Community rating was not invented by any Oz govmint but we do seem to take it further than some other countries. In part this is what I was getting at when I questioned if it sensible to call it insurance.

To balance the books there has to be a degree of the wealthy subsidising the poor and the healthy subsidising the sick. If it was all user pays you would end up with those most in need being asked to pay sums that they would never have the capacity to earn and it would not be any kind of public health system. So making the system voluntary is never going to work - which is the current semi-private scheme.

it isn’t exactly meaningful to attribute dollars of revenue to dollars of expenditure - it all goes into consolidated revenue

your ATO Notice of Assessment comes with a breakdown showing how much the health system costs you personally in tax (which at the moment therefore allows you to compare that with your personal Medicare Levy amount and see how much larger the former figure is)

Two things I found interesting from the speakers for the private system.

Firstly, they recognise the problem (people are starting to behave rationally) but say that better ‘messaging’ will correct the slide. Secondly, if the private system folds there will be havoc in the public system.

I don’t see any evidence that either of those things are true. While ever paying a lot extra is optional it is open to people to make the decision to not pay while they are young and healthy and to pay when they are older and need it. The second statement seems to be part of an effort to lobby for more subsidy. Sure there would be havoc if the private system was allowed to crash and burn but that is a straw man argument because no government will allow it to happen.

The idea of doing away with community ratings is canvassed, an age based risk system is mentioned. So as you get older and sicker your fees go up. For all but the wealthy that means when you need health care the most will be when you can afford it the least. I thought ‘health insurance’ was designed to get over that problem.

The core of the problem is for any such system to work the young and healthy have to subsidise the old and sick. That will only happen if it is compulsory. If you don’t do this you will have the system in the USA prior to Obamacare (that many conservatives want to return to) where health outcomes were directly and strongly related to wealth and ‘health care’ was a prized perquisite of better paying jobs. Some institutions provided services at less than cost because they had access to other funds but the outcome was a very lumpy and uncertain level of service that was anything but universal health care.

Our private system was sold on the basis that by paying a bit extra you got extra. People are starting to realise that is not good value for money. There are two ways to exit the spiral without having collapses where funds just cease trading and go broke. You can increase public subsidies (which is what the industry wants) or you can carefully dismantle it before it crashes.

The more you increase public subsidy to the private stream he more the whole health system becomes publicly funded but in two tiers. Tell me again, why do we want a two tier system? Oh yes one is labeled ‘public’ and the other is labeled ‘private’, that is bound to provide universal health care. And along the way somebody needs to tell me why the public purse needs to keep subsidising private enterprise in this way when there is another way out.

Dismantling will require courage and foresight and the ability to convince the public at large that it is a necessity despite the screeching of vested interests. Which is why it will be kicked down the road by whoever is in power until the crisis is upon us.

So what about healthy people who suddenly become unhealthy and have been paying next to nothing for health cover for years? Who is subsidising whom?

If private health insurance is to work at all, what is paid early in life should be protection against paying more later in life when the risk is greater. Asking the aged population to pay even more when they can least afford it (for most) is also not a solution.

There are other models and options?

In one medical future should we all get titanium hip and knee replacements in our 50’s. IE when we are most able to withstand the surgery and recover effectively. The perfect preventative procedure? Dentistry has been prescribing similar for years, starting with the denture revolution to amalgam filling of molars just in case or all wisdom teeth must be removed by 40!

There is no sign of any change to the trend nor any activity in place that will arrest the slide. If we are going to get updates every few months saying another twenty, thirty or fourty thousand have quit how long will it be before the feds take action?

Is this just more policy paralysis or are they going to attempt to let it die? Dissolution may be the best solution in the end but dissolution through inaction will get very messy with very bad PR so I am guessing the first.

I wonder what the medical professionals are considering is required. What needs to happen to ensure their relative to the rest of the community, high levels of income are maintained?

This is not intended to be a shot at whether the incomes are justified. They simply represent a very significant and influential vested interest. The same might be said of the privately owned medical service providers. Those who benefit from the current but shrinking pool of private patients.

What would the privately owned business models ask in a public only service, the end of private cover, where the government is responsible for the costs?

The easy option for government is Medicare for all with no limits on the excess fees medical practices, services and providers can charge. Back to the consumer always pays a gap as their are no limits and no insurance! Electoral suicide perhaps? Long cues at the state run public hospitals when all you need is an annual checkup. That was how my grandparents survived back in the 1960’s and long before the update to universal health care. Private cover was available, but with limitations and a very different form of policy.

Interestingly, none of us know for sure how much all the big funds currently hold cash or invested funds. Who owns those assets might be another source of great angst and pain?

It is worth reading the APRA Quarterly Report as it is not as dire as the Conversation makes out…

The report indicates private health insurance general treatment membership has remain relatively constant…noting a slight increase of 1,237 insured persons over the quarter.

Hospital treatment insurance is also relatively stable over the past 12 months with number of policies declining by about 1500 (5.5M in total), while number of members insured increasing slightly by around 8000 (11.2M in total).

