ZipPay boasts ‘100% no interest’. But can you trust it?

Find out more:

ZipPay boasts ‘100% no interest’. But can you trust it?

Find out more:

Interesting that they are likely to make a loss against income from fees vs defaults and that the defaults are likely to rise. I am assuming that the fees are only the customer fees and not the fees they collect from businesses who support their payment method.

I checked out their sister company ZipMoney and went through the signup process right up until they wanted my online banking login details. The banks constantly tell us to keep this information secret yet it seems to be required to set up an account with ZipMoney. If they ever get hacked their user data would be a goldmine for the hacker.

Quite a few financial institutions are providing a ‘service’ whereby we can see all of our accounts on their single web site. All we have to do is provide our account and login details. Surely they can be trusted for both security and not filtering the data for marketing purposes. Surely they can. (/sarcasm font)

I know they are in bed with NAB and Westpac but I wonder in general where that puts the customer when they hand over access …

Up that famous creek with a sieve for a paddle in a barbed wire canoe!

Applied for ZipPay for a large purchase. It was a waste of my time. The app is not user friendly and wouldn’t send me a verification code for hours. That is not the main reason for my topic. The product is disguised as interest free but there is a $6 fee if you don’t pay your purchase off after your first statement. So if I were making 4 fortnightly payments for a purchase, I would get charged $12. In effect that $6 is more than what I would pay on my low interest credit card. Am I correct or have I read the T&C’s wrong?

You are correct, this is a real catch with ZipPay. If you were to miss all of your repayments on a $100 purchase, you would have to spend an extra $33 on fees. You also need to watch for direct debit fees from your bank, take care the additional charges don’t leave your bank account overdrawn.

