My husband and I are in a very blessed situation. We own our own home about 8km from the CBD of Melbourne, between us we have around $950k in super, one of his super funds is a defined benefit fund, I’m earning roughly $1100 per week after tax through an income protection insurance policy that will continue to pay me until I’m 67 (indexed annually) and he earns around $120k per annum. We’re both 49 years old.

I’ve been retirement planning since I was 27 years old with regular appointments with a financial planner since that age. And I honestly think that’s the key. Key 1 is to start planning young and key 2 is to use a planner with retirement planning expertise.

Whilst I’m no longer working due to health problems (I tell people that I’m retired), hubby is planning on retiring at 55. While so many of our friends have never been to a financial planner in their 40’s and they’re refinancing their homes to buy bigger and newer cars, we bought our last car because it was being offered at 0% finance. I’d much rather be driving a BMW, but my Toyota Camry gets me from A to B and I have a super fund with $70k in it destined to be fully withdrawn and spent on a nice car post 55 years of age which hopefully will be closer to $100k by then.

So the golden rule is plan, plan, plan and get the balance right between living for today while sensibly planning for tomorrow. There is most definitely no one size fits all, so you must plan for you based on your financial capacity and your retirement goals.

Sorry for over sharing but I hope my stories show how planning is key.

Is the challenge with having a plan having control of daily life?

The past 50 years have been far from secure or stable in respect of employment.

Should working hard and sacrificing for 40+ years to have a comfortable retirement be the only goal in life?

Does retirement provide the same outcomes for everyone regardless of life’s circumstance?

Some of the savings we’ve accrued along the way have gone to raising a family, and taking the time to holiday and travel a little to broaden our children’s experiences. A good portion has gone towards education. What’s been retained for retirement is judged against the notion that you can’t take it with you.

As we age we become less able. Higher wealth in retirement may assure one of a gold plated wheel chair, or gold class at the front of the bus. Not all of us get there with or without sufficient funds. There are many on the aged pension alone who say they are OK. Contrasting opportunities for those on a pension vs those self funded the outcomes are not equal. Is another way to ask the topic question,

‘What should aged Australian’s be entitled to enjoy in retirement?’

Looking to our extended family the current Aged Pension is not sufficient. Those making do are too proud to say otherwise. They have depended on the assistance of the closest family to do more than simply exist. What ever the amount required to properly meet the needs of retirement it is a factor greater than the aged pension.

Assuming the family home is in neither St Kilda nor Point Piper perhaps $1000-$1500 per week tax free ($50k -$75k pa) for a couple would be the minimum required.

We found Financial Advisers to be variable, and important to choose well. I had a degree in business, did tax work, had an interest in finance. My husband knew nothing, his first wife did all the bills and when she died he was lost. He went to AMP who charged him $7k and put him in an inappropriate product which lost heavily.

At the other end of the spectrum was the Financial Adviser from his Industry Super Fund. We met him in a regional town on his regular rounds (free), and later I requested a session at our home (cost $1,630) and did retirement planning. He had a lot of experience and the advice he gave was unbiased. He rolled all my husband’s small super funds into one, but in my case he recommended I stay with my Super because I was on a better deal. He had experience dealing with old blokes who insisted they were entitled to the Aged Pension and convinced him to use his super Pension (income stream), something I could never convince him to do. He needed to hear it from someone else.

He also explained that while we could live off the growth in our fund, we needed to consider the cost of going into Aged Care - $300 k. He advised us to avoid retirement villages due to the difficulty of getting out (often you can only sell through management), but that wasn’t our style. He went through sale of assets, work test & topping up super, downsizing, donating, Wills, pensions, and he produced graphs and projections for each scenario some of which got him a part pension - he liked that.

We meet him on his rounds (free) to review the plan, particularly as we are crossing some age related thresholds which can change.

He quoted me “1point 63” for a home visit and hours of advice. My husband thought it was $1.63 and said “that’s good, let’s do it.” Even at $1,630 it was excellent value!

There is a minimum amount that one needs to survive and every dollar above that is a tradeoff for lifestyle. What that minimum amount is depends to some degree on where you live but I have a friend who claims that it is very close to zero. She proved the point by sleeping in her car for a year and volunteering at a soup kitchen where she was encouraged to eat with the clients. I believe that the key to retirement is to have options and if you can identify attractive options that are relatively inexpensive then the amount you need for retirement is far less than financial planners will suggest. At the higher end of options you can buy a cottage in Europe for under $80,000 and you will be able to buy fabulous fresh food at a local market for well under the cost in Australia. At the bottom end you can buy a thumb drive called Classic Books for about $17 that contains 3,000 books. Add $1,000 for a good reading chair and $500 for an e-reader and you have probably got at least three years of entertainment.

