The law and rules that sets out how much electricity and gas networks can charge for their “poles and wires” services says the objective is to meet the long-term interest of consumers.

Questions

Do you think the regulator is meeting the long-term interests of consumers in the way it works?

What do you think the long-term interests of consumers are in relation to electricity and gas “poles and wires” network services?

How would you know if the regulator is doing a good job?

This is the second run you have had at this. I note that you said nothing the last time, perhaps you would get better replies if you said what you are trying to achieve and explained your perspective.

The AER’s Consumer Reference Group is undertaking a consumer consultation process for its inflation review and development of the 2022 rate of return instrument. We are happy to facilitate this and give people the opportunity to have an impact on this process.

I followed the CRG link and opened the ‘member biographies’ PDF.

The one member of the CGR that appears to be most relevant to the average residential consumer is Energy Consumers Australia. A useful link and access to some of their activities:

It’s also worth noting that the CRG is only an advisory group. The scope of the current review is limited as indicated. One current member of the CRG, Mr Allan Asher was previously an Executive with the ACA (Choice).

It may be of interest to others in the community the extent of the organisational network associated with gas and electricity supply. There are aspirations of community consultation. I’m enlightened, but wonder why there is not broader community knowledge and involvement. I’ve left ‘my mark’ on the current Energy Consumers Australia survey, (Excuse the pun). Following that I hope to be able to respond to the OP in a meaningful way, considering:

That the electrical “poles and wire” service for at least the last decade possibly/arguably 2 decades should have been focused more largely on the “at the time” emerging and now burgeoning Small Scale Production and the impact that has had on supply and distribution issues. Why has it taken so long for responses that at least look like they are trying to change eg Victoria’s localised Battery trials. Even if a house or apartment can’t have PV panels or some other renewable energy generation if micro-grids were installed in the local community they could all benefit from more localised power storage and only need to draw from the wider grid when storage was unable to fully cope with demand. This storage also allows the wider grid to draw from the local storage at times when other areas have a lack and the local one has surplus. Anyone in the higher echelons thinking about Virtual Power Plants? Honestly the lack of foresight is just abysmal.

Why has it taken so long to move from Coal and Gas fired energy production to more carbon neutral tech. Why aren’t more efforts spent on renewables than subsidies to coal and Gas mining enterprises.

A huge failure of regulation and regulators to address the issues.

A 2 Addressing the failures, to put my answer mildly enough not to be offensive to anyone reading this.

A 3 Because the system would be addressing these issues right now rather than trialling answers that many of our similar World partners have already accepted. It seems ludicrous that overseas experience counts for almost nought here.

Each individual will have different expectations and interests. An example is those who can afford to install a large PV system expects to be able to export excess generation to the grid to assist with their return on investment. These system owners also believe that the network should be designed to allow potentially unlimited local export to the grid and that the excess electricity can be used by consumers elsewhere. As the existing grid is designed for unidirectional flows (from large generators in remote areas - to the users), the current network configuration doesn’t support bidirectional (‘unlimited’ PV system export) arrangements. In such respects, those with PV systems possibly don’t think the regulator is supporting the long term interests of (PV system owners who are also) consumers.

If one doesn’t own a PV system (not sufficient roof area, can’t afford it, rents etc), then they argue that their interests haven’t been looked after either…as they have had to pay for the generous subsidies/Feed-In-Tariffs (FITs) to early adaptors of PV systems through higher electricity costs (levies placed on all electricity consumption). They possibly would argue that they not only have been disadvantaged by not owning a PV system to reduce their own electricity costs, but they have had to pay more to allow for PV system owners to benefit from their exports.

One of the challenges the AER has in relation to meeting the long-term interests of consumers is the duration of the Resets - where projects/works within the Resets needs to be justified. Longer term strategic type projects which may be in the interest of the consumer are more difficult to get mileage as their can’t often be justified until the project becomes ‘urgent’. At such time the least Net Present Value (NPV) solutions are pursued which may constrain long term projects which benefit all electricity users.

Possibly the AER could have an over arching strategic plan with different network scenarios to assist in achieving some long term (7-10+ years) and to guide generators/network operators in what is in the long-term interests of consumers. Such is currently lacking from a consumer perspective.

This raises the question for a consumer based strategic plan, what are the guiding principles? Are they cost? Reliability? Renewables? etc etc.

I am at a loss to see he connection between the two new threads in this forum and the linked description of the AER Consumer Reference Group. The latter is all about finance and nothing about operations, prices or policy.

Objective

The AER is reviewing the treatment of inflation in our regulatory framework, including the method likely to result in the best estimates of expected inflation. …

The Rate of Return Instrument sets out the approach by which we will estimate the rate of return, and comprises the return on debt and the return on equity, as well as the value of imputation credits. …

Role

The CRG will help the AER implement an effective consumer consultation process during the 2020 inflation review and development of the 2022 rate of return instrument. …

@BrendanMays perhaps you can resolve this noticeable discrepancy.

