Making your own pancakes without commercial mix is very easy and if you have pancakes often you will save money buying the separate ingredients that you don’t already have.

If you lack a mixer use a clean plastic milk bottle and shake them up. This is also easy and has the advantage of being easy to poor into the pan and you can make your mix the night before and have a quick breakfast the next day. Also the texture will improve somewhat as the flour has time to hydrate.

Yes have noticed massive price hikes on lots, if not most, items we buy. A suggestion on how best to deal with it would be useful. Especially as we have health issues that severely restrict our options!

I have noticed a huge increase in Coles Supermarkets, even their own brands. I can’t for the life of me imagine why Kitty Litter Crystals have gone up by 25%, and that isn’t even a year. They should have to justify their increases, but they won’t. I wonder how families are balancing their budgets with such steep increases in everyday products.

I am not defending Coles price increases.

Some explanation may be the increased fuel costs for deliveries, the devastating floods in many of the agricultural areas of eastern Australian, farmers trying to rebuild flocks and herds, the continuing supply chain shortages, lagging Covid pandemic impacts like labour shortages, seasonal demand eg cherries, mangoes, seafood and similar…

You are right, probably all the reasons you give and more are putting up supermarket prices. Having had fair price stability for some time the contrast is now leading people to wish for price control. They may not use that phrase but it amounts to that.

The assumption is that Colesworths is having a lend of us by jacking up prices well beyond explicable reasons. Every anomaly is given as justification for saying so. Overall this may or may not be true, we will never find out though just by saying the price of XYZ went up so it must be so. If we don’t know why the price of XYZ was lower before and we don’t know why it is higher now then we don’t know why the price has risen, it doesn’t prevent speculation though. Aorta doosumfin!

It’s a suggestion, a question to be answered, not an assumption. All I was saying is that my example, which was random as far as it could be, had gone up by about three times inflation, so I was asking if better samples could confirm this or otherwise, and if so, what might explain such a large increase.

However, recent news included an observation that non-discretionary inflation is actually much higher than the overall rate. My sample of groceries would would count as non-discretionary, therefore this is the inflation that would apply to it. The news item quoted annual non-discretionary inflation NDI as being a bit over 18%, about the same as my sample. While this confirms my original observation, it does not explain it, since the measured NDI could just be high because retailers could be using inflation as a cover for unjustified increases.

Either way, there has been significant press coverage in the last fortnight on the subject of grocery price increases, so some attention is being directed to the matter.

I was, speaking to the local iga and asked what happens to the perishable food fresh fruit etc he said gets throw out i ask about the major shops he said they try to repack using fresh ontop ok the packaging. He told me that he refuse to resell trying to hide older underneath new. He mentioned that the previous owners were lousy. Must be so much waste.

It’s common for supermarkets and some other stores to have mark down specials as products approach expiry dates.

We’ve been able to travel a bit over the past 18 months including regional NSW, Vic and some of QLD. From small ‘local’ IGA stores, independent F&V in scale up to the big 3. It’s many years since we came across a fresh food item prepackaged where we might think the unthinkable. New used to top up old to outwit a customer.

The larger supermarket chains all provide consumers with assurances, enabling returning of fresh product for refunds or exchange if it is not up to standard.

I noticed during the recent company reporting season that Coles and Woolworths increased profits in the last year by 14% and 17%. This demonstrates the most amazing cost-cutting by both business, or much more likely, the original assertion that their prices have increased by more than inflation.

High inflation provides the ideal opportunity to increase prices arbitrarily as consumers lose their normal pricing reference points. I maintain that there is a good case for investigation of egregious price increases which not only rob the consumer directly, but add even further to inflation.

These aspects have been covered well in a recent ABC article:

If you look at the gross margin which is the relevant measure, for Coles the gross margin increased from 26.1 per cent to 26.5 per cent (or a percentage increase of 4.1%).

Woolworths’ supermarket gross margins rose 0.48 of a percentage point to 30.7 per cent, while its cost of doing business (CODB) fell 0.3 of a percentage point to 24.8 per cent. The combination of the two pushed its earnings to sales ratio up 0.78 of a percentage point to 5.9 per cent.

The gross margin isn’t revenue…but is a measure of what they make from their sales and thus can impact on the gross profit. It is worth noting that the average increase on product prices would be significantly less than the increase in gross margin and significantly less than the inflation rate which has existed in the past 12 months.

timely article showing how Colesworths have been going. One aspect worth noting though is that in the capitalist world being profitable is not enough, one has to be profitable enough to stave off corporate raiders and analysts who cause share prices to collapse for missing expectations by a percent or few. One basic result is if input prices go up 5% product prices go up by 5% PLUS the margin on that 5% just to stay even with the ‘market’ expectations. Then factor in the economic basis of infinite growth being expected and required and one can surmise what is happening in the board rooms.