You need to work out how you expect your retirement to look and some of that you can really only figure out the closer to retirement you get. I am fortunate. I retired 9 years ago and am on a defined benefit though having worked part time while raising my children, it is not as big as it would otherwise have been. I was youngish so still did a bit of casual work but stopped completely a few years ago. Nevertheless it is indexed and is quite a livable amount if not at all extravagant. My husband is yet to retire and earns very good money. In many ways, we expect to live quite “comfortably” and have planned accordingly. We would like to live entirely on my defined benefit super and keep his for everything else as needed.

The things that we now have to consider is how much we would like to see and help our children. 3 of them live in the northern hemisphere and on different continents. So, do we hope to visit them annually? Do we rely on them visiting us? How many of them will stay overseas permanently? At least one. Then, helping them to buy a house or repay HECS debts? These are personal choices that are not for everybody. They may very well affect when to retire and whether one wants to continue to do some form of work after retirement.

I know others who retired well off but are discovering that huge dental bills totalling $30,000 are a bit of a shock as is maintenance work on an older house as both start to fall apart! Some people expect to be able to live like they did when they worked and get a new kitchen when the time comes whereas many of us would only imagine replacing worn out appliances as needed. How long do you expect to live? People in my family live a long time as a rule. It seems to me that the less you own the cheaper it will be to live. Maintenance, insurance, repairs,subscriptions, it seems every time we turn around we have our hands in our pocket.

So you really have to work out what exactly you expect your life to be like and plan for it.

However that is, I am darn sure that for most of us it is a lot better than it is for our children and I never want to have to rely on the pension.

I worked in financial services for most of my career, a large portion being in corporate superannuation client management. As has been previously mentioned, there is no one size fits all for this simple question. Having seen many clients struggle to find their own answer, including how long they could expect to live, and then working out how best to invest their assets both before and after retirement, my wife and I came up with the very simple strategy of calculating what we would need as an income in retirement (for us we chose $100,000 pa to allow for overseas travel and significant medical expences if they should arise - and to some degree they have) and then considered that we could earn an income of around 5% pa on our invested assets. Thus a lump sum of $2,000,000 was required. In this way, we haven’t had to concern ourselves with what the market is doing at any point because the only thing relevant is the income coming in. Also, the income can go on forever and grows with inflation over time. When we both pass away there will be a large sum of money left over which we can choose to pass on to our children or give away to a charity or a combination of both.

There is a huge financial planning industry that can advise people about this. There are many online sources that can indicatively answer the question.

Judging from the thoughts here, my impression seems to be confirmed.

Just as important, if not more so, is the importance of planning for the non-financial aspects of retirement. It is well-known, for example, that retirees have significantly higher rates of depression.

Yet most people spend more time planning for a three week holiday than they do for the non-financial aspects of retirement, noting the possibility of spending upwards of a quarter century in retirement.

I have a potential conflict of interest, as I’m a part time retirement coach. I was diagnosed with clinical depression about 18 months after I retired. Knowing what depression is like I would never have volunteered to become depressed. Having survived it and wondered about how I came to be so has been insightful and prompted to wonder why so many people gamble that they can transition into retirement as easily as falling off a log. Some do; a sizeable proportion don’t regardless of whether they had enough money to retire.

Money can’t guarantee mental health in retirement, although having enough money to live your preferred lifestyle in retirement does not hurt.

As I have said in a previous post in this thread, money is a part of the retirement consideration.

The most important consideration, I feel, is retire to what?

If you are happy to live an inexpensive lifestyle, then you need less money.

If you want an expensive lifestyle, then more is needed.

I agree with your question: retire to what? One would always want to retire to something, rather then from something.

The lifestyle expense consideration is important.

So are the questions of how to replace the other benefits of work namely, your status or self-identity; purpose; structure of your days and weeks; and socialisation opportunities.

These questions are largely answered for you by work responsibilities and expectations.

In retirement you have to manage these things yourself.

Playing golf seven days a week, for example, will soon lose its novelty, as people find this kind of thing won’t be able to sustain themselves seven days a week for the rest of their lives.

