And the legal costs and any fines will be paid by CBA’s customers as they jack up their home loan interest rate. The margin since the GFC is now 1.14% higher than it was before the GFC caused by their liar loans. They also are crying about the sudden increase in borrowing money what they didn’t tell you is that since 2008 they have been borrowing money at 0% and charging Australians like they borrow from the domestic market. Bankers are Sick to the Bone.

3 Likes

Another wet tram ticket penalty.

Perhaps the decimal place could be moved a little to the right.

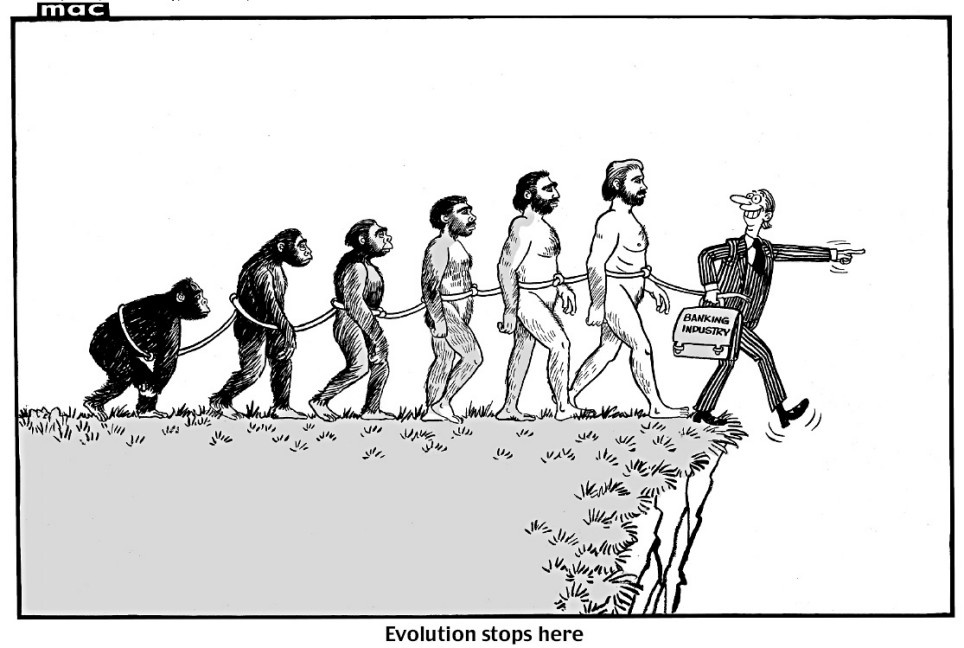

Whoever said that crime does not pay?

7 Likes

Wouldn’t it be lovely to run business like the banks… steal a million dollars, pay back what ever you feel like and all is good… just don’t do it again.

4 Likes

Nothing new. Although the performance of the ACCC is also temporarily under the spot light at present offers some hope.

That the ACCC has the power and authority in such matters to ensure the offences are not subject to the application of law in a court appears to contradict natural justice?

Perhaps the ACCC’s rules need to be changed that the ACCC cannot settler any mater out of court without first satisfying a court of the public interest test. If the court believes it is in the public interest then all the matters need to be put to the legal sword. Secondly if there is to be an out of court settlement the minimum agreed penalty, independent of any agreed restitution should be specified so that the ACCC cannot settle for a lesser amount. 10% of the maximum legal penalty might be reasonable.

In the Westpac settlement noted the minimum settlement with the ACCC would then have been in the billions. It’s unlikely we would accept a fraudster who by deception is talking a million to be set free after paying a fine of a few hundred dollars. And being allowed to retain the proceeds?

4 Likes

The paying a pittance in return happens at times with the Tax Office when a firm goes “bankrupt” and pays a few cents in the dollar towards their tax bill and can then resurrect with plenty of money from “somewhere”. I sort of remember Alan Bond in this regard though my memory may be incorrect.

3 Likes

A little off topic.

Most of us pay our tax as we earn. At the end of the year there is an adjustment. Companies and business only pay their tax retrospectively, on average 18 months behind the income stream.

Companies and business collect tax such as gst and remit it quarterly to the ATO. This is principally a tax on the end user - consumer. It would not be that difficult for the ATO to require a company or business to also make a quarterly tax payment to the ATO prospectively as an instalment against the EOFY Company tax liability. This could be a fixed percentage of turn over. Since turnover - sales are one of the calculations on the gst return it is not hard to do!

Implementation might be the problem?

p.s. Businesses are also supposed to remit payee taxes collected from employees and super to employees funds quarterly as well. The ATO has been slow to enforce these under takings in instances. Perhaps if the ATO is not getting a big fat Quarterly Company tax instalment from a business it might realise that somehthing is amiss and act more promptly?

And given our politicians are also PAYE employees the change will not affect their incomes - so no reason for them to say no!

