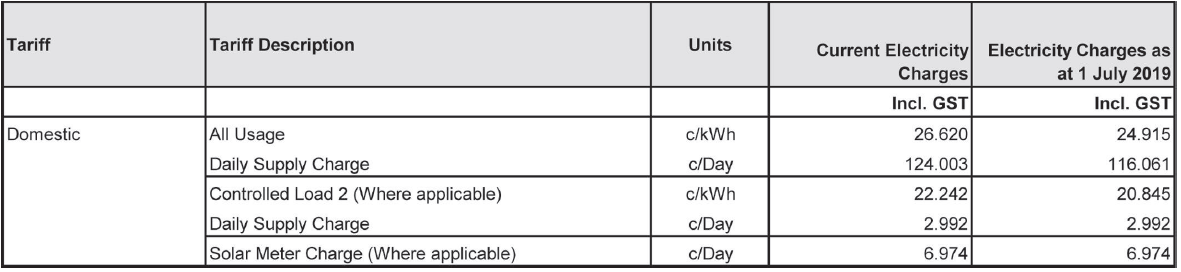

Getting back to the original topic about current energy price rises, it might be interesting to see what default market offers have been made by the Energy retailers to forum members. This is one from Origin for Brisbane:

What is pleasing is both the energy component and the daily supply charge have decreased for Tariff 11 (standard tariff)…on the energy component for off peak (Tariff 33) has also decreased slightly.

It appears the ABC headline can be interpreted two different ways.

Looking at the detail in the report might offer a different understanding?

Firstly the report is looking at the wholesale market rate (cost of generation). This is approx one third only of the average electricity bill!

The second consideration is that for coal fired generation the overall costs of operation are not linear. This is due to the inherent design of the plant that is aligned to constant load while daily demand varies. The report considers how solar PV is affecting one part only of the daily demand cycle, and how the NEM market pricing is structured.