No, I don’t think that consumers’ interests are being met.

Consumers’ interests are being looked at too narrowly; in financial terms. AER appears not to have embraced the fact that consumers also care about the environment and sustainability. I suspect that these interests will gain more and more momentum in the future. PV uptake is not only for financial benefit, it is also to reduce our country’s need to use fossil fuel generators. People also want as much self sufficiency as possible. The uptake of solar PV can be juxtaposed to the uptake of water tanks. Twenty years ago local councils made owning a water tank in suburbia prohibitively difficult. Now they are pervasive. People don’t want to be charged for putting the excess power generated any more than they would want to pay for excess water from their water tanks overflowing into the storm water drains. AER should be looking at the future, and representing the more than the maintenance of the status quo which, from an outsider consumer’s point of view, is what seems to be occuring.

If the grid & networks respond to current and future trends led by consumers. I am not talking about ‘gold plating’. We have been there and done that, and it didn’t help consumers. It only added to the providers’ bottom line. What I am talking about is better and more efficient bi-directional delivery. Generation should be from decentralised sustainable renewable energy plants. When all that happens I will know that AER is doing it’s job.

protect vulnerable consumers, while enabling consumers to participate in energy markets

deliver efficient regulation of monopoly infrastructure while incentivising networks to become platforms for energy services

effectively regulate competitive markets primarily through monitoring and reporting, and enforcement and compliance

use our expertise to inform debate about Australia’s energy future and support the energy transition.

My reading of the plan is IT IS NOT within the Authority of the AER to change the design of Australia’s Energy supply networks for gas and electricity. What the AER can influence is set out by Government and legislation. It’s worth noting that in addition to the enterprises involved with the gas and electricity industries, as part of the NEM (National Energy Market):

The Energy Ministers are the key decision maker with policy and governance responsibility.

The AEMC (Australian Energy Market Commission) develops the rules by which the market must operate.

The AEMO (Australian Energy Market Operator) responsible as system operator to maintain system security and reliability in accordance with the standards defined in the National Electricity Law, National Electricity Rules and by the Australian Energy Market Commission’s Reliability Panel

and others ……

The industry is a bit like a “Frankenstein” with Private Enterprise as well as State owned entities. There are more vested interests in the industry than there are connections represented at the running of the Melbourne Cup.

Q1/ The regulator is not meeting the long-term interests of consumers. The need to transition to low carbon energy was recognised and agreed to by Australia as of Dec 1997 in Kyoto.

Irrespective of political ambitions, the role of the AER is supposed to put the needs of consumers first. The majority of Australian consumers have consistently supported the objectives (public surveys) of the first agreement to reduce carbon emissions and all those following. It’s apparent from where the gas and electricity supply industries are now, with a lack of vision and future investment, that there has been a mis-step. As the consumer champion the AER should have either halted years prior the uptake of rooftop residential solar PV, because the industry and grid was not up to the task, or called out the industry to ensure it was ready in advance.

Q2/ The long-term interests of consumers in respect of gas and electricity network services depend on which future best meets the needs of consumers. In a low carbon future, the traditional models and analogies for energy distribution no longer apply. The AER to it’s credit recognises the need to deliver Consumer outcomes focussed on DER (Distributed Energy Resources).

The principle of centralised generation, distribution, ownership and operation needs to provide for decentralised ownership and operation of micro grids. The AER needs to advocate for independent ownership and operation. This is necessary to provide for expanded opportunities for local community ownership as well as contracted out operation.

The regulatory model needs to promote competitive practices to transport energy around the major inter connecting network, independent of the local networks. Communities and consumers need outcomes that are more transparent in how energy is costed. Regulation needs to support local energy sharing/exchange without the overheads of the NEG and limited competition for supply.

The option should be available for large energy consumers, including shopping centres, large scale residential properties, businesses to take supply from any of a large number of competitive sources, and to export. The best financial model for the high capacity interconnecting network needs to be determined. In the interest of individual consumers who directly draw from or export energy to their local micro grids the model should be zero cost.

The AER should ensure that the option of a no network future for residential consumers (IE off-grid residences or communities) is available as an alternative competitive option, and is not blocked by vested interests or poor decisions that are not in the best interests of those consumers.

Q3/ The Regulator will be doing a good job if it is ahead of the transitions commercially and technically. The Regulator should be able at any time to explain the impacts of different pathways and possible decisions to consumers, in advance of all transitions or industry commitments. These should be clearly communicable in respect of meeting environmental outcomes (near and future), cost, quantity and timeliness of supply. The AER should be able to demonstrate consumers are able to choose or prioritise needs from multiple options for supply, and not just supplier in a competitive environment.

