Over the past few weeks, the COVID-19 coronavirus has revealed just how quickly our financial situations can change. For so many of us and the people we love, our worlds have turned upside down. With little warning, thousands are struggling to pay the bills and navigating complicated processes to get help.

Australia’s major banks have made a good start by committing to some debt repayment relief, but these measures don’t go far enough to match the scale and urgency of a crisis like this.

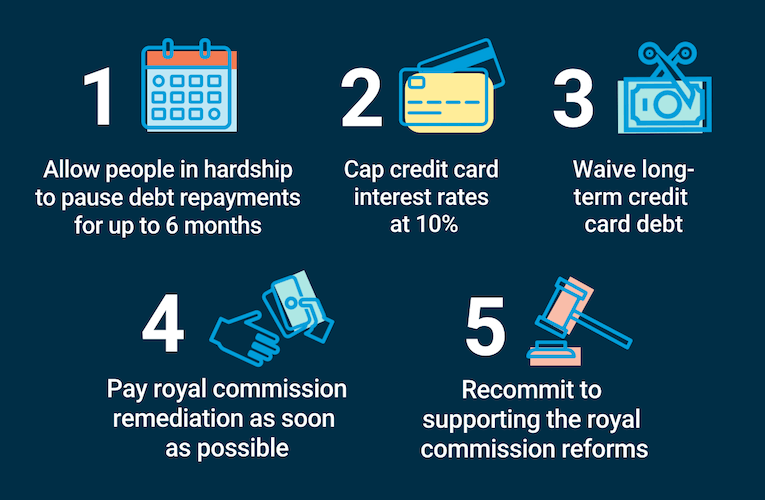

That’s why I’m asking people to call on Australia’s banks to urgently implement these 5 crucial measures to help out anyone doing it tough:

The banks might think they’ve done enough to respond to COVID-19 – but we know they can do more. If we use our voices, we can send a powerful message that the banks must use this moment to right the wrongs revealed through the banking royal commission and to prove that they can be a responsible part of the COVID-19 response. In order to get through this, no company can sit this one out.

So here’s the plan. Together, we’ll:

Investigate and expose banks that treat people who are doing it tough unfairly

Work with banks to improve their processes and measures to help people

Rank and compare banks on their responses to COVID-19 to encourage good conduct and name and shame the worst examples

I know this kind of pressure works because we’ve done it before. The sweeping changes to the financial industry following the banking royal commission only kicked off after thousands of us called for change and didn’t stop until we got it. I know that we can do it again, but I need your voice.

Westpac has sent us new terms, from June, dropping our mortgage payments. We are in the position to not need this. I cannot go online to change this, until after the change has been made in their system and have now spent 3 hours on hold trying to get it corrected.

I will have to make a note in my calendar, so that I am sent a reminder in June, to change it online.

Having had poor experiences with Commbank in the past, they are never an option for a mortgage, but now we are stuck with Westpac. It is too soon to move the mortgage to another bank, having recently changed.

If you have access to a branch, maybe go and see the loans officer and get them to change it. Would save effort and stress should there be online problems in June.

Has anyone else with Westpac read the fine print in their covid 19 relief package? My understanding is that the 55 days Interest free will be lost on new purchases after the relief period is over- unless balance remaining is paid in total by the time the package expires. So Westpac will basically make all its money back In interest if you can’t pay the total statement balance at the end of 3 months?!!

I have moved your post into this topic as this topic deals with CHOICE’s campaign about the Banking sector and their responses to the COVID-19 issues. Your complaint about Westpac either fits here or in the topic on COVID-19 and poor business behaviour.

It would seem from what you detail there may be a catch up by the bank once the situation has improved leaving the customers no better off and indeed they may be far worse off. Hopefully it isn’t the case but the details you provide will interest CHOICE and they may wish to get further details from you to

maybe give you some help and

to help others in the same situation and finally

let the Banks know they need to fix their game.

I hope the Community will continue to provide advice, help and support to you into the future and that you will continue to participate in areas of the site that interest you.

This is the webpage on the Westpac support package…

It appears that the 3 month (3 statement cycles) stay in interest and repayments applies to

new purchases/cash advances made on the card

existing amounts owed on the cards

After the 3-month support period, you will need to make at least the minimum monthly repayment on your account to ensure one continues to receive the support package from Westpac…that being the 3 month interest free period. While I haven’t checked, if one does not make minimum repayments, it appears on face value that interest which would otherwise have been accrued would be added back to the account/credit card.

