@PhilT Here! here! the removal of penalty rates was not about better job options it was about better (read bigger) profits for businesses while keeping workers in a state where they don’t dare refuse the employers in case of job loss.

4 Likes

An old topic but a goodie as businesses have found ways to surcharge instead of raising prices. Even if only a case of 1 it is an over the top arrogance by the business. The solution is for customers to go elsewhere. I doubt enough will but worth following.

3 Likes

Two things that I found strange.

-

It is not possible at any time of the week to pay just the price listed against each item on the menu. Everyone has to pay at least one surcharge on top of the advertised prices.

-

The tax invoice shown in the article states that no GST was paid.

3 Likes

It is very strange… almost similar to online drip pricing. Their menus state…

Credit cards incur a processing fee of 1.0% to 1.5%. Debit card fees are 0.5% to 1.0%. EFTPOS no charge. ‘Tap and Go’ incurs debit/credit card fee. External payment Apps incur additional fees. 10% discretionary service charge applies to all groups of 10+. 10% surcharge applies on Sundays, 15% on public holidays, 5% service fee applies Monday to Saturday.

So, a group of 10+ going on a Sunday could be charged an extra 26.5% from the above information (10% group charge + 10% Sunday charge + 1.5% credit card fee). Ouch to say the least.

It explains why the charges aren’t included in the menu prices as customers could be paying different surcharge based on how they pay, how many are on the premises and what day it is.

It should show 10% GST as it is caught by tax legislation…

This could get them into hot water if the tax invoice is genuine.

4 Likes

Ummmm, cards are either ‘credit cards’ or ‘debit cards’. Even a gift card has to be one side of the accounting equation. So their statement “EFTPOS no charge” applies to what, exactly?? It’s card based, and they’ve just finished stating that ANY card transaction will incur a fee, likewise with their following “Tap and Go” statement.