Whether UBS is spot on or Coles know better what each customer is purchasing, every consumer knows how it really is. It’s what goes in your basket one has always purchased and what it now costs that counts.

I was going to post the same thing, thanks for beating me to it. This seems to support the argument that it is at least worth investigating the issue, if not by Choice as I was originally hoping then by someone else. As hard-core oligopolists, these two businesses are too powerful to be allowed to run free of scrutiny and it would be disturbing if they are worsening inflation in the interests of their shareholders.

It might be disturbing but reality is that corporations only have two requirements, operating within the law (or at least not getting caught if they do not) and maximising shareholder value.

Ancillary issues such as public good, contributing to society, and so on are not in the mix. To understand any publicly listed business one only need check their annual report for the chief executives KPI’s leading to their bonuses. So long as naming and shaming does not detract from their corporate P/L it is largely irrelevant save for media attention.

Not quite true - they also have to pay attention to

a) social licence, which is not legally specified but can be regulated by the naming and shaming you mention, or the threat of changes to laws and other government pressures, and social media campaigns.

b) trade practices laws which aim to prevent anti-competitive behaviour including oligopolies conspiring or appearing to conspire to ease up on competitive pricing to take advantage of situations like inflation.

Choice already has an important role in the former and potentially could contribute meaningfully to the latter.

The UBS analysis looked at a significant number of food items within a supermarket. The Australian Bureau of Statistics ABS to calculate CPI uses:

The CPI aims to measure price changes for a fixed basket of goods and services over time. In the real world, however, things don’t remain constant - manufacturers and service providers are continually changing their products and services which may result in an improvement or degradation in quality. One challenge in compiling the CPI is to have it only measure any product price change excluding the effects of any quality change. Quality adjustments are the main procedure for ensuring continuity of consistent quality in the basket of goods and services over time.

The ABS basket of food attempts to represent price changes likely to impact on consumers for commonly purchased items. When Choice compares supermarkets, it uses a similar approach which has been accepted as being reasonable when comparing temporal changes or between supermarkets.

The UBS analysis doesn’t represent a basket of food, but pricing for a large number of supermarket items irrespective of whether they are commonly or routinely purchased by consumers. I am yet to meet a consumer whose shopping basket is made up of anywhere near 60,000 items per year. This is where the UBS analysis can misrepresent likely impacts on an average consumer and may result in increases very different to that measured by the ABS (or Choice).

Choice punches well above its weight. With an annual income of a few A$10’s millions. Colesworth in comparison have annual profits around the A$1billion mark, and incomes in the A$10’s of billions. Aldi which is privately owned is more of a mystery.

Does the ABS differentiate between essential items in its basket, or is it simply reflecting the demand averaged across the most purchased products?

From memory the ABS index for “Food and non-alcoholic beverages” includes soft drinks, crisps, take-away food and other items. Items not necessarily in the shopping bag of a family short of funds. My MiL used to purchase day old bread and the cheapest cuts of meat/offal etc to get by.

It may be more meaningful to have a seperate list of items ranked according to different levels of budget and subsistence needs to really know how it goes. Store brand sparkling mineral water used to be 75c a bottle not that long ago and now it’s $1.25. For many it or so called “spring” water are essentials. Perhaps the fact that sugary drinks dominate that category and have not gone up as much hides other outcomes.