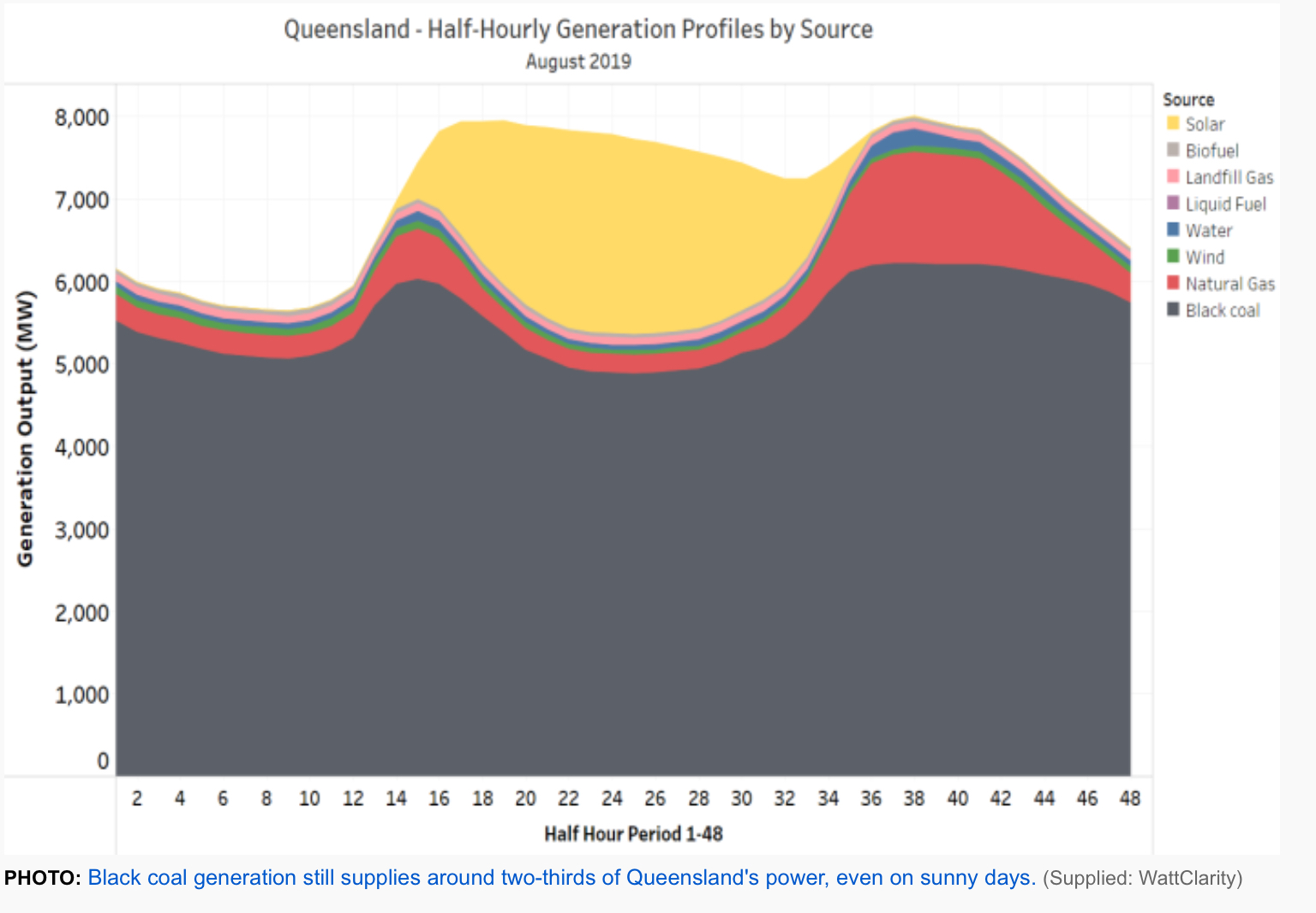

The complexity of the discussion is evident in the following graph from the ABC report.

P.s.

As a separate discussion point from the complex market pricing in the ABC report.

While for the Qld example, black coal power still has peaks in the morning and evening, it is the red graphic that is also a significant provider of peak power for August. Red represents natural gas generation, which is very expensive compared to coal.

Renewables such as Solar PV need the support of large scale pumped storage, grid sized batteries, and increased residential distributed battery storage to substitute for as much of the daily peak demand. Although any benefits of further investment and development in these remain some time off.

From what I understand, it isn’t about the price but ability to provide rapid network support.

Natural Gas has a very different generation profile to coal. Coal it is very difficult to have fast ramp up and ramp down of generation.

I suspect that AEMO requires coal generators to provide a constant generation output based on the average expected daily demand…which can be estimated. AEMO would be setting a coal generation level to ensure that coal generation doesn’t cause an overloading of the network. As it is difficult to ramp up/down quickly, the generation level set for coal would be conservative and shortfalls made up with gas generation.

The renewable generation component is not constant and varied due a wide range of factors. Some days (even with the same day) renewable generation will be very high making the need for gas generation support less (renewables would meet much of the shortfall between coal fire generation and demand)…while other days the renewable generation will be low requiring a greater need for gas support in conjunction with renewables. As the renewable generation is highly variable temporally, gas would be needed to buffer this variation (for August in Qld, the area of the red on the the graph).

It would possibly be concerning if there was no gas generation as it could indicate that there may be a over-generation event and there was a likelihood that different generation types are removed from supply to the network. This could include coal fired generation where coal is burnt, but no electricity is exported onto the grid from the generators (not an efficient outcome).

These are the most expensive form of network storage and are very expensive compared to hydro storage…which is currently the first level storage being adopted.

As indicated in another thread, if battery storage for excess renewable generation was only used to support the grid in times where there was a generation deficit, the average consumer electricity bills would go through the roof. There have been costs such as $1.5T to maintain current reliability standards (or around $10K/yr per household) and to meet future electricity demands (inc. when electricity replaces.traditional fossil fuel uses).

Pity the consumer trying to make sense of it all. Audrey Zibelman (Australian Energy Market Operator CEO) has compared running the grid of the future to conducting an orchestra. It’s complicated. We’re in transition, which only compounds the complexity.

At present, we have:

Coal generators which must be kept running (the origin of the term “base load”).