4 Likes

Small withholders of tax ie withholds $25,000 or less a year pay quarterly to ATO

Medium withholders of tax ie withholds $25,001 to $1 million a year pay monthly to ATO

Large withholders of tax ie an individual or business that withheld amounts totalling more than $1 million in a previous financial year, or is part of a company group that has withheld more than $1 million in a previous financial year pays roughly weekly to ATO. (a week and a day or if a public holiday the next “Business Day” after that period).

3 Likes

A royal commission into banking… now they’re talking about holding a royal commission into the energy industry … … next up, there’ll probably be a royal commission into royal commissions.

3 Likes

Not enough time before the next federal election to kick that one off. Odds on to announce there will be one into power prices if the LNP is re-elected. Will the terms of reference limit the recommendations?

2 Likes

Be interesting to see what unfolds… particularly given the fact that it was a Liberal government here in Victoria back in the early ’ 90s that was, possibly, the first to sell off essential services.

3 Likes

The banks will surely change their ways after this big RC reveal. Surely they will - Not.

3 Likes

(/sarcasm)

Clearly power is not an essential service if they believed they could sell it or integral components of it.

It would seem that only money in the coffers is essential! Lucky they are such good adult money managers.

(/end sarcasm)

5 Likes

The ABC News website today has an article regarding Woollies selling an insurance policy to a disability pensioner, and then refusing to do anything about it until the ABC aired the story.

That’s why I pick Coles and Supa IGA.

3 Likes

The ABC News website today reports on some more examples of the contemptable behaviour of insurers at the Banking Royal Commission.

What a bunch of disgusting, bottom feeding parasites.

6 Likes

Another episode of the disgraceful behaviour of these bottom feeding parasites, courtesy of the ABC News website.

5 Likes

The fact an x-senior manager in APRA is also in the news underscores how lax Australia has been and probably remains, and reflects how our pollies are not worried as long as nothing costs them votes, until it costs them votes when the jawbone and little else begins in earnest. A more recent claim is often “It was all the opposition’s fault” too. Considering the time in government of each party, and what they did and did not do or just blocked, it beggars belief they can maintain their pomposity and feigned care about any of it.

7 Likes

The CBA have issued an email to their customers explaining how they will be improving:

"A better Commonwealth Bank starts now.

Dear xxxxxx,

My name is Matt Comyn, and as the new CEO of the Commonwealth Bank, I would like to update you on changes we are making to build a better bank.

Over the last few months, the banking industry, including the Commonwealth Bank, has been rightly criticised for mistakes we’ve made. You may have seen examples of this in the news.

I’m sorry for the mistakes we’ve made. My job now is to fix them.

In our Annual Report to shareholders last month, I laid out a new purpose for the Bank – to improve the financial wellbeing of our customers and communities. To make this a reality, we’re making major changes to simplify our business, listen more, resolve your concerns faster, and support our people.

We’re already making changes to benefit you, and will make more in the coming months.

Here’s how:

• Focussing on service instead of sales. We’ve changed our employee incentives to reward our tellers for helping you, not for selling products.

• Removing ATM withdrawal fees. We were the first major bank to remove these fees.

• Quickly fixing issues raised by our regulators, including making changes to better combat financial crime.

• Making sure we are only selling products that are right for our customers, and compensating customers where we got it wrong.

• Providing greater transparency on fees and charges. We’re helping you avoid fees, save money and stay in control with smarter alerts and notifications.

• Safeguarding your privacy and security. We’re strengthening how we keep your information private and taking quick and effective steps to better protect you in the event of a data breach.

• Being there for those who need us most. We’ve expanded our support for drought-affected farmers, and we’re assisting customers experiencing domestic violence and older customers to protect themselves from financial abuse. This support is in addition to the help we continue to give to customers facing financial hardship through a range of solutions such as deferring, reducing or freezing home loan repayments.

• Getting back to basics. We’re simplifying our business, including exiting some businesses. That way we can focus our attention on doing a better job for you.

Hearing from you matters. I can be reached at ceo@cba.com.au if you would like to contact me. You can learn more about the changes we’re making at commbank.com.au/betterstartsnow

Building a better Commonwealth Bank will take time and it is my number one priority. I hope you will see, we are working hard every day to earn your trust and for us, better will never stop.

Matt Comyn

Commonwealth Bank CEO"

The email says they made mistakes, this is a mild way of saying how they did unethical and quite possibly criminally illegal things beyond mere mistakes. They are trying to make the faults sound far better than they are. Sorry but this to me is just so much painting over the cracks to cover the rot behind.

4 Likes

File that one in the

6 Likes

Oh that’s priceless

It’s so reminiscent of ALL the other corporate “apology” letters… there must be just one template out there!

“Have you been caught screwing your customers? Well we have the apology letter for you! It worked for Facebook… Designed for social media giants, financial institutes, mining companies, insurance industry, telecommunications… AND it can easily be transformed for Government use! Just one million dollars form corporatebullyboy-dot-com”

3 Likes