Yes, there is more to retirement than money. I remember senior work colleagues who were forced to retire at 65 and told to “put your feet up”, who died within a year of retirement. My father pleaded with my uncle to “do something, collect stamps, anything …” but he died shortly after. My husband’s parents & grandparents all retired poor and spent their retirement being shuffled between their children & grandchildren, a long unsettled life as they lived, mostly, into their mid 90’s.

As we are more affluent we can buy a lot of independence and entertainment. In our case we bought a farm and 400 years of work. We both had interests outside of work which grew to fill our retirement hours. He decided to move closer to his family and I had to retire prematurely from my Civil Engineering work and I lost my social status. No longer regarded as a competent professional managing multi million dollar projects, winner of the Premier’s Award for Environment, I became a little old lady being called “Darls” and “Luvvie”. Both of us have said “we were happier in XXXX, why did we move?”

I agree with @Rene there is a need for retirement planning beyond the financial. However there are people who refuse to plan, who think it will all work itself out if you ignore it, that the Govt should save them etc. I suspect those who go to a retirement coach are already ahead of the game.

Something doesn’t add up. The story indicates she had proceeds from a sale of a property and there was potentially a substantial change in lifestyle pre and post retirement.

I wonder if good financial advice wasn’t sought and may have contributed to the circumstances at hand.

It adds up. Lyn is now 73. The reference to the bank lending money when she was in her late 50’s. It’s not contemporary with today’s banking environment. The proceeds from the property sale appear to be a share only as part of a divorce settlement at that time. Although not stated explicitly the implication is the funds were insufficient to purchase a property outright at that time. The loan refusal pushed Lyn into needing to rent until retirement.

The ABC has not published more detailed personal information. The article appears to have short handed Lyn’s history as a lead in to the broader story line. One that is about the lower retirement savings of women vs men and how this contributes to poorer outcomes in retirement.

We can all wonder at what might have been. Financial literacy was never taught at school in my day. For many of us the only financial advice that has ever been offered has placed the self interest of the seller ahead of the customer. With reference to those in our family from the same generation as Lyn, and the decades prior, reliable and sound advice was hard to come by. The industry had free reign, and Government ensured free will. The RC in to Banking, Insurance and Financial Services is a lasting testament to the wrongs of those industries, and government failures over recent decades.

But why wouldn’t you drawdown into the ‘capital’ of super? You are proposing a scheme to live off the minimum drawdown of your super if I read you right? So you are trying to hold on to as much of your super balance as possible. What happens when you die… are you intending to set a dependent relative up for life? If so that isn’t what super was set up for…

We plan to deliver to our kids in the later stages of our life. We worked to get to this point because we never really were comfortable with covering our retirement. The rule we imposed meant we can. Of course there are plans and strategies in place so we are able to deliver to the kids, nit have it taken back by government. During our life we worked very hard in remote areas and reaped the rewards. We did no overseas trips till our fifties, but we did fund our kids through graduate and post graduate degrees and music letters and thought that was our duty as parents. Parenting is a noble profession.

Totally agree. All parents desire to provide for the best outcomes for their children. I’m not convinced having them wait until we pass on is of any benefit. Most will be great grand parents and our children retired the way our population is ageing.

We take retirement as an opportunity to be rewarded for all that we gave up in getting our children to full independence and self fulfilment. Perhaps older Australians have a variety of differing expectations of retirement.

There are no inheritance or death taxes in Australia.

What is it that the Australian Govt would take back? Assume this is able to be answered generally.

If a person is looking to get any Govt Age pension giving to the kids will be of limited use. $10,000 total a year in 3 years out of 5 or facing deeming rates on the extra gifting. This deemed amount will be for a number of years, no reduction in time.

If self funding then giving what they like is their choice but also a person also needs to be aware that if too much is gifted and pension is required then amounts gifted before seeking pension may also be treated under deeming rules depending on how long gifted before the claim. This may impact entitlement and or the rate of payment. If wishing to gift substantial amounts before claiming any Age pension it would be wise for a person to do so at a time that places them outside the deeming period ie earlier rather than later. Income and asset amounts for eligibility are reasonably generous and currently do not include the house that is the person’s place of residence that they own.

As we currently have no death or inheritance taxes you are right that the Govt will not be taking anything from the funds other than the normal Super tax rate of 15% on affected amounts.