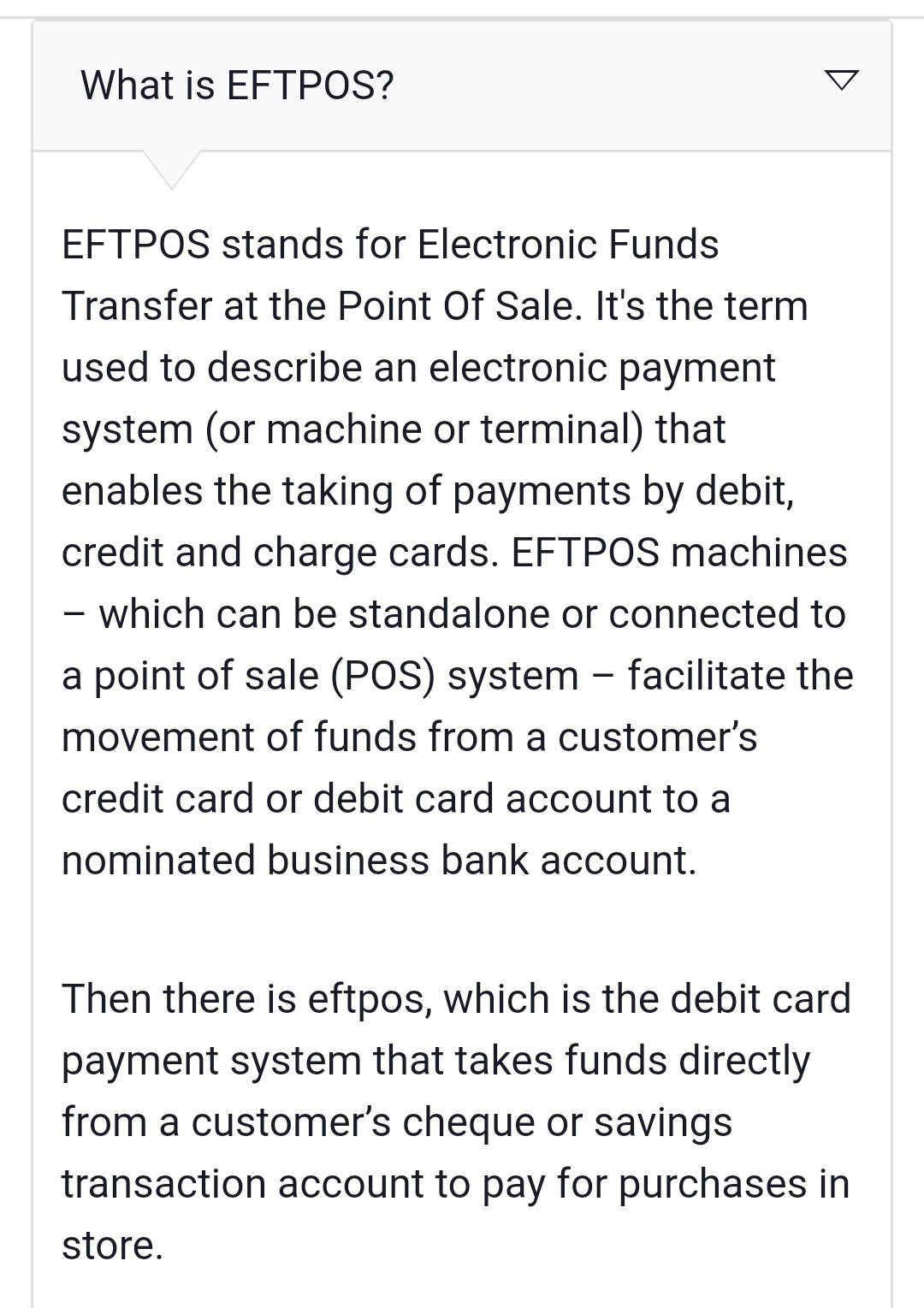

Well, in hindsight, given that EFTPOS stands for Electronic Funds Transfer at Point Of Sale, a person could pay using their phone/app, circumventing a physical card, but is still trapped by the ‘Tap and Go’…

2 Likes

EFTPOS refers to a debit card inserted in the reader with (eg) ‘savings’ selected and a PIN entered. When a debit card is used and ‘credit’ is selected or the card waved (tap and go) it is processed as if it is a credit transaction by the visa/mastercard networks, with credit card fees applied.

There are a number of topics about this on the Community. All gift cards cannot be universally used everywhere and may be specific to a business, each gift card program with its own T&C to read.

2 Likes

But what they’re saying then, is double dutch. They are saying debit cards are charged fees, but EFTPOS has no charge. That’s then an impossible transaction.

They are stating there is a surcharge for debit cards UNLESS they are used in EFTPOS mode. A old related topic…

1 Like

There used to be bank issued eftpos cards…but most banks now have moved to Visa or MasterCard Debit Cards instead. Differences between Eftpos and Debit cards are given here. I haven’t seen a bank issued Eftpos card for many years…they could exist. If they don’t the statement about Eftpos cards is meaningless…unless…Eftpos cards still exist as gift cards.

With all due respect, people, I worked in Customer Service at Westpac for many years, so I understand the difference between debit and credit cards, and the EFTPOS system.

This from Westpac’s website:

Even if a debit card co-branded with Mastercard or Visa is inserted into said EFTPOS machine, and cheque/savings account selected, followed by PIN entered, it is still a DEBIT function being used (customer’s own funds), and this business is saying the transaction will attract a fee.