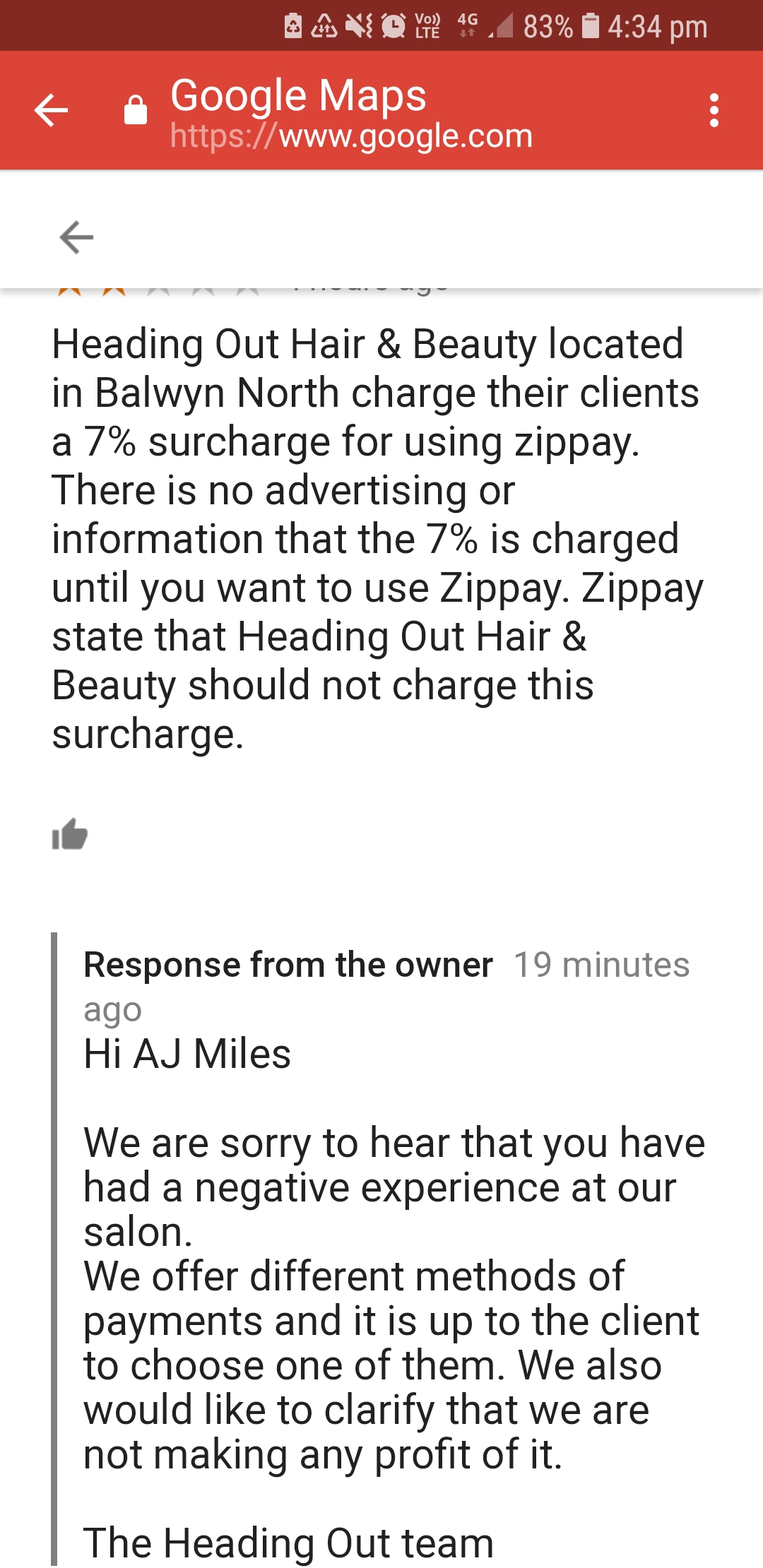

Heading Out Hair & Beauty located in Balwyn North charge their clients a 7% surcharge for using zippay.

There is no advertising or information that the 7% is charged until you want to use Zippay. And zippay state that Heading Out Hair & Beauty should not charge this surcharge.

Customers need to be aware of these 7% charges.

Furthermore, you have to ask for the receipt for the sneaky unethical charge to be disclosed. If you use zippay they do not provide a receipt.

This is overcharging and something the ACCC has targeted in the past. The fees Zippay charges can be found here:

It appears that the maximum fees Zippay charges merchants if 4%, so assuming the hair dresser is on the maximum rate and not the minimum 2% rate, they should only be charging around 4% surcharge.

Here is a recent news article about excessive fees and charges…

and this is what the ACCC says.

I possibly would be approaching the merchant/hairdresser advising that you believe the 7% surcharge for using Zippay is excessive and you would like the reimbursement of the additional surcharge paid above and beyond what they are charged by Zippay. If there is no resolution and one strongly feels the charges are excessive, one could also lodge a formal complaint with the ACCC.

Choice has also reviewed Zippay on the past…

@phb stole my thunder whilst I typed, hence my shortened version.

I would get ZipPay’s position in writing/email and use that to approach the business.

The only bit I might add is that it appears some payment systems (ZipPay?) might not be included in the excessive payment regime as the wording is always like

The ban restricts the amount a business can charge customers for using an EFTPOS (debit and prepaid), MasterCard (credit, debit and prepaid), Visa (credit, debit and prepaid) and American Express cards issued by Australian banks.

ZipPay is apparently not a credit card equivalent, but is a layby system, so they (and AfterPay) may have found a loophole – they are not credit, debit, or prepaid cards.

This is an interesting new avenue for our exploration. Please let us know what you do and how you go with it.

It appears that Zippay falls under the Financial Services Ombudsman.…so this may be another complaint avenue to explore.

If one believes that a retailer/service provider intentionally overcharged, one has the choice not to use their services again, no matter how good they are.

