept your offer to buy my damaged house for $600,00 because you believe if you pay another $200,000 to upgrade it you will be able to sell it for more than $800,00, which you appear to claim is viable.

Thank you also for offering to provide a copy of your house insurance which undertakes to cover the costs of all upgrades to the undamaged portion.

Both the local council Planning regulations and the VBA regulations have similar 50% clauses. The council ones are interpreted by council Planning staff. The VBA ones are interpreted by private Building Surveyors. Both are highly subjective and discretionary, so the outcome depends on pot luck, and a waiver from one does not at all ensure a waiver from the other. Council verbally offered me a waiver, but have not yet provided it in writing. The insurer has so far chosen to follow their own Building Surveyor, though I have the right to appoint one myself, if I can find one who is more reasonable.

This relates to my claim also. The PDS states that repairs will meet building regs for the damaged parts of the home, however the insured event caused damage to 50% or more of the home. It seems logical therefore that the insurer and their repairer should meet this regulation unless otherwise stated. If not, they’re writing their own rules when it comes to building regs and/or their building surveyors are not being impartial.

FYI I’m just a consumer so take it with a grain of salt if you don’t agree

If I’m understanding this conversation, if more than 50% of a home were destroyed by fire or storm (or whatever), the remaining part would need to be upgraded to current fire or storm standards.

The cladding might need to be changed, the roof reinforced, windows and screens changed, or the whole house rewired. BUT, you can’t use any of your insurance money to do that. Is that the story?

Does that mean you couldn’t plan to rebuild a smaller, updated home with your insurance money? Depending on the size and layout of a house, I could see some people willing to cut off a couple of bedrooms or a garage so they could afford to rebuild and repair what’s left to current standards.

That’s the observation, although it is a council building approval requirement. It can vary between different authorities, and some may give concessions.

Insurance policies typically only offer to upgrade the portion replaced to current building standards. Hence the disconnect. An assumption is policies would cost even more if a partly damaged property required the whole of the property to be upgraded to the latest building codes. It might require the 50% of the property not damaged to be demolished prior as upgrading is impractical, or too costly.

The least expensive option is for councils and state govts to provide concessions to the home owners caught out. Just how many homes this has applied to over previous years has not been mentioned. It may not be that many. In which instance the insurers and governments are both creating un-necessarily great distress for a handful of home owners lucky enough to have not quite half a home saved, and unlucky enough to loose everything?

Let’s say you have home insurance for $1,000,000 for a house with a granny flat, and the flat and enough of the house are destroyed to equal more than 50% of the property.

What if you decide you don’t want to replace the granny flat? Is it the insurance company who benefits by paying only to rebuild the part of the house that’s gone? You’re still up for any costs to bring the remainder up to specs, right?

Do they pay up to a million dollars of cost to replace the flat and half-house?

So to get your money’s worth, so to speak, could you rebuild the granny flat and part house (the 51% that’s gone) to current standards and make that bit your home and demolish the old part? Or do you have to replace the rooms the same way they used to be?

Someone else might like to comment.

Hypotheticals are always open to multiple responses, none of which may be correct or all of which may be correct, or something else.

Firstly will your local council and state planning approve the demolition?

Secondly what does the policy provide for, and what might the insurer agree to?

Double guessing either could be risky, especially with scope for insurers and councils to all have differing views across the nation. It’s worth reading through the topic from the beginning, as well as reading carefully the pds of one’s own home insurance policy.

This would possibly trigger an investigation into whether the house was underinsured. This poses its own risks which are covered in this other post…

Hypotheticals are difficult to say what the outcome is as it will be dependent on the type of cover, what caused the damage, what the specific insurance policy says etc.