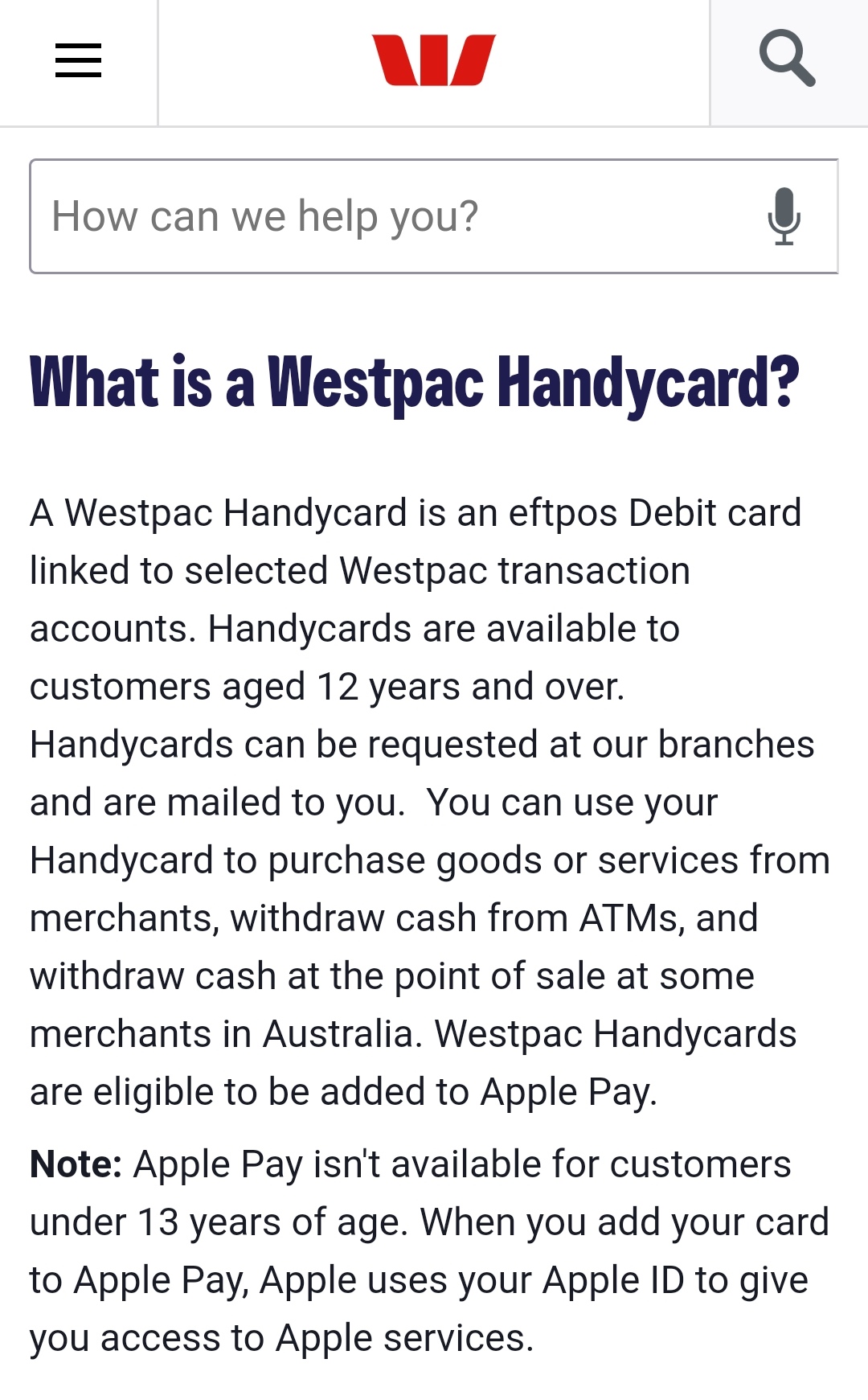

Also from Westpac’s website re Handycard, which can still be requested:

This is a pure debit card with no credit facility/co-branding. If this is what the business means, it is not what they are saying. This is a debit card, and they say they will charge a fee for its use.

In any case, it seems whatever card method you use to pay, you will be charged a fee, and whatever day of the week you choose to grace their establishment, you will be charged for that as well. Is the food really THAT good??

2 Likes

Thanks for researching showing Westpac still issues a bank eftpos debit card… their Handycard.

As Westpac indicates, it is an eftpos debit card issued by the bank. These are the cards I suspect which the restaurant calls eftpos cards.

Their fees in their merchant agreement may be different for Eftpos, Mastercard/Visa debit and credit cards. This may be driving their ‘fees’ for different payment methods.

Edit: should have said eftpos (debit) cards are processed differently to (credit card company issued) debit cards. Not only are transactions processed differently, so are consumer protections.

1 Like

Businesses typically have some arrangement to have EFTPOS terminal(s) with one of the network participants in the Australian eftpos system. Note the difference in case.

The big four banks, and some other organisations, provide switching of the EFTPOS transactions and they are interconnected to send the card transaction to the appropriate bank for processing. The bank will debit your account, and send a credit some time later to the merchant account.

This is the network used when selecting cheque or savings on the terminal. Both are debit mode. Tap and go can also be used up to a limit where the pin is required.

The transaction costs are typically included in the charge to use the eftpos service with the EFTPOS terminal equipment, so the merchant would not incur per transaction charges and could not justify charging a customer for that payment method. However, some business do anyway as a way of recouping the cost of providing card payment facilities rather than cash.

