Hydrogen is a lot of hot air personally.But we seem to be heading in the right direction but slowly in Australia for our own future when it comes to electricity

It is very cold actually. But seriously, there is currently research focusing on a two stage hydrogen from water which they hope reduces hydrogen costs to at least $2/kg (Bill Gates has also invested in the research program). Some are talking even lower costs. If this is the case, hydrogen will be far cheaper than other energy options for private transportation bsuch as cars, trucks and buses.

There is also emerging research about storing hydrogen in gels rather than the volatile gas, which could also he a game changer.

The discussion points to high energy conversion efficiency of 98.7% and suggests a

production cost as low as US$1/kg.

The H2 produced is delivered at high pressure (100bar) which is advantageous in subsequent transport or storage.

The intended market - is industrial use, which suggests that the H2 delivered may need further processing (added costs) for transportation.

Note:

The purity of the H2 produced has not been commented on in the referenced article. Hydrogen fuel cells require very high purity H2 (>99.97%) to prevent damage to the catalyst. The maximum permitted level of contaminants in the gas varies with sulphur at 4ppb one of the most stringent. Ref ISO 14687-2

1 Like

Hydrogen fuel cells is only one use of hydrogen gas, and could be considered a interim technology like battery or hybrid systems. Conversion of ICE to hydrogen is also possible, as well as research being does and trialing hydrogen (and other gas) combustion engines.

Hydrogen has one of the highest energy density values per mass. Its energy density is between 120 (33.333kWh) and 142 MJ/kg (39.444kWh). Diesel is around 34-40MJ/L and petrol 36-50MJL. This gives a hydrogen an energy density of around 3 times that of conventional vehicle fuels and if the $1/kg is achieved, it would be less than the cost for these existing fuels (if taxes are removed). Should the research eventuate in industrial scale production, this will be a game changer for hydrogen gas in the transport and industrial industries.

This shouldn’t be required if the purity of use in hydrogen combustion engines ensures combustion efficiency is still achieved. Any impurities which may exist, assuming they do, will possibly be driven lower for emissions from combustion engines, rather than ability to use the hydrogen gas.

Discussing with a friend who is a ecologist and sustainability consultant, and who has done extensive work in the alpine salt brine areas in the Andes, he shares the same concern that the drive for lithium will result in loss/extinction of fragile alpine ecosystems. Any technologies to prevent these extinctions should be explored.

The current situation is that more than 50% of world supply of Lithium comes from Australia. And ramping up production fast. Last time I looked at an atlas the Andes is a long way away.

While H2 is derived from Coal or other Fossil Fuels it is not environmentally friendly, simply put if you release CO2 to make H2 it is still “burning coal” to produce the energy.

There has been discussion of how clean H2 is, and yes it is but only if not made from carbon sources. As exactly GregR put it, and nor should there be other contaminants or extremely low levels of them if produced from water.

Until that day H2 is “dirty”.

1 Like

Other countries are doing the same and will continue to increase extraction as the demand for lithium grows. Some lithium will hopefully be recycled, but this will be a small percentage of total expected demand if electric cars and electric battery systems using existing lithium technologies are delivered.

While the Andes may be a long way away, it is likely that many of the battery products in Australia contain lithium from high environmental impact areas, as currently almost all lithium battery technologies are manufactured overseas and imported. While it may be a long way away, it has some of the cheapest and highest quality deposits in the world. While production in Chile has slipped as a percentage of world production in past years (their production growth has been a lot slower than other producing nations), there are plans by the Chilean government to accelerate and capitalise on its lithium competitive advantage and the region containing about 50% of known lithium reserves). There are many big world players, such as LG, Samsung, which have entered into long term contracts with Chilean producers to secure supply for their anticipated long term demand. What happens in Chile has direct bearing on Australia, even with the distance being far.

Actually the cheapest and highest quality deposits are in Australia. From Lithium containing rock deposits. A mineral called spodumene.