There are also requirements to be get to get tye support, namely…

held your credit card account on the 1st January 2020 and haven’t applied for hardship assistance on this account, or the account isn’t currently under hardship assistance

have been up-to-date with your minimum repayments at some point during the last 90 days

have lost your job or suffered a loss of income as a result of COVID-19

Reading this, once the 3 month stay finishes, the credit card returns to ‘normal’ where the account starts to accrue interest on owed monies and the account holder is required to pay back (at least at minimum monthly repayments) monies owed on the card. Any purchases made before, during or after support package is in effect would then accrue interest. The stay in interest/repayments is only for 3 months and not for purchases made during this perid until paid off.

It’s not the minimum amount required to be paid at the end of the payment pause in order to continue to receive the benefits of the relief package- it’s the entire statement balance.

I guess I will see come September as I can’t get a straight answer from Westpac.

I am not sure where you are getting this impression, but the Westpac website and T&Cs you have posted indicate otherwise.

The information indicated that if one pays at least the minimum monthly amount (or the Monthly Payment amount under SmartPlan) after the 3 month interest rate and repayment stay, then the benefits of the 3 month stay are retained. If one chooses not to pay at least the minimum monthly repayments, the benefits of the stay are not longer provided by Westpac.

Interest is calculated on the whole of the monies owned on the credit card on a month by month basis and the balance owed on the credit card will accrue interest for the balance at the start of the stay period as well as any purchases made during the stay period…once the stay period ceases (this being the balance owed at the end of the stay period).