On the other hand, if credit is selected, the transaction is routed through from the Australian eftpos network to the Worldwide networks run by Visa and Mastercard, and they provide credit.

There, merchants are charged per transaction fees, and most merchants these days can and do pass this charge on to the customer.

1 Like

What if the merchant is using Square or another not Visa or Mastercard connected terminal?

1 Like

I would still phrase it as some, not most at least in my area. Is the trend growing, maybe. My view is cards are a cost of doing business and should be bundled into their business models and pricing strategy. The few cash-only shops are also essentially declining some business these days; how that balances out in their P/L only they know.

What rankles me are the number of higher end businesses adding surcharges where a 1 or 2% price rise would be imperceptible. Example - a fine dining restaurant where a meal with wine for two will easily be $200 and more. Who would blink if it was $203 but seeing a $3 surcharge does not sit well. Same with a motel with a $500 per night room + $7.50 surcharge. How many travel with $1,000s in cash or visit an ATM daily? I understand the psychological nature of consumers looking at prices, not surcharges or final costs, and acknowledge everyone is not like myself in this regard.

Many seem to be accepting of a surcharge in the same way Americans feel obligated to tip 15-20% regardless of the service. After being surcharged I assess whether the business was ‘that good’ and if not, avoid it in future.

3 Likes

Our only local butcher commenced adding those card charges separately to the bill approx 12 months after taking the business over. It seems to have been a big thing on that side of the counter. It would as you suggest be simpler to increase the margin and avoid the discussion.

There is currently no surcharge for the cutting and packaging of the product, the electronic weight measurement, the light over the counter, accounting of the sale or …. They remain for now all just overheads and part of doing business.

Perhaps if the product was given away for free the butcher could dispense with all those overheads? ![]()

2 Likes

My guess (it is only that) is that some merchants are sensitive about complaints of rising prices and seek to blame somebody, anybody, but themselves for it. A card surcharge is a way to say ‘they did it not me’. Of course the absurdity is most of their rising costs come from other sources that do not have a surcharge.

It would be interesting if you went to dinner with a group and when the bill came you laid down ten Nellie Melbas for the $967.50 and said keep the change.

1 Like

The merchant gets charged fees for EFTPOS card processing, for SquareUp it depends on the console used (but between 1.6-1.9% on the value of purchase being made):

https://squareup.com/help/au/en/article/6109-fees-and-payments-faqs

Different non-bank issued EFTPOS POS consoles have different fees and charges, depending on the issuing business.

1 Like

Yes, thanks.

I was also interested in seeking to clarify @Gregr post which appears to be saying all payments by credit card are routed through VISA or MasterCard’s systems. Perhaps it was intended as an example?

My reading of Square’s marketing is they are quick to pay merchants. I’ve made credit payments on Square with other than a VISA or Mastercard branded product. I’d expect Square has an arrangement with each of the card providers as to how the charge is passed on to the card holders account. It does not have to be a bank issued card, EG some AMEX, JCB. The merchant fee appears to be the same for all cards that Square accepts.

It would be interesting, although the smaller and more local the business the more likely to see someone pay with cash. Whether it’s to save a few cents or dollars in card surcharges or some other motivation, I’d only be guessing too?

It depends. You can pay a higher merchant charge to have monies deposited into your account immediately.

The standard arrangement is a business can set when their daily close of finances is and Square then transfers the next day thereafter. Deposits are within a business account the next day of the transaction being made if one’s bank supports NPP.

It is with the console one uses - standard rates for in person and manually entered card details.

The merchant fees are slightly greater than that of the banks (expect for Amex), but this is offset by the consoles being owned by the business, whereby, consoles from banks are generally rented month by month. For business with larger turn overs, banks Eftpos consoles make more financial sense than SquareUp.

There are alternatives to SquareUp which are approved for us within Australia such as Tyro, Zeller, Google Pay etc. Each are slightly different in relation to their merchant agreements. Our own investigations indicate that non-bank options are financially better for small businesses or where flexibility of location is required (some of the non-bank options work when there is a mobile/data connection with the console).

Edit: I suspect that there may be a relationship between the banks and the Eftpos processing system in relation to transactions and associated fees. This arrangement may be different to non-banking POS payment offerings.

1 Like