In Chile and Argentina and Bolivia it is from super salty brine deposits that need to pumped up and that processing method is the prime problem in ecosystems with depletion of natural lakes.

The reserves in seawater are millions of times more than in land deposits but as yet extraction is not yet economic due to the lower concentration. But given that the price of Lithium is bound to rise considerably, it will come into the picture.

BUT, we are off topic.

Yes and no?

There is another topic that looks to the local production of lithium and the manufacturing of batteries.

The implications for independence of supply and availability from from local manufacture are broad.

Home batteries, BEV’s, grid support, GHG reductions, Transport including air services.

Hydrogen and derived products are expected to compete as energy storage and portable energy sources. Which ever option/s best suit different needs Australia’s ability to be independent of external supply chains will factor into the suitability of each option for a particular need.

2 Likes

I would expect that Hydrogen will become part of the mix of energy sources used in Australia in the future. But it is not as attractive here as it is in Japan, where they have to import almost all of their energy sources. Their nuclear power is in crisis after the Fukushima disaster, and they need lots of LNG and coal for their power. Hydrogen is desirable because they will need it to try and meet CO2 reductions.

My worry is that Governments in Australia are looking at all that coal we have and the employment and communities involved in the digging up the stuff, and thinking what can we do with it.

Electricity producers don’t want to keep burning it. Not economic anymore.

Other countries are seeing it the same way.

So let’s turn it into Hydrogen, or other gas, and subsidise some companies to show it can be done. Don’t worry about the CO2 emitted at the pilot stage. That will be taken care of at some later stage. Somehow.