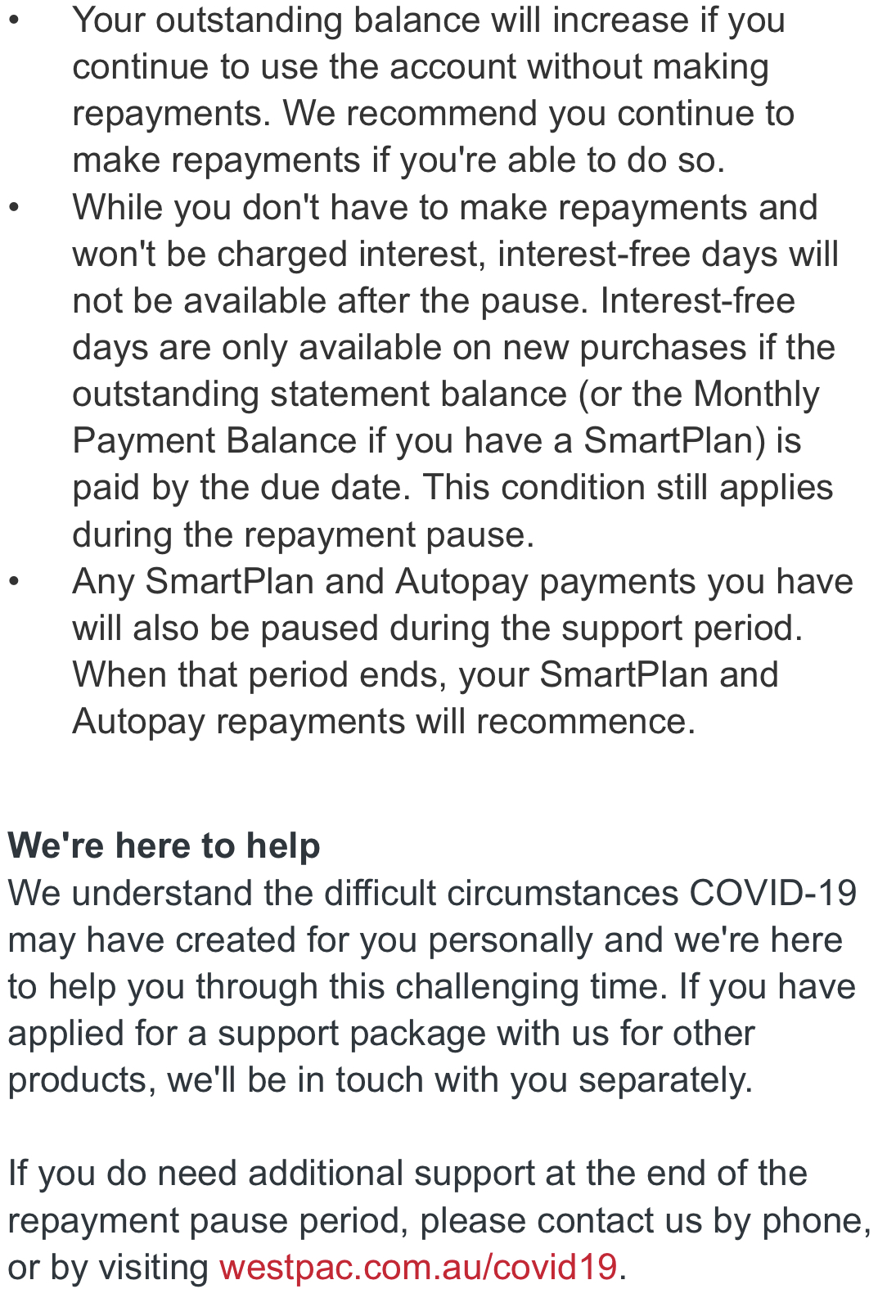

I can see where it could be confusing in the second and third dot point in the image above. “While you don’t have to make repayments…won’t be charged interest…Interest-free days will not be available after the pause…Interest-free only available on new purchases if outstanding statement balance is paid…or the Monthly Payment Balance if you have a SmartPlan”…then it goes on to say “SmartPlan and Autopay payments will be paused” so if they pause the SmartPlan a person will be charged interest it might seem as the SmartPlan payment is not occurring.

I don’t think that’s the way it should be read but it might confuse someone and then Westpac should be able to quickly reassure the customer.

I have this impression as the picture above is a direct screen shot of the terms and conditions of my own Covid 19 Package and mine has not been adjusted to my own circumstances in any way.

It’s just the generic one they rolled out.

Rather than go around in circles-

I will speak to Westpac about this and get confirmation of these terms in writing.

I have it in writing from Westpac that the interest on purchases made during the period the Covid 19 Relief Package will be added if The full statement balance is unpaid when the package ceases. I asked this question very specifically.

I still don’t know if this is factually correct (in that this is how this particular employee I liased with interpreted the wording), but I have this in writing from Westpac. I can’t share this here as it has identifying details.

Do you normally pay your credit card account off in full each month/statement cycle?

Is this answer in relation to whether an interest free period exists after the stay? Westpac written information indicates that there is no interest free period and to avoid any interest, one would need to pay the balance off in full. Interest which otherwise would have accumulated during the stay isn’t added unless one doesn’t at least make a minimum repayment.

If one doesn’t pay it off in full, then any credit still owed at the end of the stay period would start accumulating interest from the first day after the stay period ceases.

There is also no interest free period (e.g. 55 days) at the end of the stay period…I assume that interest free rolls into the stay period.

It doesn’t make sense to give one a stay and then if the balance isn’t paid off in full at the end if the stay, the benefit associated with the stay is forfeited. Westpac makes it clear that pre-stay balances won’t accumulate interest or repayments are needed during the stay and benefits are only forfeited when at least the minimum repayment is made post-stay.

If the balance needs to be paid off in full otherwise the offer is forfeited only benefits Westpac for those customers which don’t pay off in full. It doesn’t make sense nor concur with the information from Westpac.

I asked specifically about interest being added to purchases made during the stay Period and whether the statement balance or minimum payment had to be paid on expiry of the relief package.

I was not referring to the loss of the 55 days interest free when the statement balance is not paid in full.

I have it in writing from Westpac that it’s the statement balance, and when I spoke to a staff member over the phone they kept saying kept saying ‘ remember this is only a pause’ . Whether the team member has also misinterpreted I don’t know… I’ve spent hours on the phone, at the branch and online chat trying to figure out what on earth the terms and conditions are, as what I am being told by Westpac staff members, what is on the website and what I have in the relief package terms and conditions all differs.

From the information Westpac is giving me, I will be paying my first statement balance after the relief package expires in full and then closing the account, simply from the run around I have had trying to get clarification about the terms and conditions of the package. I don’t know if it’s also just a case of the left hand not knowing what the right is doing.

It Absoltuley does not make sense to offer relief and then take it back, but This is what I keep being told.

That’s all from me on this topic as I can’t get any clearer information from Westpac and I’ve been a customer of theirs for many many years.

You can respond to Patrick Veyret by sending an email to community@choice.com.au and addressing the body of the email to Patrick with the subject something similar to “NotHappyJan for Patrick Veyret”. I’m sure Patrick will then respond to you with perhaps his email account details or a reply from the Community email address to your’s. The Community does not see the emails and if you gain enough experience in the forum you will also be able to private message (PM) individuals, the messages are only able to be seen by those included in the PM.