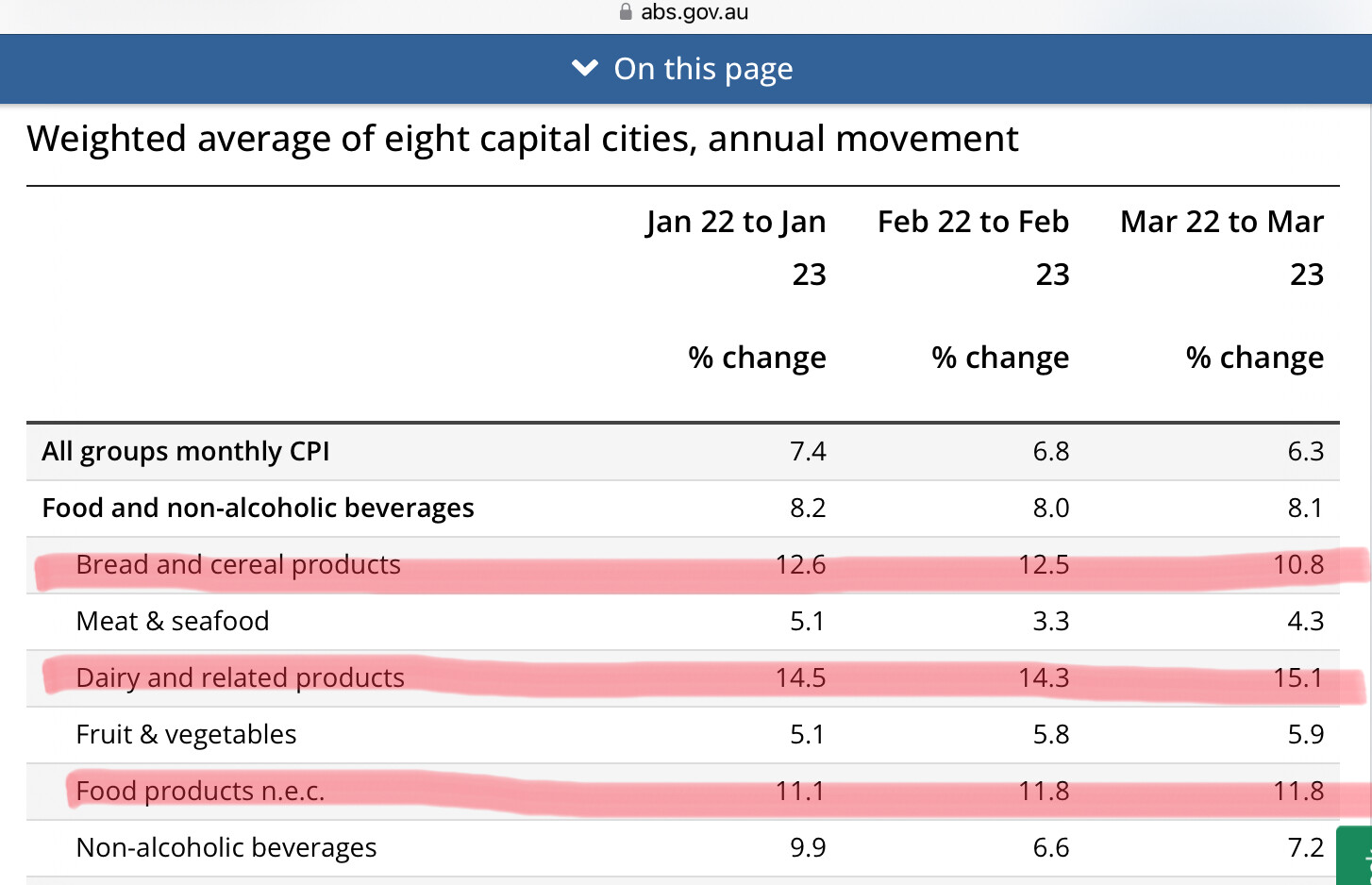

For the 12 months the ABS index which samples more than just supermarket supplied products and prices in the “Food and non-alcoholic beverages” category reported an adjusted 8.1% movement. Looking to some of the sub-categories there are some standouts.

While we might ask how best to interpret the UBS statistic, the ABS data is also open to dispute it’s reliability since very few of us are average. It’s a blended average of what the well off, middle income earners and not so well off purchase. How far it is skewed by including many discretionary items as well as essentials or in which direction, even the ABS knows it’s not perfect. There are both annual and quarterly changes. Households opting for more lower cost alternative products will cause a shift in the cost of the basket hiding the apparent increases in the costs of the more more premium or discretionary items.

While the CPI is often thought of as a fixed basket, in practice the CPI basket is updated in two ways:

Each year the CPI is re-weighted to capture changes in the purchasing patterns of Australian households.

Goods and services (or items) exit the basket every quarter and are replaced by new items.

No-one in the real sense is ‘average’ or buys the ‘food basket’ nominated in the ABS calculations. The purpose of statistics, such as the ‘food basket’ is to represent the likely impact on a consumer. Each and every consumer will have slightly different impacts based on the ‘food basket’ they typically purchase. The same applies to the ‘food basket’ used by Choice in supermarket comparisons. Many of the food items in this basket aren’t bought by many households…but provides an indication of supermarket ‘expensiveness’ when compared to others.

The UBS data is different - it is a possibly measure of change in prices across a whole supermarket rather than impact on consumers (which the ABS provides a measure). It isn’t based on a ‘food basket’ but change in prices for around 60,000 supermarket items. This includes many items which would fit into discretionary spending or never/not routinely purchased by many in the community. This can cause a bias of the impacts of consumer price increases on the consumer, which has been shown in the above data. UBS values are about 1.5% higher than that measured by the ABS. If one purchases the 60,000 items measured by UBS, they might find that their shopping basket has increased by around 9.6% over the past year. If one purchases the ABS basket, then prices would be seen to rise on average of around 8.1%.

As you have highlighted households which are shopping for more lower cost alternatives, such as replacing known brands with store brands, the price impact could be less than that indicated by the ABS. It is possible such households may have seen ‘deflation’ where the lower priced store brands are more than 8.1% less than the branded products purchased in the past.