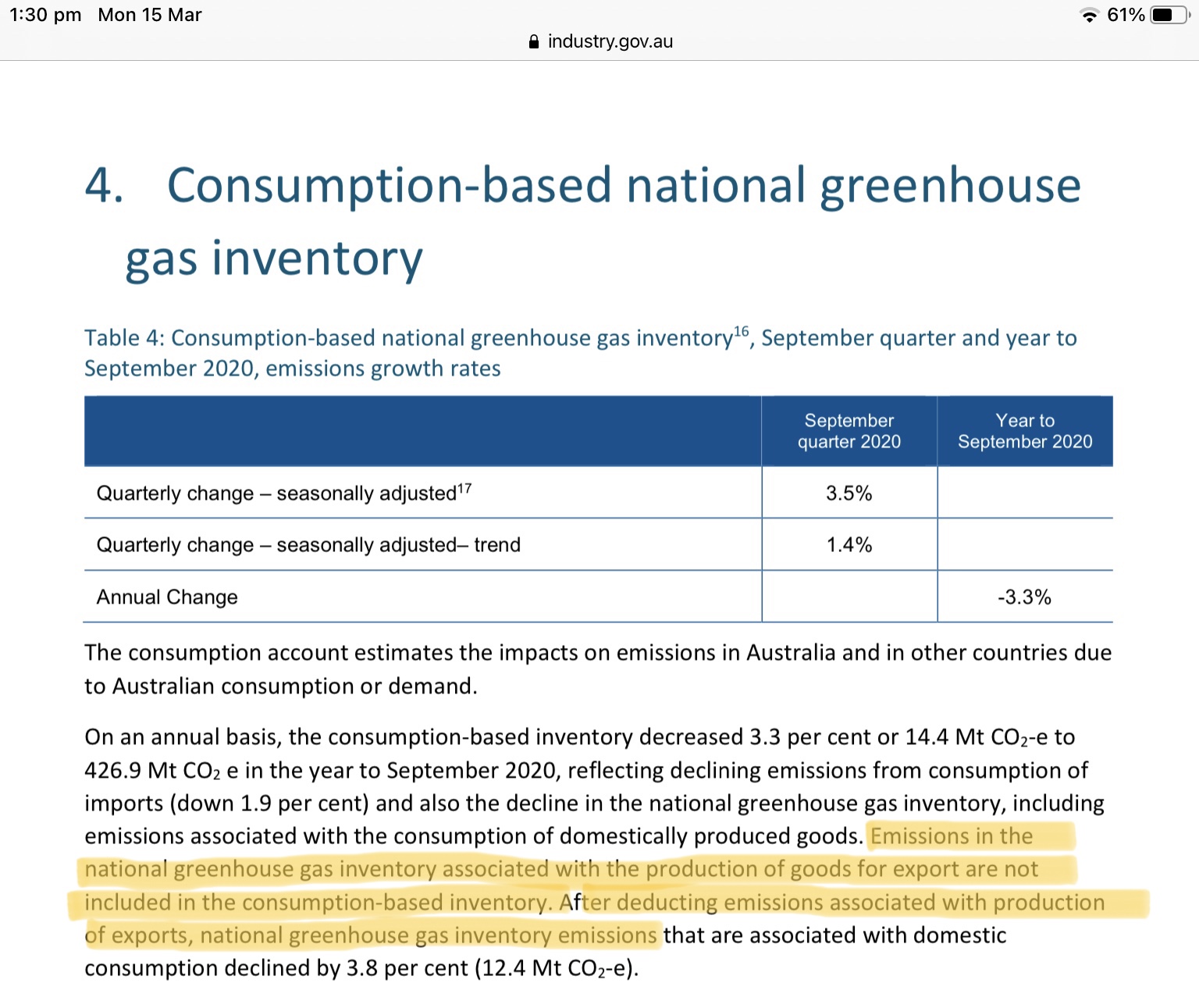

Not likely to be a problem. At risk of distracting to a different topic. There was a change some time back in the how the Government Dept of Industry, Science, Energy and Resources is reporting. It offers a zero cost solution. Consumption-based National GreenHouse gas emissions inventory accounting. It’s all to do with how you do the arithmetic, no science required.

Quarterly Updates of Green House Gas Inventory - refer to section 4.

This Aussie solution transfers the GHG emissions created in producing an exported commodity with the product to the end user.

It’s different to Australia’s International obligations, and the exact opposite of EU proposals to place a carbon tax on imports. It proposes imports will be taxed based on the imbedded carbon created by production at the source. This is intended to provide a fair and level outcome for EU businesses while discouraging off-shoring of GHG emissions. This favours hydrogen production from zero carbon sources. EG electrolysis of water using PV generation.

Japan and the UK are considering similar options on carbon taxing imports, to be discussed later this year as part of the scheduled G7 summit. Australia is not a G7 participant.

1 Like

The Australian Govt considersmany of these GHG emissions to be what are termed Scope 3 emissions and therefore not to be accounted for by us. If we dig the Coal out but Japan burns it the emissions belong to Japan, the fugitive emissions from mining should be on our account as scope 1 or 2 but no one can accurately determine these.

As the coal will be used to make Hydrogen here, the emissions should/will be accounted for here, even if a Japanese backed company is responsible for the Hydrogen plant. The Japan CO2 emissions will drop while ours go up yet again. This is not blaming our Japan friends, this responsibility sits squarely with our Governments.

A bit about Scope 3 emisiions:

Gas is another Carbon source to make H2 from and this report shows some disturbing matters about the closeness of the Federal Govt and the Gas industry. But even the first few paragraphs paint a “dirty” picture:

" The Australian government is refusing to address claims that some of the Liberal Party’s biggest fossil fuel donors have profited from fast-tracked, multibillion-dollar projects.

It comes amid growing scrutiny over the government’s relationship with the gas industry, after claims of stacking the COVID commission with gas contacts before officially unveiling a gas-fuelled plan in September as the centre of the coronavirus recession recovery.

Seven months on, the government has refused to answer how many jobs the gas-led recovery will create and is attempting to conceal documents about fast-tracking fossil fuel projects from the public."

3 Likes

Coal smoke and mirrors?

2 Likes

Should be? Of course they should.