Unfortunately both the Conversation and Grattan Institure have constantly knocked Australia’s private health system and government support of the industry. Many of their articles cherry pick data to portray a different picture to the reality. This is why it is important to go to the original data sources (APRA) …that linked above.

In reality, from December 2018 to December 2019, membership has been relatively stable with some minor variations within each of the subset data/membership groups.

It is also likely that hospital treatment insurance has been impacted by the potential crackdown on junk hospital insurance polices. Such policies have been highlighted by Choice in the past…

That does not mean the system is stable. If the equilibrium is obtained by similar numbers of young healthy people leaving and old unhealthy people joining the death spiral is still in progress.

The APRA report shows us that for general treatment 70yo members cost about 150% of 30yo members and for hospital about 400%. What it doesn’t show (that I can see) is the change in age profile over time.

The graph supplied by the Grattan Institute this week shows a steady decline over the last 5 years from 47.3 to 44% of the population having private cover and over the same period the average age of members went from 40.6 to 42.1 years I don’t see what it cherry picked about those figures. They tend to support the idea that young people are leaving.

What we need is the age profile over the last decade overlaid as a 3D column chart …

Using young member data only is flawed, as younger generation may join, then leave as there is no penalties…and they can easily change their membership starus due to changing financial situations. I suspect the data also includes move off parents/guardians policies where a decision is made not to have cover at that point in time.

Once they reach the age cap for reduced premiums, it is a different matter and why often memberhip increases as age increases to prevent the applied financial penalties.

This is why looking over the dara set as a whole is important as looking as specific subdata may have underlying influences.

The average age of the population is also getting older which would influence to some degree the average age of policy holders. If average age remained static or declining, then Grattan’s/The Conversation conclusions are plausible, but increasing average population age is somewhat ignored.

Not correcting for aging population shows a direct bias to the reported information.

True but I wasn’t aware that had happened, I was just pointing out that the total membership change from last year to this doesn’t tell us much on its own.

What we need is to look at the age profile of members over time. None of the reports mentioned do it AFAICS. However APRA have an interesting spreadsheet. I will see what I can do with it.

That’s right, and how membership within each age profile changes on a year on year basis. One also needs to look at the change in membership as each member ages.

One also needs to look at whether there is a statistical difference over time, if the deviations are within the normal variation within the age profile and as members age.

It would be also interesting to know the effect of the private health insurance age loading, particularly for age groups immediately before and after when age loading comes into effect (age of 30).

The other thing which would require more intensive research is why there is particular trends (upward or downward) in particular age groups.

It would also be worth doing the above using metrics which consider the total population and change in current membership numbers. As Australia’s population is increasing, using population statistics itself may show a reduction in % members within the population, whereby, actual membership numbers have increased slightly.

I think you are making this harder than it needs to be. All that, and other suggestions you made, would be very interesting but I don’t think it is required to answer the key question. Not to mention the data may not be public.