Sorry if you felt there was insufficient guidance in the last set of questions.

In a fuller form, the law requires the AER to come to a regulatory decision on the gas and electricity networks (poles and wires, not retailers) that::

network regulation needs to achieve the long term interests of consumers,

gives incentives for the efficient use of the networks,

considers the costs of both over and under utilisation of the networks and allows them to recover

their investment costs

I would like to hear your thoughts on these things to inform what the CRG says to the regulator

The CRG is advising the regulator about setting the allowable revenue (how much they can charge) of networks for their poles and wires services.

Much of this is about rates of return on debt and equity using complicated formulae, however it is also about consumers expressing their views on prices, quality safety and efficiency. The rules also call for a system that meets the long term interests of consumers

All of these things are open for comment

Can we see the complicated formulae, the debt and equity involved?

How does this relate to the cost to the consumer of electricity?

What portion of the network costs is met by consumers, and what portion of total energy carried over the networks is used by consumers?

How are the network costs of locally produced and consumed energy (Distributed resources) considered? Are they assessed independently from those of centrally generated resources, and if so how?

What is the future forecast demand or loadings across the network by segment, state and zone/region?

What are the current forecast future expenditure requirements (costs) for:

Maintenance of each zone/level across the transmission network,

Maintenance of local distribution,

Capital investment in the transmission network,

Capital investment/upgrades of the local distribution network?

How does profitability, relate to future investment and return on investment?

How much idle or spare capacity is there across the distribution networks?

The list of items suggested for comment appears to be missing reliability, if that is also a desirable outcome for the networks.

Constructively the dilemma for the AER and indeed the ACCC is that if consumer use of network sourced energy decreases, there is less consumption from which to recover network costs.

I cannot contribute as I have no understanding of the relationship between rates of return on debt and matters such as prices to consumer, quality or safety. I wonder if any members of this forum do. If anybody does I would welcome an explanation.

Is there anything on the AER website that might tell me what kind consumer feedback is desired regarding matters consumers are directly involved in such as reliability, price etc?

This all seems so vague. Perhaps that the intention. Is it opened-ended and not tied to the specific role and powers of the AER (which I doubt many understand either) to get a wide range of replies regardless of relevance? If so why?

Thirdly, what will become of the responses that you get? Is there anywhere we can see what has happened to such responses from previous reviews?