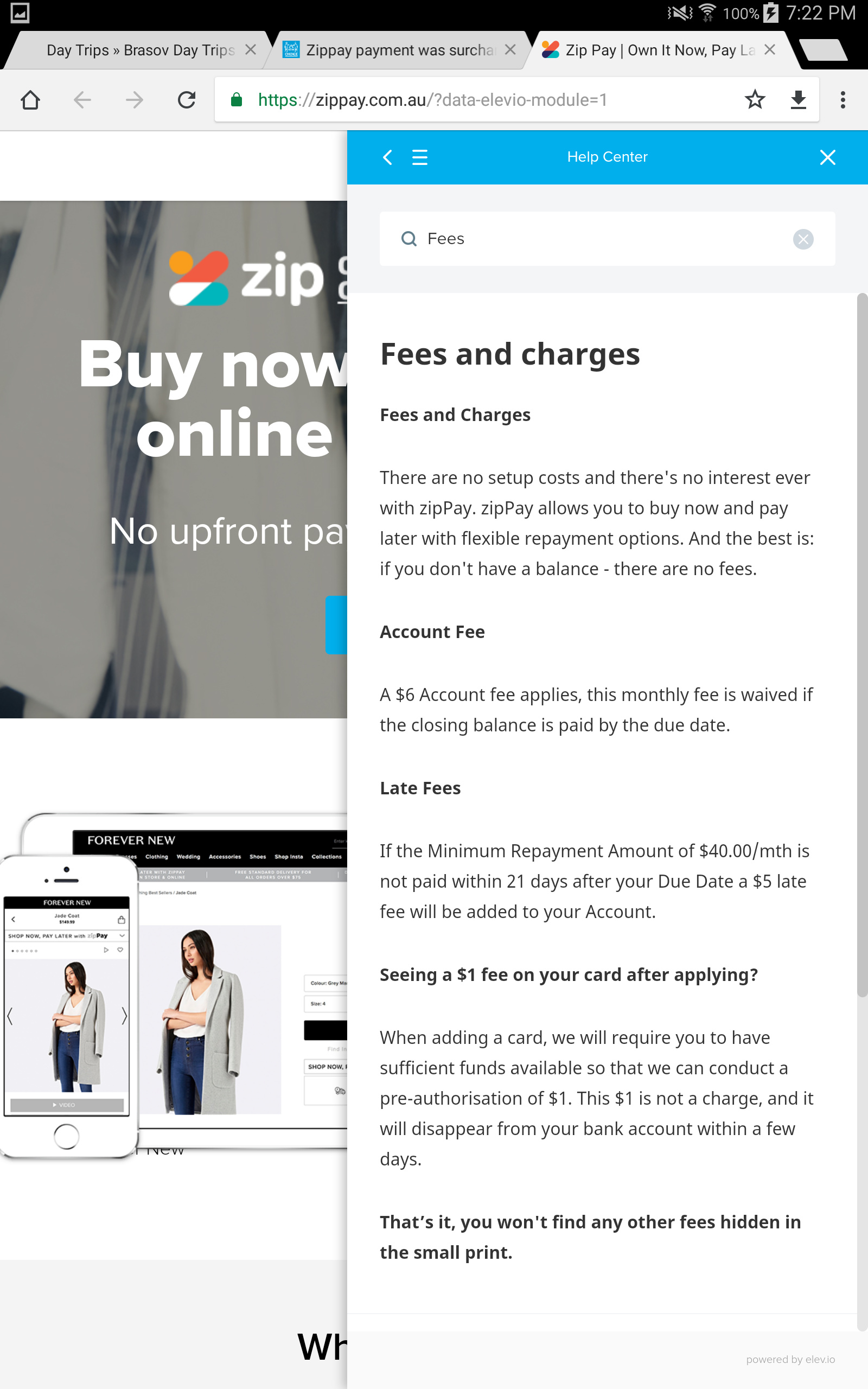

This is also what Zippay says about customer fees on their website…

It is interesting to note…That’s it, you won’t find any other fees hidden in the small print

It appears that there are in fact hidden fees which can be charged by merchants. The website could be misleading or terms of use should be amended to include a statement with something like ‘merchants may charge additional fees for using Zippay. Merchants should be contacted before commissioning of services to determine what additional fees may be applicable.’

Based on this, you could also be within your rights to request reimbursement of the whole of the 7% surcharge imposed either from the merchant and/or Zippay.

The website states in relation to merchant costs…

There is no indication that Zippay expects merchants to pass on merchant fees. This is unlike say the Commonwealth Banks Mastercard where the conditions of use state ‘Third parties may impose a fee for use of a card.’

In any event, these fees are unacceptable and unreasonable especially when the Zippay website is silent on these ‘hidden’ fees and the merchant didn’t openly disclose the fees at the time of the transaction (if in fact this is the case).

Thanks for the report @AJMiles. We’ll keep this in mind the next time we address excessive surcharging

You could probably also point out to the merchant that ZipPay likely (I know AfterPay does) expressly disallow a vendor to surcharge to customer anything for choosing this payment method.

yes much better for the company to charge 70 people $1.00 extra so the one person buying the fridge with Zippay doesn’t have to pay extra for using the service

While your solution would work, it doesn’t resolve the Zippay merchant fees which are imposed on the retailer and then which the retailer chooses to impose in its customer(s). It would be better for the merchant fees to be addressed, so that the impacts on the end consumer(s) are minimised.

I can’t imagine that Zippay costs for processing the purchase are around 2-4% (or the retailer’s costs being 7%) when the rest of the credit industry are <2%.

I agree they don’t have a high processing cost and it would be something similar to the rest of the industry. But Zippay do not charge interest on the debt/transaction. It is a single % based fee imposed and they choose to put that impost on the merchant rather than the consumer. If the consumer then defaults on a payment they are then required to pay a fee for that late or missing payment which is not imposed on the merchant.

For the merchant there are benefits ie they get an immediate sale with full reimbursement less the fee, they can sell to customers who might otherwise not buy the goods due to lack of money at the time, if they would have sold on account there are the administration costs avoided by getting “instant payment” and no recovery fees in the event of a failure to pay, if normally a layby then a similar administration cost is saved, possible failure to complete the layby and a saving on storage cost and space. For this convenience they pay a fee more than the admin/processing fee imposed by some others, but we must also remember this is the merchant’s choice to offer the “Zippay” selection not one being offered by the purchaser. The merchant who agrees to the T&Cs of Zippay to use their service and then wants to alter the way they then use the product outside the contract would be and indeed is in a clear breach of those conditions.