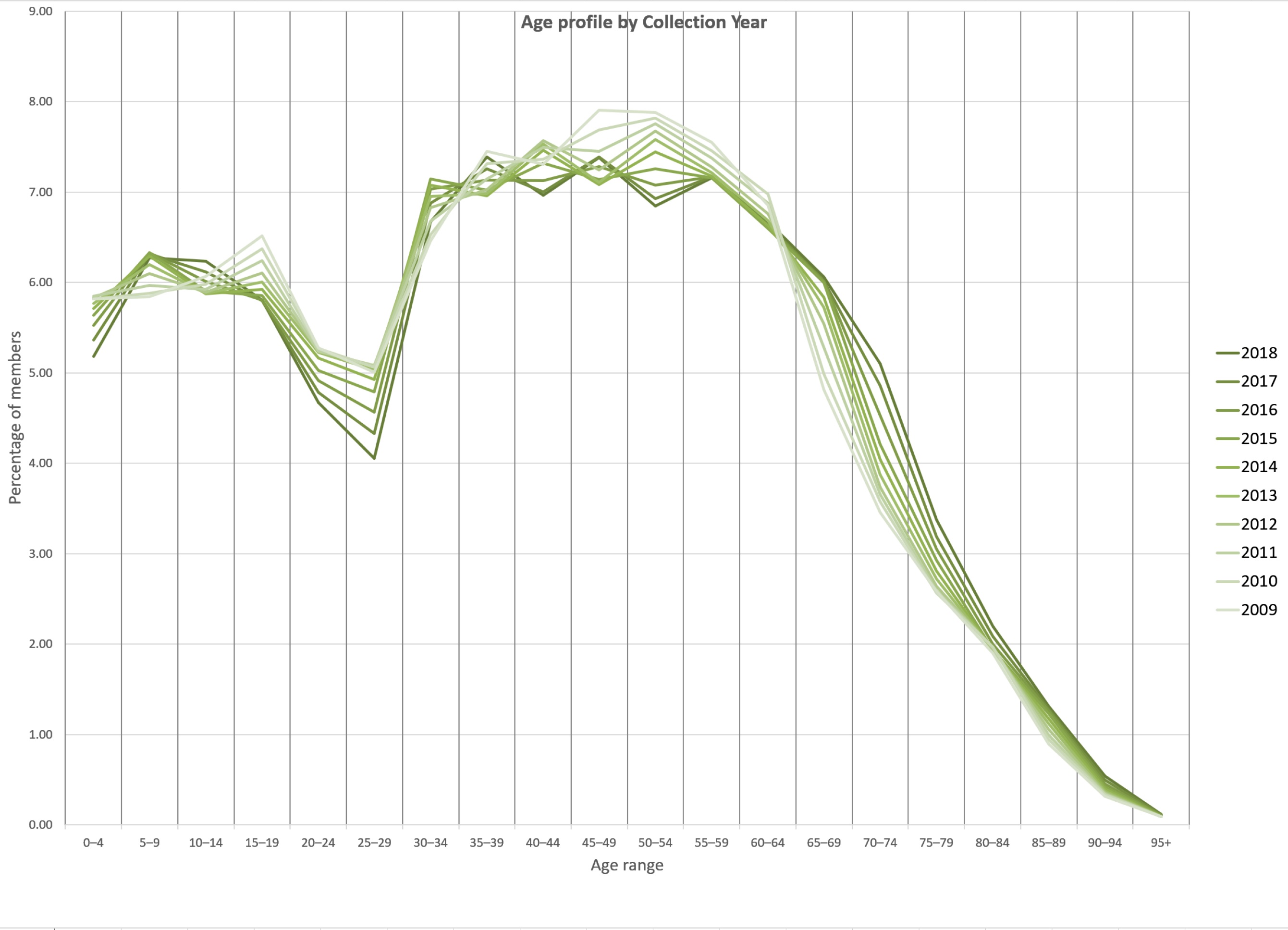

I have dived into the APRA annual statistics spreadsheet (shudder) and graphed the last ten years available. I cannot find the raw data for year ending 2019, there is a PDF (link above) but it shows graphs not tables. The spreadsheet ends in 2018 so we are not going to get the “45,000 young people who left in the last year”. However the results are still interesting.

I have graphed the percentage of private health members age range by year. I tried to do a 3D chart but it was too hard to read so it is a overlaid line chart.

Disclaimer: spreadsheets are the work of the devil, it is too easy to make mistakes and to munge data and not realise it. I have done my best to process this carefully but I have nobody to double check the work which I would do if I was doing this in business. So you have to take it as is.

The Conversation/Grattan Inst. articles focus on the question of young people leaving private health insurance. The chart shows the change in age profile for all reasons. It may be that this is due to members joining or leaving, members ageing or something else. However to address the question - are the funds sustainable - we can still get useful information. The reason is that age is a key determinant of costs, the funds need young people who claim less to cover old people who claim more.

The charts shows pretty much what we expect:

minors are there because they are on their parents’ membership,

between 19 and 30 young adults can opt out with no penalty,

joining after 31 penalties apply so people join up before then,

the numbers drop off from about 60 as members die.

Now look at the differences over the ten year span. The hole between 19 and 30 gets progressively deeper from 2009 to 2018 and the decline from 65 to 80 becomes less (higher values) from 2009 to 2018. Notice also the changes are getting faster between the more recent years.

For whatever reason the membership profile has progressively aged over ten years and it is accelerating.

I believe the majority of the effect is the young voting with their feet and jumping once they are independent and not re-joining until just before the penalty age. The degree to which this effect explains the changes may determine the options for saving the funds but this chart says to me unless some action is taken the death spiral is inevitable.

That’s probably the key government policy. It costs the taxpayer nothing (at least not directly) and yet does seem to be effective at what it is trying to achieve. (By contrast, the PHI subsidy / rebate does have a direct cost to the taxpayer.) Perhaps the government should be looking to phase the penalty age down from 30 to say 25.

However I think you are both making things more complicated than it needs to be … the bottom line is how much it costs. That’s what customers, even involuntary ones, look at. If the cost in real terms continues to rise - regardless of the reasons, regardless of the age profile, … - then that is an increasing problem.

So the challenge on health funds is to contain costs.

What is also interesting is that eventhough the 20 somethings are less likely to join private health at that age, when they get to early 30s, it seems that the lower membership nunbers of the 20 somethings doesn’t impact on the levels in the 30s+.

It also appears that the age loading is a major influence in the uptake of private health.

Both can destroy the system. Even if costs are contained in the sense of the price of goods and services if the membership issue isn’t dealt with the system will fail. The membership problem is especially difficult because it is self-intensifying, it is non-linear.

Great presentation of the movements in membership over time.

Is the explanation the baby boomers are filtering through the data as a distinct one off bump. Post baby boomers the birth rate fell, and population growth has declined. It is not just about the baby boomers coming through as they age and fewer younger people signing up. It is that there are simply less people proportionally in each of the younger age groups that follow to draw new members from.

The trends in immigration over time might also find a bump, if not in numbers in the age groups being added to the citizenship pool over time. Is there a skew in this statistic because immigrants are on average older than 30 when they enter the system through citizenship?

It doesn’t change the nature of the problem facing the system? It might however challenge that simply reducing the no penalty joining age will deliver a low cost solution.

Perhaps the real solution is the obvious but too hard for some of constraining more directly the costs of service delivery?