Some figures from Noel Whittaker’s site (these figures change with 1/2 yearly CPI increases)

A single homeowner can have up to $593,000 of assessable assets and receive a part pension – for a single non-homeowner the lower threshold is $809,500. For a couple, the higher threshold to $891,500 for a homeowner and $1,108,000 for a non-homeowner.

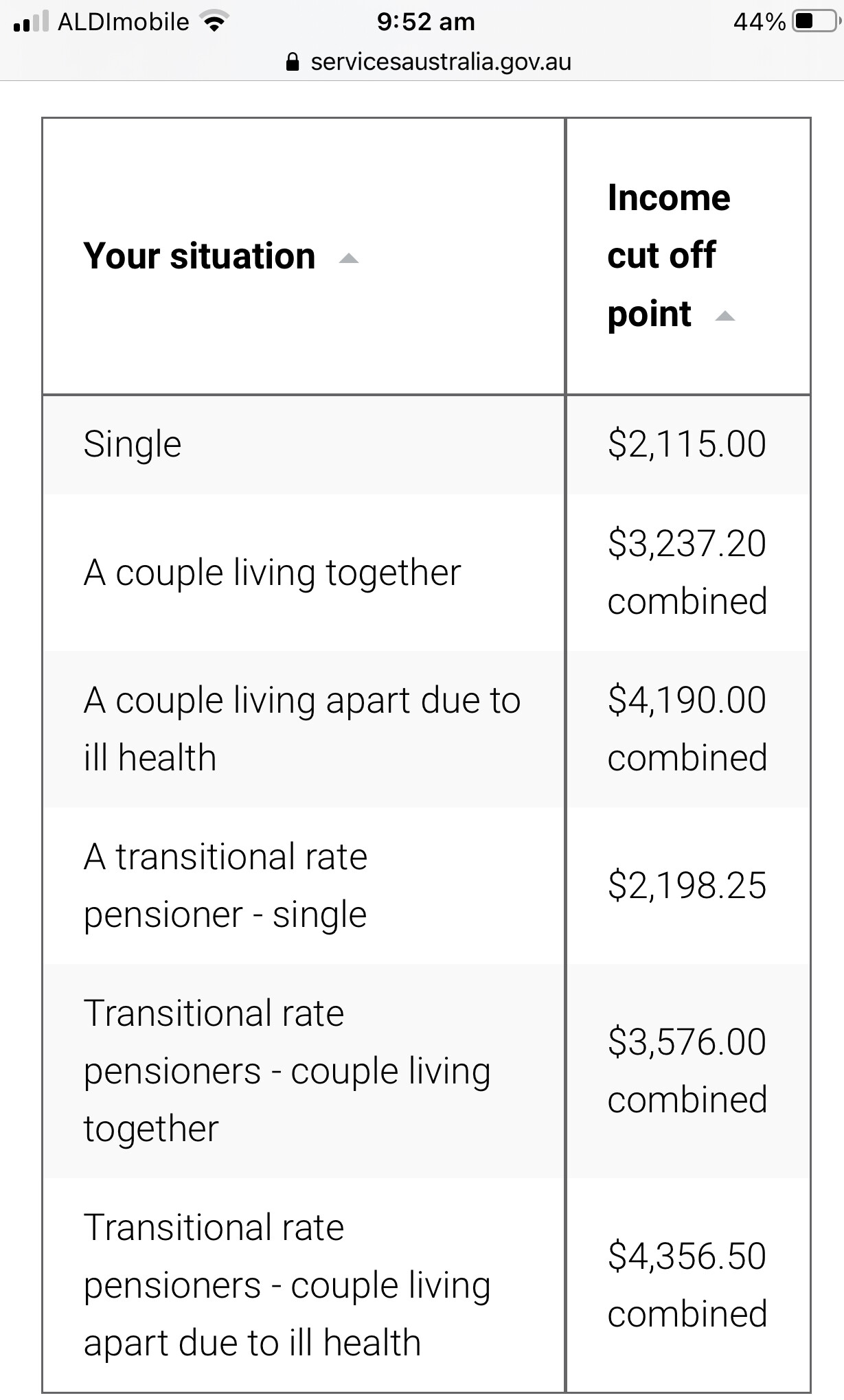

From Services Australia’s site are the Income limits for pension per fortnight at current time (CPI increases also affect limits)

Even at $1,630 it was excellent value!

Even at $1,630 it was excellent value!