Will they be? Reporting using Consumption based accounting suggests the intentions are to not account for the emissions here.

Getting away with it, might need more than -

1 Like

The debate over hydrogen vehicles continues.

Personally, I would take more notice of Toyota and Hyundai than GM or VW.

And other car companies such as BMW etc.

GM and Volkswagen have decided to focus on battery EVs rather than hydrogen, which is why they and other manufacturers which have focused in batteries systems only (e.g. Telsa) have ‘reject’ hydrogen technology. Their ‘rejection’ supports their business model and the punt they have made.

Manufacturers such as Toyota, Hyundai and BMW have hedged their bets either way by both carrying R&D on both battery and hydrogen fuel systems, and developing cars with both technologies.

It is in their commercial interests to try and discredit hydrogen fuel systems.

2 Likes

Nothing quite like the good old vested interest.

2 Likes

It takes a lot of money to bring vehicles through idea, to development, to production and market.

Batteries and electric vehicles are here now. In production, and the issues understood.

Hydrogen in vehicles is as yet just research and testing.

Some producers have decided to make a decision and go with the demonstrated technology. Others have decided to continue research.

I see no vested interests in this or discrediting. It just how they see the technology now and to produce vehicles to bring to market.

1 Like

Neither do I. Assume for the point of discussion they have made a rational business decision to go battery because; the tech is here now, the backbone of distribution (the power network) is here now and the embryo of the supply network is here. That is reasonable and only time will tell if it is right. How do you distinguish between saying battery is better because you really think battery is better from any other motive? What do they say and what way do they say it that shows their motive is to discredit the other view? I don’t think you can tell.

Secondly, at this stage battery has a big head start and hydrogen is not an immediate threat. If one thinks hydrogen might be a threat in future the best idea is to: support better battery development, push out e-cars now to encourage charging station building and also lobby for assistance with station building to service the new fleet. If you succeed in that over the next few years you go a long way to shutting out hydrogen. The domestic car is a network good, getting hold of the market first beats technical merit. Think beta versus VHS or reciprocating versus rotary ICEs.

Thirdly, the main advantage of hydrogen over battery for the consumer (range) will not be here forever. The early ICE car was a turkey that was expensive, unreliable and inefficient when first introduced. Development cured those problems. Both systems have technical problems now and need development to become mature products. I am betting battery get there first.

1 Like

Not quite, hydrogen vehicles are commercially available and Toyota and Hyundai have readily available models. Toyota has had a production model available for over a decade. Other manufacturers Audi, and Mercedes BenzBMW, Audi, and Mercedes Benz and Honda , and startups such as Riversimple…which has one of the least attractive cars ever designed) are also close to releasing new hydrogen models (BMW is one example where their first H-vehicle will be released in 2022 with more models under design and in the pipeline).

The main current issue with H-vehicles is finding the infrastructure to support the H-vehicles, such as refuelling stations. Currently there are limited refuelling stations available (only a handful in Australia) which makes them a less attractive proposition at this point in time. Even James May has highlighted the infrastructure problems which exist in the UK for the Mirai he owned).

E-vehicles however can be recharged, albeit slowly, using existing domestic electricity infrastructure, but like H-vehicles, finding the quicker fast charge stations outside urban areas which support the particular manufacturer’s plug is also challenging.

One shouldn’t confuse lack of infrastructure for H-vehicles as H-Vehicles not being ready for the domestic market and just research and testing.

There is a significant vested interest. Volkswagen, GM, Telsa etc have gambled their long term business success on going down one path, that being battery system technologies. A few years ago, these car manufactures (except Telsa) had significant R&D into hydrogen and they decided in their business plans to focus on battery systems at the expense of hydrogen (they dropped their H programs). Their future success as ICE vehicles are phased out, is battery systems. They are relying on their future success to be that battery systems will replace ICE. They have a significant interest in discrediting H-vehicles as H-vehicles aren’t within their future business plans.

1 Like