Gas turbine generators, which are increasingly expensive, but can start up quickly.

Renewables, which have variable, but very cost-effective output.

Pumped hydro, which originated as a way to store some of the base load that would otherwise have gone to waste.

Batteries which are not great for bulk energy storage, but excel at rapid response, frequency control and grid stabilisation.

June 2018. So little has changed, although Snowy 2 has now had the support of two consecutive Prime Ministers. Well sort of.

However, as is evident in the previous post, and from the ACCC assessment, the current NEM pricing mechanism fails to deliver lower power costs for consumers.

As ACCC indicated, higher prices usually encourage more investment in supply (generation). Such model fits the well established supply, demand and cost curves taught to first year economic students. This curve generally exists where there is free and open markets, and where there is a demand and supply of a particular goods/service.

What is also taught is that intervention within the free market by government (or say business) impacts on the curve and its relationships, thus potentially biasing the curve in the particular direction of the interaction/intervention.

In the case of electricity and more so in recent times, there has been both government and business intervention in the electricity market such that increased prices (through supply not meeting demand or through externalities) has not resulted in investment to increase supply (generation).

That ACCC attributed increased prices as primarily due to ‘policy failures’, which in hindsight have been more about governments not taking action, rather than decisive market interference by government.

‘Business intervention’, is that not the free market exercising it’s will?

Reducing electricity security and supply so that it leads to increased prices, is not the way to run an essential service. How high does the cost of supply need to climb before the market responds? And for electrical supply the lead times for new investment, design and approval and construction are significant.

P.s.

Without a price on carbon or legislated controls over emissions, what would the free market deliver? And assuming government assures the free market of a 50 year economic and profitable future for any new investment? Would it the path forward be more about policy, to which the market is still free to respond?

Yes, in a true market, but the electricity sector is not a true market as it is dominated by a limited number of players, cost of entry is very high (which prevent new participants) and the players which are there, can easily affect the market by their actions.

I suggest it isn’t about not taking action, but the policy direction of government changing like the wind (which includes both previous LNP and APL governments).

Energy investment is for the long term and not a 3 year election cycle.

When the sector was majority public owned, long term decisions were made as it was the public which had an interest and also benefited from long term electricity security. When private sector was invited into the sector along with other externalities, the interest changed and long term decision making became even more difficult.

Yeah from the articles and reports on current affairs eg Drum this legislation will not work very well. I feel that it’s a bit of noise so the Government can look like they are for the citizens when in fact it produces that noise but no other effect.

I see supply and demand charts but but I don’t see any with dollars. How would you get anybody to pay for capital cost of the excess production and building the hydrogen ships unless there is good prospects of a return?

Don’t get me wrong, I would love to see some of the forecasts in RenewEconomy come about but the problem with zealots is they tend to get very excited with only half the picture.

An article regarding the Australian Energy Market Commission outlining changes needed to reform Australia’s electricity grids and power pricing including fairer feed-in tariffs.

Our regional Qld monopoly rocket scientists, Ergon Energy, changed their tariffs as of 01.07.2019 with the daily “Service Fee” rising from $0.97843 to $0.99380, a rise of 1.6%, General Tariff 11 dropping from $0.27828/kwk to $0.26027/kwh, a decrease of 6.5%, and the Solar Feed-in Tariff dropping from $0.09369 to $0.07842 a decrease of 16.3%.

Ergon very conveniently failed to show the old FIT on their webpage so as to try to try to avoid consumers seeing how much they are being ripped off but had the termerity to state this.

“If you receive the solar feed-in tariff, this will decrease slightly from 9.4 cents to 7.8 cents to reflect a reduction in wholesale energy costs.”

If Ergon seriously considers that a decrease of 16.3% is a slight decrease, then little wonder electricity prices are out of control.

In 2018, the average spot price in Queensland was $72.87/MW (7.3c/kW). This year they are slightly higher averaging around $80.29/MW (8.3ckW) so far. The revised FIT is within the average spot price last year and so far this year.

The last time the average spot price was around 9.4c/kW was in 2017, when the average spot price was $93.13/MW.