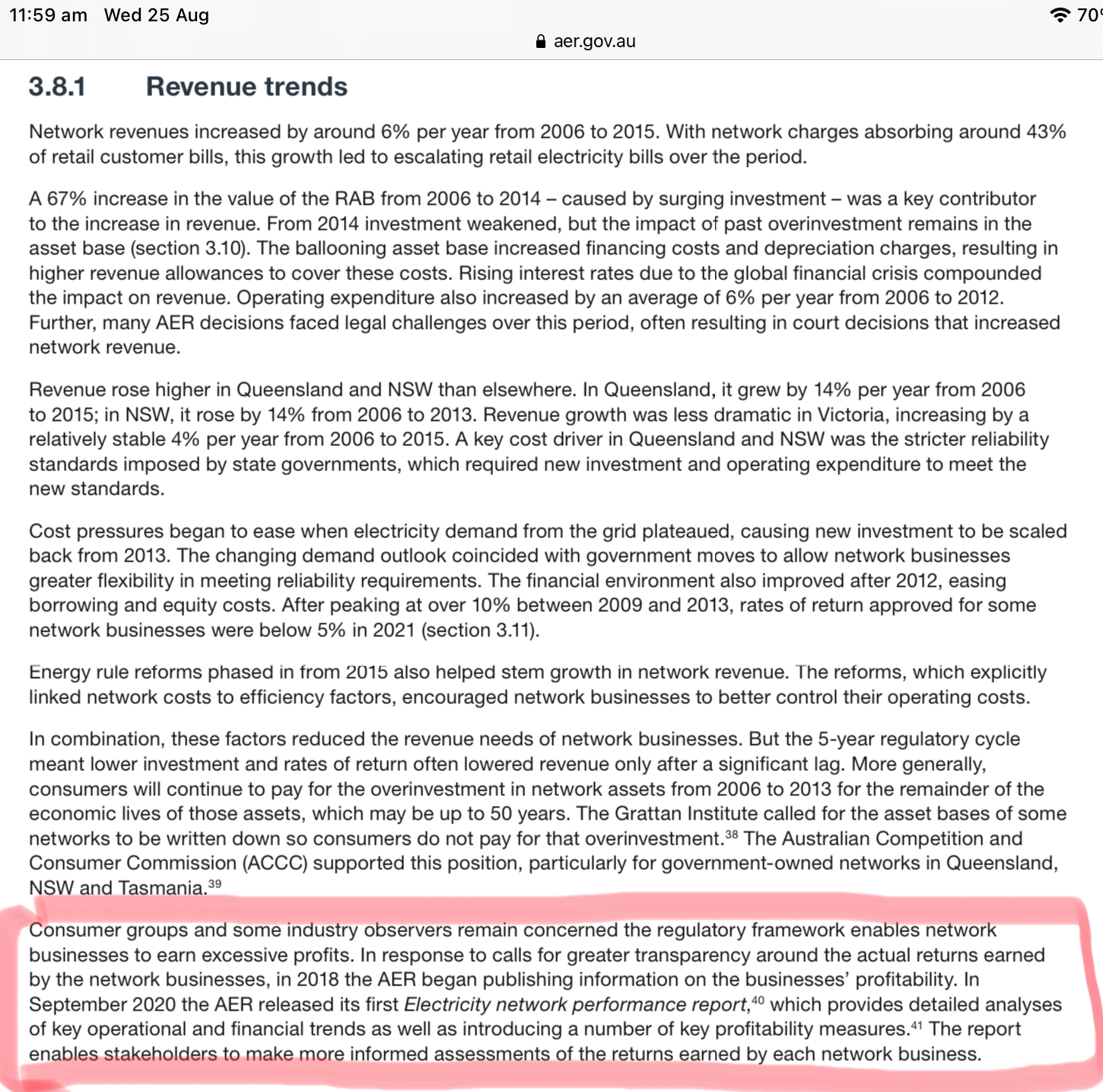

I found the following to be a more complete explanation of the decision processes in respect of the networks by the AER. It includes in detail the relative values of the assets and their utilisation vs customer base as the starting point. It’s a PDF in plain language with lots of consumer level illistrations.

I’ve copied one key page that I found useful. In particular the last highlighted paragraph. It suggests there is more content very relevant to understanding the current profitability of the ‘poles and wires’ business.

Hi syncretic, I am a Member of the CRG and as I am new to this forum, am interested in your comments. The CRG is currently focussed on the AER’s decisions around the energy networks “Rate of Return”. The Rate of Return has a large impact on energy prices and this is one of the reasons why this issue may be of interest to consumers like yourself. While the CRG is not the decision-maker (the AER is) we are an advisor to the AER as provided under the energy laws. The “long-term interests of consumers” is one of the key things the AER has to take in to account when making its decisions. That is why we are interested in hearing your views about what these long-term interests are. Who better to ask than consumers themselves! This is a different issue to our first post, which was focussed on energy prices and an understanding of what the AER does. Wishing you all the best, and thanks again for posting.

So let me see if I understand. The level of profit of electricity networks is determined by this rate of return and from time to time it is renegotiated. However you want the consumer perspective on this renegotiation. I doubt too many people understand this relationship exists much less how it works.

We have been given some examples of other interests that consumers may have apart from price. Some of these clearly do relate to the network directly, such as stability under varying load and generation patterns, but others like greenhouse gas consequences are more related to generation. +++

But what can I say in respect of the desired network structure and function if I don’t understand the trade-offs between price and reliability or stability?

Not understanding the factors that go into this renegotiation and what the consequences may be for any given outcome (other than some impact on prices up or down) why would you expect consumers to say anything other than we want prices to be as low as possible while stability and reliability are as high as possible?

One of the other factors that make this situation less like most consumer issues is that consumers usually show what they want the market to do by voting with their purchases. We are all familiar with trade-offs such as quality versus price when it comes to the appliance store or supermarket. As this exercise is divorced from retailing (which is the most pitiful imitation of a competitive market) and retailers have no control of quality aspects like reliability, there is no way for us to vote directly.

So I don’t know how I can assist other than stating the bleeding obvious: that I am in favour of both low prices and high reliability, also both motherhood and apple pie. Maybe some of the smarter members can do what I cannot.

+++ If the network cannot deal with the characteristics of renewable generation, large scale or distributed, that of course limits any approach to GHG reduction of energy generation, so the two are related to some degree.

Hi again syncretic, I agree with you that the Rate of Return is a complex subject. The sorts of issues for consumer feedback include how sensitive consumers are to price (if the rate of return is set at a higher rate to last time, this can mean higher prices), whether consumers feel confident in the AER, what values consumers place on price stability (i.e. that prices don’t move up and down alot over the years),whether consumers feel energy networks tend to be self-interested, etc. These are the types of topics we hope to explore in this forum. TheAER website is not easy to navigate but you can try startin with the fact sheets here https://www.aer.gov.au/about-us/stakeholder-engagement/consumer-reference-group/statements-and-advice

The CRG intend to use the feedback we receive to inform our advice to the AER. The AER has told us that they are keen to hear consumer feedback.

That is a question? There may be some here who think that large utilities spent billions buying networks to allow them to better serve the public and that the leaders get their joy not from executive bonuses but the warm feeling of public service. I tend to think not.